- New fracking technologies have led to significantly increased supplies of oil and natural gas in the US, leading to diverging prices between US oil (WTI) and international oil (Brent).

- WTI prices have fallen more than Brent prices due to increased US production and limited export infrastructure, creating a price advantage for US companies.

- This divergence in oil prices is expected to continue and provide competitive advantages to US companies through lower input costs, while also creating new jobs and moving the US closer to energy independence over the next 10-20 years.

Please find attached our complimentary copy of our Oil Buyer's Guide 2013 Review. This is just a sample of incredible content our subscribers receive each day. Visit bloombergbriefs.com for more information.

A Green Movement Approach: South African Fuel Price Part 1Lwandle Fakazi

From 2011 to June 2018, local fuel price have grown by over 8% annually while Brent Crude Oil Price (in dollars) shrunk by over 2% per annum in the same period. Follow the link to download Part 1 of a series unbundling the nature of our local fuel prices.

The oil industry, with its history of booms and busts, is in its deepest downturn since the 1990s, if not earlier.

Earnings are down for companies that made record profits in recent years, leading them to decommission more than two-thirds of their rigs and sharply cut investment in exploration and production. Scores of companies have gone bankrupt and an estimated 250,000 oil workers have lost their jobs.

The cause is the plunging price of a barrel of oil, which has fallen more than 70 percent since June 2014.

Prices recovered a few times last year, but a barrel of oil has already sunk this year to its lowest level since 2004. Executives think it will be years before oil returns to $90 or $100 a barrel, a price that was pretty much the norm over the last decade.

Brent crude, the main international benchmark, was trading at around $29.64 ( 21st February 2016) a barrel on Saturday.

United States production has surged in recent years as the shale boom took off. That has helped create a glut of oil as major producers like Saudi Arabia continue to pump at high levels.

A study released by the analysts at consulting firm Deloitte that looks at the top issues facing the oil and gas sector. The study finds that within the next 5-6 years surging shale oil and natural gas production in the U.S. will "cut deeply" into OPEC's influence on setting world oil prices.

Please find attached our complimentary copy of our Oil Buyer's Guide 2013 Review. This is just a sample of incredible content our subscribers receive each day. Visit bloombergbriefs.com for more information.

A Green Movement Approach: South African Fuel Price Part 1Lwandle Fakazi

From 2011 to June 2018, local fuel price have grown by over 8% annually while Brent Crude Oil Price (in dollars) shrunk by over 2% per annum in the same period. Follow the link to download Part 1 of a series unbundling the nature of our local fuel prices.

The oil industry, with its history of booms and busts, is in its deepest downturn since the 1990s, if not earlier.

Earnings are down for companies that made record profits in recent years, leading them to decommission more than two-thirds of their rigs and sharply cut investment in exploration and production. Scores of companies have gone bankrupt and an estimated 250,000 oil workers have lost their jobs.

The cause is the plunging price of a barrel of oil, which has fallen more than 70 percent since June 2014.

Prices recovered a few times last year, but a barrel of oil has already sunk this year to its lowest level since 2004. Executives think it will be years before oil returns to $90 or $100 a barrel, a price that was pretty much the norm over the last decade.

Brent crude, the main international benchmark, was trading at around $29.64 ( 21st February 2016) a barrel on Saturday.

United States production has surged in recent years as the shale boom took off. That has helped create a glut of oil as major producers like Saudi Arabia continue to pump at high levels.

A study released by the analysts at consulting firm Deloitte that looks at the top issues facing the oil and gas sector. The study finds that within the next 5-6 years surging shale oil and natural gas production in the U.S. will "cut deeply" into OPEC's influence on setting world oil prices.

A Guide to Investing in Oil Some investors believe that today’s low oil prices mean the time is ripe for investing in oil. Here’s where to start. Those watching the oil space know that prices for the fuel have been volatile since they soared past $140 per barrel in 2008.

What the drop in oil prices means for the economy and office marketsJLL

Oil prices are below $65 per barrel for the first time since 2009, and energy producers across the globe are starting to panic. Lower prices will likely extend into 2015—bad news for energy companies and the downstream industries that support them, but good news for the U.S. economy and consumers.

