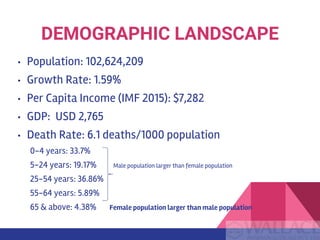

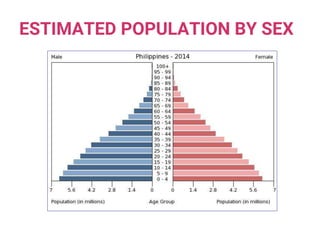

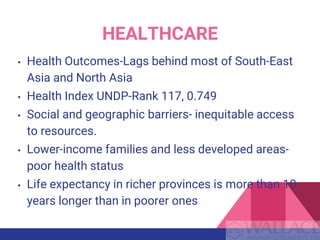

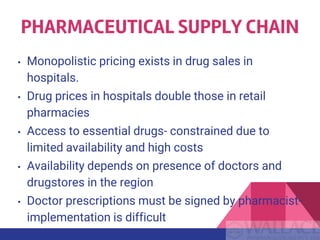

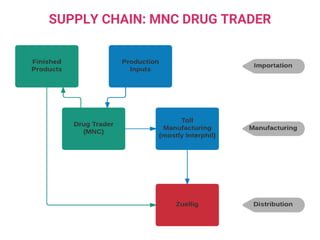

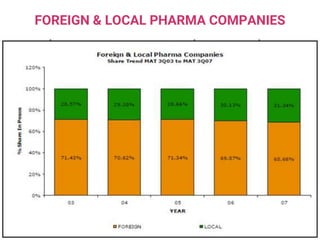

The document provides a comprehensive analysis of the pharmaceutical market in the Philippines, detailing its demographic landscape, healthcare system, and economic context. It emphasizes challenges such as high drug prices, limited access to essential medications, and a market heavily reliant on imports, with significant foreign pharmaceutical company presence. The report also highlights the need for regulatory reforms and the potential for growth in the local pharmaceutical sector, projected to reach $8 billion by 2020.

![CTEV [ clubfoot] DR ARUN LAL ,DR MOHAMED ASHRAF travancore medical college k...](https://cdn.slidesharecdn.com/ss_thumbnails/ctevclubfootdrarunlaldrmohamedashraftravancoremedicalcollegekollamkeralaindia-260208063247-18fc466c-thumbnail.jpg?width=640&height=640&fit=bounds)