Downloaded 13 times

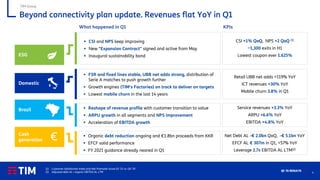

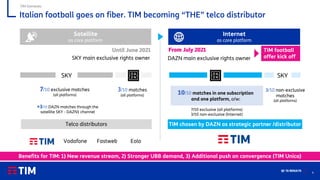

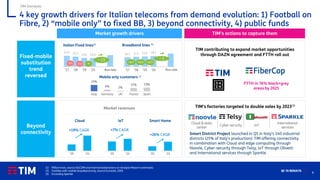

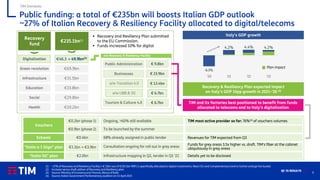

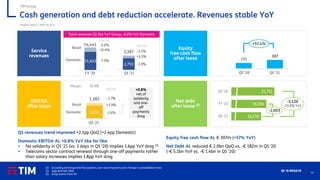

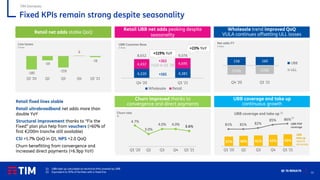

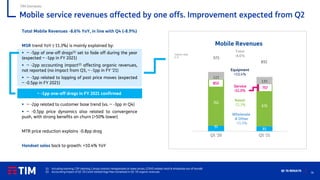

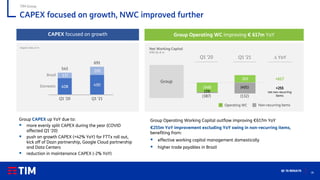

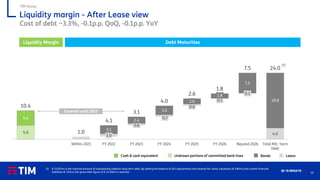

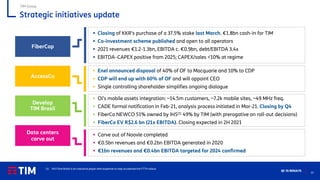

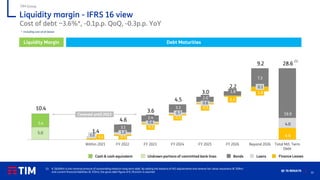

- TIM Group reported Q1 2021 results with revenues flat YoY and accelerating cash generation and debt reduction. Net debt was reduced by €2.0bn in Q1. - For TIM Domestic, fixed service revenues stabilized YoY while mobile service revenues declined slightly. UBB coverage and take up continued to grow. - Key growth drivers for TIM include the distribution of Italian football exclusively on fiber networks beginning in July 2021, capturing the shift from mobile-only to fixed broadband, leveraging opportunities in beyond connectivity areas, and benefitting from public funds being allocated to Italy's digitalization.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)