We expect demand for real estate in the energy markets to weaken. Landlords and developers will feel pressure to secure and retain occupancy. But, the benefit of sustained low oil prices will fuel (pun intended) retail, residential, industrial and office demand across the United States overall.

Learn more about the energy industry, and our services for companies in the field, at http://bit.ly/1qSz2Li

Oil prices falling and Their Impact on World and Indian EconomyRishabh Hurkat

The presentations is focused on Reason Behind the Fall in Global Crude Oil Prices.

It also inculcates various Charts and Data which are Up-to-date.

The Basic Reason is to understand the Effect on Global and Indian Economy.

Oil is the major

source of energy from most of the developed as well as developing countries around the world.

Therefore a change in the supply of oil will significantly affect operations in most parts of the

world. There are a number of factors that affect the demand and supply of oil in the world.

- See more at: http://www.customwritingservice.org/blog/factors-affecting-demand-and-supply-of-oil

declining crude oil pricing:causes and global impactSatyam Mishra

this presentation gives some insight into the causes of declining crude oil pricing and how that is going to affect various oil producing and non oil producing countries across the globe.

Impact of Oil Prices on the Economic Growth of PakistanMuhammad Sharjeel

We gathered data from different resources and then finalize our presentation. The intention to upload this file is to help those guys who need some guidelines for preparing presentation. :)

Capital Builder Provides BTST (Buy Today Sell Tomorrow) calls. In case of BTST it is usually advisable to take an overnight trade in f&o segment.

Read More@ https://www.capitalbuilder.in/

This ppt is of subject called Elements of Corporate Finance .

it include the information about the OPEC , reasons , some current information about crude oil and major suppliers of crude oil to india( 2015)

A Guide to Investing in Oil Some investors believe that today’s low oil prices mean the time is ripe for investing in oil. Here’s where to start. Those watching the oil space know that prices for the fuel have been volatile since they soared past $140 per barrel in 2008.

What the drop in oil prices means for the economy and office marketsJLL

Oil prices are below $65 per barrel for the first time since 2009, and energy producers across the globe are starting to panic. Lower prices will likely extend into 2015—bad news for energy companies and the downstream industries that support them, but good news for the U.S. economy and consumers.

We expect demand for real estate in the energy markets to weaken. Landlords and developers will feel pressure to secure and retain occupancy. But, the benefit of sustained low oil prices will fuel (pun intended) retail, residential, industrial and office demand across the United States overall.

Learn more about the energy industry, and our services for companies in the field, at http://bit.ly/1qSz2Li

Oil prices falling and Their Impact on World and Indian EconomyRishabh Hurkat

The presentations is focused on Reason Behind the Fall in Global Crude Oil Prices.

It also inculcates various Charts and Data which are Up-to-date.

The Basic Reason is to understand the Effect on Global and Indian Economy.

Oil is the major

source of energy from most of the developed as well as developing countries around the world.

Therefore a change in the supply of oil will significantly affect operations in most parts of the

world. There are a number of factors that affect the demand and supply of oil in the world.

- See more at: http://www.customwritingservice.org/blog/factors-affecting-demand-and-supply-of-oil

declining crude oil pricing:causes and global impactSatyam Mishra

this presentation gives some insight into the causes of declining crude oil pricing and how that is going to affect various oil producing and non oil producing countries across the globe.

Impact of Oil Prices on the Economic Growth of PakistanMuhammad Sharjeel

We gathered data from different resources and then finalize our presentation. The intention to upload this file is to help those guys who need some guidelines for preparing presentation. :)

Capital Builder Provides BTST (Buy Today Sell Tomorrow) calls. In case of BTST it is usually advisable to take an overnight trade in f&o segment.

Read More@ https://www.capitalbuilder.in/

This ppt is of subject called Elements of Corporate Finance .

it include the information about the OPEC , reasons , some current information about crude oil and major suppliers of crude oil to india( 2015)

Mercer Capital's Value Focus: Energy Industry | Q3 2021 | Segment: BakkenMercer Capital

Mercer Capital's Energy Industry newsletter provides perspective on valuation issues. Each newsletter also typically includes a macroeconomic trends, industry trends, and guideline public company metrics.

