Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Similar to Thought for the_week_-_268

Similar to Thought for the_week_-_268 (20)

More from theretirementengineer

More from theretirementengineer (19)

Recently uploaded

Recently uploaded (8)

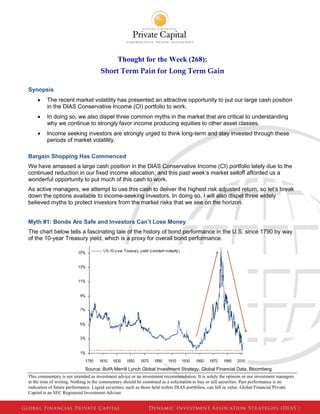

Thought for the_week_-_268

- 1. This commentary is not intended as investment advice or an investment recommendation. It is solely the opinion or our investment managers at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Past performance is no indication of future performance. Liquid securities, such as those held within DIAS portfolios, can fall in value. Global Financial Private Capital is an SEC Registered Investment Adviser. Thought for the Week (268): Short Term Pain for Long Term Gain Synopsis The recent market volatility has presented an attractive opportunity to put our large cash position in the DIAS Conservative Income (CI) portfolio to work. In doing so, we also dispel three common myths in the market that are critical to understanding why we continue to strongly favor income producing equities to other asset classes. Income seeking investors are strongly urged to think long-term and stay invested through these periods of market volatility. Bargain Shopping Has Commenced We have amassed a large cash position in the DIAS Conservative Income (CI) portfolio lately due to the continued reduction in our fixed income allocation, and this past week’s market selloff afforded us a wonderful opportunity to put much of this cash to work. As active managers, we attempt to use this cash to deliver the highest risk adjusted return, so let’s break down the options available to income-seeking investors. In doing so, I will also dispel three widely believed myths to protect investors from the market risks that we see on the horizon. Myth #1: Bonds Are Safe and Investors Can’t Lose Money The chart below tells a fascinating tale of the history of bond performance in the U.S. since 1790 by way of the 10-year Treasury yield, which is a proxy for overall bond performance. Source: BofA Merrill Lynch Global Investment Strategy, Global Financial Data, Bloomberg

- 2. This commentary is not intended as investment advice or an investment recommendation. It is solely the opinion or our investment managers at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Past performance is no indication of future performance. Liquid securities, such as those held within DIAS portfolios, can fall in value. Global Financial Private Capital is an SEC Registered Investment Adviser. The 10-year Treasury fell to a 220-year low of 1.4% in July 2012 (red dotted line) and reached 1.7% just four months ago – both due to the Fed’s Quantitative Easing (QE) program which has been purchasing $85 billion in bonds each month since September 2012. By simply comparing what happened the last time the 10-year Treasury yield fell to these levels, which was during the Great Depression, we are left with two key takeaways: 1. Bonds Are Not Always Safe: Bond prices are inversely related to their yields so as the yield rises, the bond price falls. Bear markets in bonds exist and the most recent one lasted 35 years from 1946 – 1981 (upward pointing red arrow). 2. The Party is Over: The end of the greatest bond market in U.S. history is currently unfolding (downward pointing red arrow). We watched bonds outperform for the last 31 years, and as difficult as it may be to accept, bond prices have only one direction to go and that is down. Short-term interest rates are at zero percent, and at some point they will rise just as they did after the Great Depression. Given the abnormally low interest rate level for such a long amount of time leads us to believe that bonds could suffer years of price pressure until the bond market normalizes. NOTE: A rise in interest rates causes the price of bonds to fall because investors sell these bonds in order to reinvest their money at the newer, higher interest rates. Bonds with longer maturities tend to suffer more than shorter maturities because they pay back the principal further down the road, posing greater reinvestment risk, and subsequently face steeper price declines as rates rise. A common pushback is that since investors are guaranteed to get their principal back at maturity, these government securities are “risk free” and the logic above does not apply. However, this guarantee only eliminates default risk and provides absolutely no protection from interest rate and inflation risk. Coupon payments on most government securities and corporate bonds are fixed and do not adjust with inflation or interest rate changes. Therefore, if either inflation or interest rates increase, then the value of that fixed payment will be worth less to the recipient. For example, if an investor purchased a 10-year Treasury back in April yielding 1.7%, and then over time long-term interest rates rose to 4.5% by 2017, that investor would receive less than half the going rate of return on his principal for a remaining six years unless rates were to drop back down dramatically. The bottom line is that bonds are not always safe and currently face legitimate price risk unless held to maturity. Furthermore, even if investors keep their bonds to maturity to prevent capital losses, the fixed coupon payment holds them hostage to lower comparable returns in a rising interest rate environment. Myth #2: Interest Rates Can’t Stay Low for Too Much Longer Well if there is just too much risk by locking up principal for several years in government bonds, some investors argue to simply stay in money market funds and CDs until the day rates rise – effectively waiting for the storm to pass. The chart below shows the 3-month U.S. Treasury bill yield, which is a proxy for money market funds, and blueprints just how long an investor may have to wait for rates to normalize.

