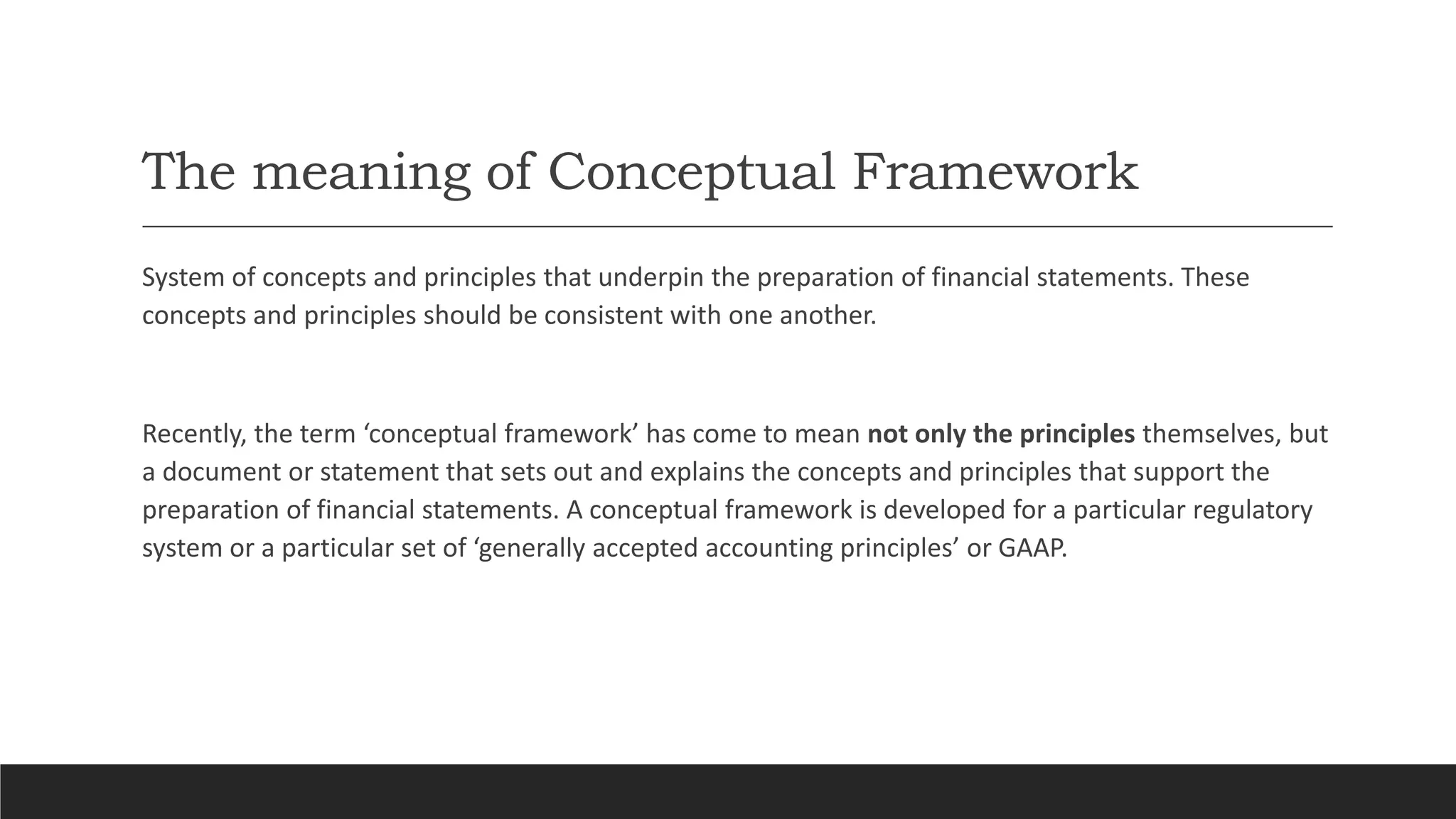

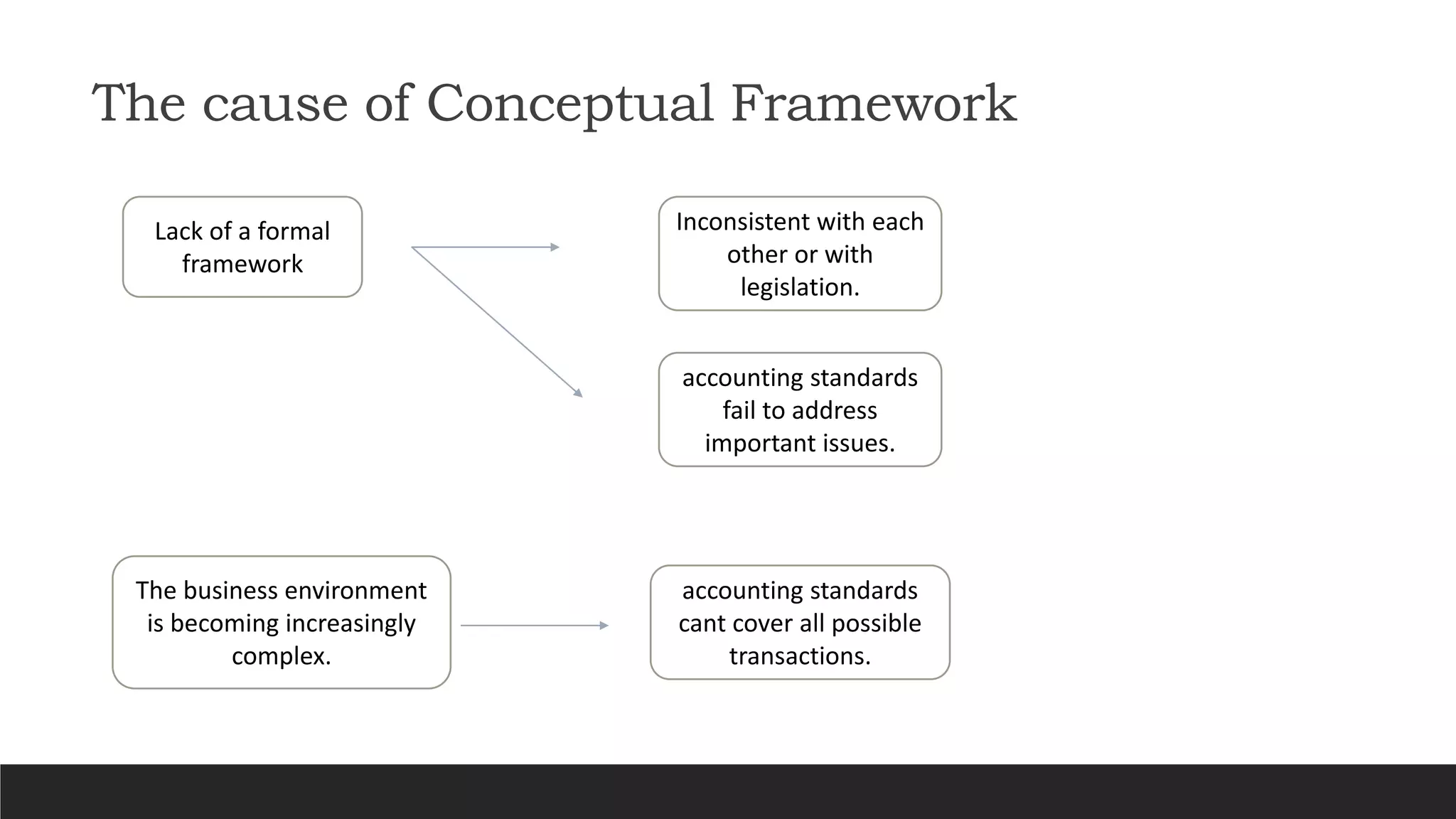

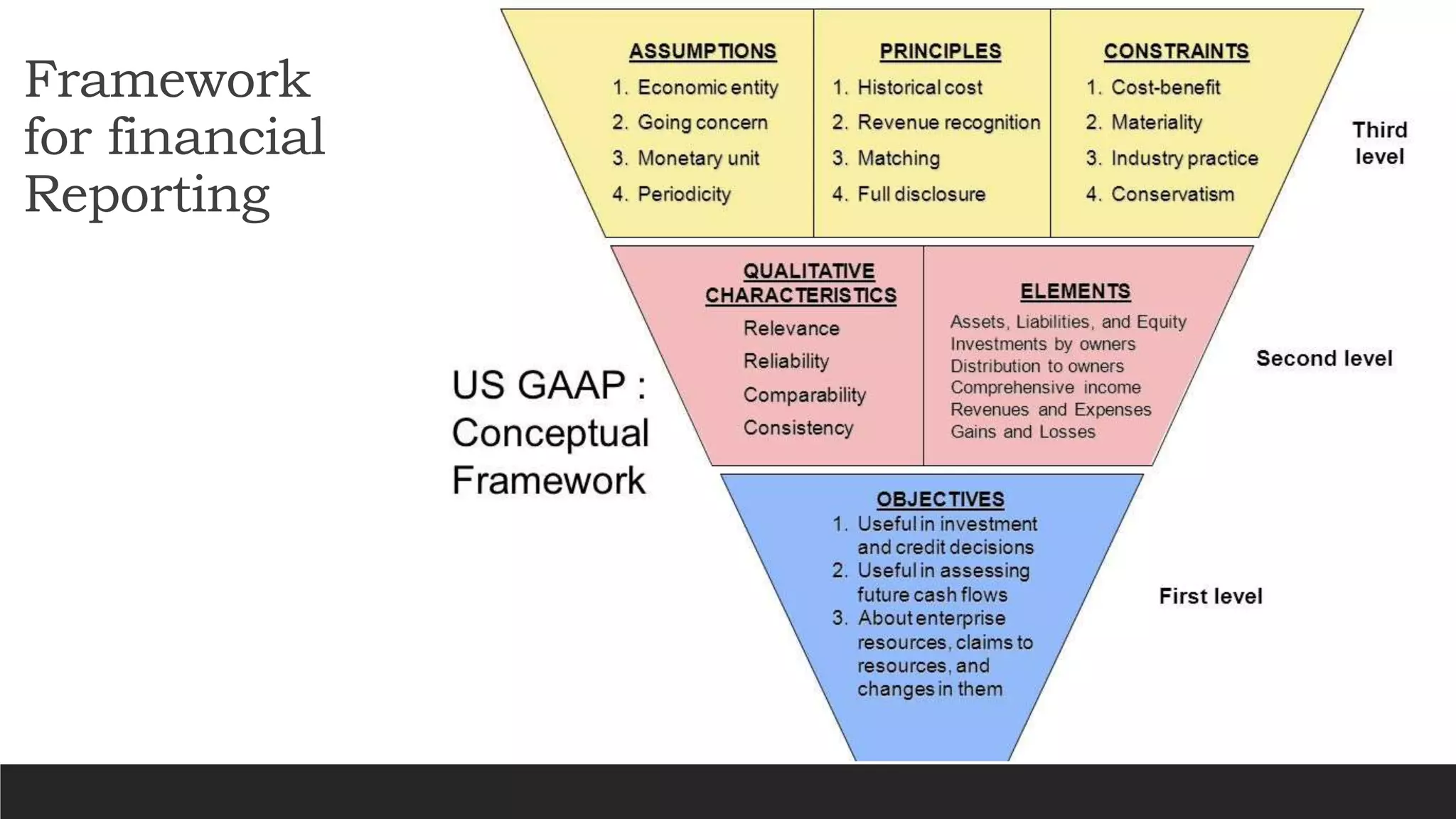

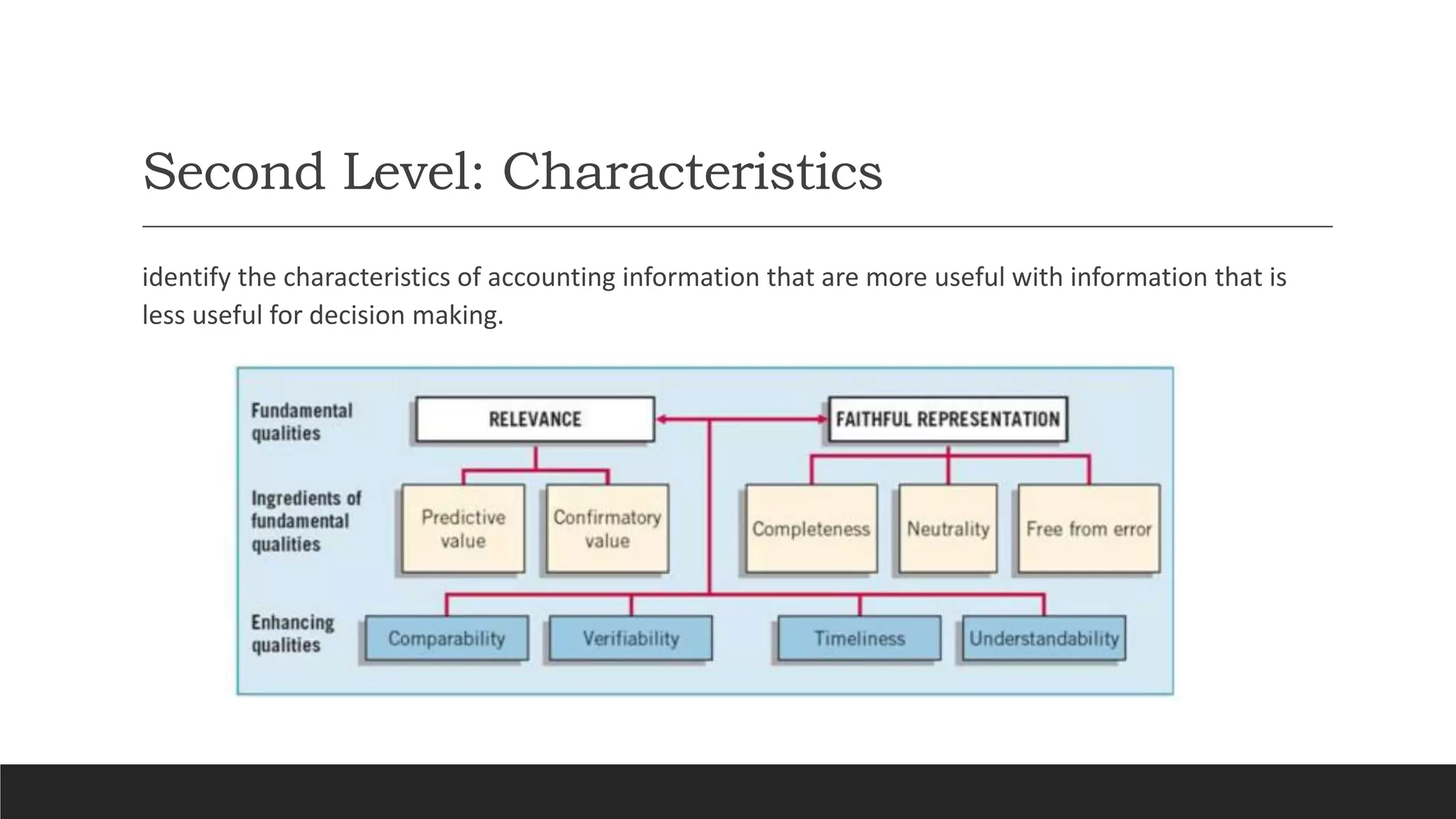

The conceptual framework establishes the concepts and principles that underlie financial reporting. It defines elements like assets, liabilities, and equity, and provides guidance on recognition, measurement, and disclosure in financial statements. The framework ensures accounting standards are consistent and addresses important issues. It is developed by regulatory bodies like the IASB to provide a standardized set of principles for preparing financial statements that are useful to investors and creditors for decision making.