Mercer Capital's Value Focus: Energy Industry | Q2 2022 | Segment: PermianMercer Capital

Mercer Capital's Energy Industry newsletter provides perspective on valuation issues. Each newsletter also typically includes macroeconomic trends, industry trends, and guideline public company metrics.

Mercer Capital's Value Focus: Energy Industry | Q3 2019 | Region Focus: BakkenMercer Capital

Mercer Capital's Energy Industry newsletter provides perspective on valuation issues. Each newsletter also typically includes macroeconomic trends, industry trends, and guideline public company metrics.

TD Securities Calgary Energy Conference 2014Enbridge Inc.

Al Monaco, President and CEO, Enbridge Inc. discussed the strategic imperative of energy market access before an audience of investors, business leaders, and energy industry representatives.

• US tight oil production and the future oil price

• Dubai:MD and CEO of DEWA receives CEO of First Solar

• UAE's Masdar inks deal to build Mauritania solar projects

• No 'significant' change in Saudi oil policy after king's death

• Algeria:To increase its oil output & renewable energy projects production

• Norway: Det norske commences drilling on the Ivar Aasen field

• Bangladesh:KrisEnergy completes 2D seismic program in SS-11

• India: Energy subsidies prove drain on Indian economy

• Oil producers in US not able to drill at $45 a barrel

• Oil price plunge to boost global M&A activity in 2015, says EY

Mercer Capital's Value Focus: Exploration and Production | Fourth Quarter 202...Mercer Capital

Mercer Capital's Energy Industry newsletter provides perspective on valuation issues. Each newsletter also typically includes a macroeconomic trends, industry trends, and guideline public company metrics.

Mercer Capital's Value Focus: Energy Industry | Q1 2022 | Region Focus: Eagle...Mercer Capital

Mercer Capital's Energy Industry newsletter provides perspective on valuation issues. Each newsletter also typically includes macroeconomic trends, industry trends, and guideline public company metrics.

Mercer Capital's Value Focus: Energy Industry | Q1 2020 | Region Focus: Eagle...Mercer Capital

Mercer Capital's Energy Industry newsletter provides perspective on valuation issues. Each newsletter also typically includes macroeconomic trends, industry trends, and guideline public company metrics.

Mercer Capital's Value Focus: Exploration and Production | Q3 2018 | Segment:...Mercer Capital

Mercer Capital's Exploration and Production newsletter provides perspective on valuation issues. Each newsletter also typically includes macroeconomic trends, industry trends, and guideline public company metrics.

The Saturday Economist Oil Market Update 2015John Ashcroft

What is pushing oil prices lower? What’s the difference between Brent Crude or West Texas Intermediate? Will prices stay low and what are the prospects for oil demand growth? Who are the winners and losers? What is the impact of lower oil prices on the economy? Are lower oil prices good for growth? What does the falling price mean for the consumer? US Oils rigs go up as the oil prices rise, so is the real challenge, Sheiks versus Shale or a Western squeeze on Russian resources?

Check out our oil market update to understand just what is happening in the oil Market

Mercer Capital's Value Focus: Energy Industry | Q1 2021 | Region Focus: Eagle...Mercer Capital

Mercer Capital's Energy Industry newsletter provides perspective on valuation issues. Each newsletter also typically includes macroeconomic trends, industry trends, and guideline public company metrics.

Recently commodity prices have fallen to multi-year lows. Read our December Market Perspective to learn how these dramatic price movements may impact consumers, industries and companies.