- 3. This commentary is not intended as investment advice or an investment recommendation. It is solely the opinion or our investment managers at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Past performance is no indication of future performance. Liquid securities, such as those held within DIAS portfolios, can fall in value. Global Financial Private Capital is an SEC Registered Investment Adviser. Source: BofA Merrill Lynch Global Research, Haver Analytics, Bloomberg The last time short-term interest rates were this low was during the 1930s – 1940s, and comparing now vs. then leaves us with two key takeaways: 1. Current Rates Generate No Income: The U.S. 3-month Treasury bill yields 0.02% today and the all-time low was 0.01% in 2011. Income seeking investors that have stayed in money market funds and CDs have generated no income for the past 5 years on these investments. 2. We Can Be Here A While: Back then, rates stayed near zero for roughly 15 years. Furthermore, rates did not reach the average of 3.7% until 1960, or 30 years of below average returns. Now the Fed will likely begin tapering QE within the next few months, but tapering does not equate to an end to QE. Economists currently estimate that tapering will only result in a decrease from $85 billion in bond purchasing per month down to $65 billion, and QE will likely not end completely until summer 2014. Furthermore, an end to QE does not equate to an immediate rise in interest rates, and given the Fed’s expectation of unemployment below 6.5%, we do not anticipate an interest rate hike until 2015/16 at the earliest. Finally, once rates do begin to rise, they will likely increase slowly so attractive returns to an income seeking investor in a money market fund or CD could potentially be a decade or more away. The bottom line is that income-seeking investors cannot simply wait out this storm. Not only will these vehicles generate immaterial income, they will also be subjected to the effects of inflation every year. NOTE: The inflation rate in the U.S. currently sits around 2.3%. This figure states that if you put a $100 bill under your mattress, the purchasing power of that $100 will be 2.3% less one year from now (the cost to buy goods like food and clothing would have risen on average by 2.3% so now your $100 has the power to buy less). Any investment that yields less than 2.3% annually is losing purchasing power. Myth #3: Volatility in Equities is Bad Many investors believe any weakness in the equity markets is a leading indicator of worse times to come, but fortunately for investors, nothing could be further from the truth. Take a look at the 5-year chart of the S&P 500 below to see why volatility in equity markets is actually healthy.

- 4. This commentary is not intended as investment advice or an investment recommendation. It is solely the opinion or our investment managers at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Past performance is no indication of future performance. Liquid securities, such as those held within DIAS portfolios, can fall in value. Global Financial Private Capital is an SEC Registered Investment Adviser. Source: Bloomberg The red circles indicate the larger volatility induced selloffs but notice that the overall trend is rising. These spikes are attributed to short-term traders exiting for a variety of non-fundamentally driven reasons. Long-term investors, on the other hand, love to buy on these dips. NOTE: A natural question is when does an investor know the difference between a correction and a material change in a fundamental thesis? We mostly look for signs that our economy or a thesis has fundamentally changed – slower growth, change in leading indicators, etc. Currently we see very little risk of falling back into a recession given the continued flow of positive economic data. Let’s use this most recent sell off, driven by fears of a potential strike against Syria and tapering from the Fed, as an example. We argue that a strike against Syria poses no fundamental change to our long-term thesis of the stocks in our portfolios. Furthermore, the Fed will only begin tapering and ultimately unwind QE when they feel that our economy is strong enough to grow on its own – a very positive sign for an investor. Therefore we conclude that traders are running for the exits because investors see no change to the thesis for owning stocks. The bottom line is that volatility in equities is to be expected and determining the cause of the volatility will often present an investor with an opportunity to buy stocks that go on sale for more technical reasons than fundamental ones. Implications for Income Seeking Investors The war against seniors and savers has forced income-seeking investors to choose between three primary options, all of which embed tradeoffs: 1. Money Markets & CDs: Generate no income while inflation eats away at the principal for several years to come. 2. Fixed Income: Bonds offer lower volatility but are also headed in one direction and that is down. The risk-adjusted return seems to us like running in front of a steamroller to collect a dime.

- 5. This commentary is not intended as investment advice or an investment recommendation. It is solely the opinion or our investment managers at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Past performance is no indication of future performance. Liquid securities, such as those held within DIAS portfolios, can fall in value. Global Financial Private Capital is an SEC Registered Investment Adviser. 3. Income Generating Equities: Endure occasional short-term volatility (pain) for attractive long- term returns (gains) driven by healthy yields and capital appreciation from an improving economy. We believe that income seekers are best suited holding a diversified portfolio heavily weighted to Option #3, and we are currently deploying our cash in just this manner. Lastly, as uncomfortable as these volatility spikes may become at times, the Investment Committee continues to strongly believe that there is very little risk of a recession and urge our investors to: 1. Stay Invested: Selling inside those red circles above is a recipe for locking in short term losses and missing out on long-term gains. 2. Be Patient: Equity volatility and active management of our portfolios in anticipation of market changes make measuring performance over any time period less than a year inappropriate, and investors are best suited by maintaining an 18-month time horizon at the very minimum.