NewBase 16 October 2023 Energy News issue - 1665 by Khaled Al Awadi_compres...Khaled Al Awadi

NewBase 16 October 2023 Energy News issue - 1665 by Khaled Al AwadiNewBase 16 October 2023 Energy News issue - 1665 by Khaled Al AwadiNewBase 16 October 2023 Energy News issue - 1665 by Khaled Al AwadiNewBase 16 October 2023 Energy News issue - 1665 by Khaled Al AwadiNewBase 16 October 2023 Energy News issue - 1665 by Khaled Al AwadiNewBase 16 October 2023 Energy News issue - 1665 by Khaled Al AwadiNewBase 16 October 2023 Energy News issue - 1665 by Khaled Al AwadiNewBase 16 October 2023 Energy News issue - 1665 by Khaled Al Awadi

EY Price Point: global oil and gas market outlookEY

We enter 2021 on a note of cautious optimism for global health, the world economy, and the oil and gas markets. The first weeks of December brought approval in the US and the UK of the first of several COVID-19 vaccines. The speed with which vaccine development occurred is unprecedented, but certainly welcome. In the weeks following the early November announcement of 90+% effectiveness by the manufacturer of the first approved vaccine, the price of WTI crude oil increased by US$10/bbl to US$48/bbl, the highest level since early March. Sustainability hasn’t returned yet, and whatever time it takes to get the world to normal, it will take even longer for normalization within the oil and gas markets. Inventories remain at historically high levels and, optimistically, it will take until April before inventory returns to levels observed in the preceding five years. That’s an estimate, and there has obviously been some difficulty properly calibrating the expectations of how balance will return and how long it will take. In late November, OPEC met to adjust its output plans because of the anemic rebound in demand. In mid-December, the IEA lowered its demand forecast for 2021 due mostly to continued sluggishness in aviation fuel demand.

A mild winter has interrupted a recovery in North American natural gas prices after a run-up motivated by curtailed capital expenditures, upstream activity and production. After an initial meltdown, with cargo cancellations and dramatic price reversal, LNG markets have made a remarkable comeback, and the spread between Asia and Henry Hub has reached a level we haven’t seen in almost three years. It may be the case that interruption in FIDs has brought us to the cusp of a balance that can support reliable returns.

Oil Prices have been extremely volatile during the last decade due to extensive speculative pressures on the commodity. in this episode of Energy Risk Management Series we show one of the methods of countering the same.

1. This commentary is not intended as investment advice or an investment recommendation. It is solely the opinion or our investment managers

at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Past performance is no

indication of future performance. Liquid securities, such as those held within DIAS portfolios, can fall in value. Global Financial Private

Capital is an SEC Registered Investment Adviser. All charts courtesy of Bernstein Research.

Thought for the Week (257):

Two Prices for Oil

Synopsis

Natural gas prices have declined dramatically over the past 5 years due to new technologies that open access to reserves once deemed too costly to pursue.

Despite similar technologies allowing access to new oil reserves in the U.S. and Canada, we have not seen as dramatic of a price decline because the cost to extract these reserves is much higher.

However, we are experiencing a divergence in the global price for oil and companies in the U.S. stand to benefit for some time.

The net result is that cheaper energy in the U.S. is one of several factors that could fuel a secular bull market over the next decade.

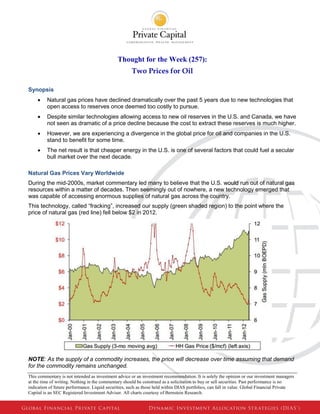

Natural Gas Prices Vary Worldwide

During the mid-2000s, market commentary led many to believe that the U.S. would run out of natural gas resources within a matter of decades. Then seemingly out of nowhere, a new technology emerged that was capable of accessing enormous supplies of natural gas across the country.

This technology, called “fracking”, increased our supply (green shaded region) to the point where the price of natural gas (red line) fell below $2 in 2012.

NOTE: As the supply of a commodity increases, the price will decrease over time assuming that demand for the commodity remains unchanged.

2. This commentary is not intended as investment advice or an investment recommendation. It is solely the opinion or our investment managers

at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Past performance is no

indication of future performance. Liquid securities, such as those held within DIAS portfolios, can fall in value. Global Financial Private

Capital is an SEC Registered Investment Adviser. All charts courtesy of Bernstein Research.

Although the U.S. has profited from cheaper natural gas, the rest of the world has realized little benefit from our supply increases because there is no world price for natural gas. The commodity is very difficult to transport so prices are local to the region in which the gas in extracted.

For example, natural gas is cheap in the U.S. but quite expensive in Japan. In fact, in many regions of the world, natural gas is even burned into the air at drill sites simply because drillers realize no economic value from capturing, transporting, and selling the gas!

Oil is Quite Different

The two most important types of crude oil are American West Texas Intermediate (WTI) and Brent North Sea Oil (Brent). WTI is known as the U.S. price for oil and is considered to be very high quality oil which can be used for refining a large portion of gasoline demand. Brent oil comes from 15 different oil fields in the North Sea (just north of mainland Europe) and is almost as high quality as WTI.

These two prices for oil effectively set a world price for oil and moved in lockstep for decades. Unlike natural gas, oil is easily shipped across the globe in tankers and hence, the price for oil was the consistent for most of the developed world – until recently.

The chart below tells a fascinating story. The black line represents the price of Brent oil, the green line is the price for WTI, and the green shaded region is the production of oil in the U.S. Since 2010, the production of oil in the U.S. has increased dramatically which has caused the relationship between Brent and WTI to diverge by a substantial amount.

This divergence, or spread, between Brent and WTI has widened for several reasons. One reason in particular involves a city in Oklahoma, named Cushing, where WTI oil is being delivered from:

1. Canada: Over the past few years, Canadian oil sands have become a vast resource for oil and the reserves are currently being transported to Cushing.

3. This commentary is not intended as investment advice or an investment recommendation. It is solely the opinion or our investment managers

at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Past performance is no

indication of future performance. Liquid securities, such as those held within DIAS portfolios, can fall in value. Global Financial Private

Capital is an SEC Registered Investment Adviser. All charts courtesy of Bernstein Research.

2. Fracking for Oil: Similar to how fracking has increased the supply of natural gas, new oil reserves are coming online here in the U.S., which are also being sent to Cushing.

Since there is no sufficient infrastructure in the U.S. to export this extra oil, the supply has been building rapidly in Cushing, OK. The net effect has driven the price of WTI oil down and those companies with the ability to access oil from Cushing and have it delivered economically have benefitted. On the other hand, Brent has risen due to production declines in the North Sea (lower supply means higher prices) and more direct exposure to unrests in the Middle East.

We believe that the net result of these factors will be a permanent spread between Brent and WTI oil - two world prices for oil instead of just one.

NOTE: You may be asking why the price of oil has not declined at the same rate as natural gas had years ago, despite an increase in supply. While fracking for natural gas is inexpensive, the technology behind fracking for oil, along with the complexity of accessing oil in these Canadian oil sands, is considerably more expensive which maintains a price floor. If the price of oil were to go too low, then companies would not be able to profit from these extraction processes.

Why Does All of This Matter?

We believe that we are at the beginning of a secular bull market that could persist for over a decade and a key component to our thesis involves cheap domestic energy.

Although we could list countless benefits to our economy from this energy revolution, the three most important are:

1. Cost/Competitive Advantage: At one point last year, the spread between Brent and WTI exceeded $25, meaning companies purchasing WTI oil were paying 25% less vs. those purchasing Brent for the same product. The benefit here is two-fold:

a. Increased Sales: By maintaining lower input costs, companies here can compete more effectively. Think about how companies in China for years have been able to offer products at a lower price due to cheaper labor. The same principle applies here – companies with access to cheaper oil can price products more competitively.

b. Higher Company Earnings: Companies with decreasing input costs can widen margins which increase earnings-per-share (EPS).

2. Job Creation: The energy is below our feet and we will need additional skilled labor to bring it to the surface. Job creation is one of the most powerful drivers of a strong economy because approximately 70% of our gross domestic product (GDP) consists of consumer spending.

3. Energy Independence: We believe that the idea of energy independence for the U.S. could become a reality in the next 15-20 years given these advances in technology.

There is certainly much controversy surrounding the future of energy in the U.S. However, as companies continue their migration to cheaper sources of energy, as many utilities have already moved from coal to cheaper natural gas to fuel power plants, we believe that our economy will greatly benefit along the way.