Conceptual Framework

• Aconceptual framework, in the field we are

concerned with, is a statement of generally

accepted theoretical principles which form the

frame of reference for financial reporting.

• These theoretical principles provide the basis for the

development of new accounting standards and the

evaluation of those already in existence. The

financial reporting process is concerned with

providing information that is useful in the business

and economic decision-making process

3.

Conceptual Framework

• Thereforea conceptual framework will form

the theoretical basis for determining which

events should be accounted for, how they

should be measured and how they should be

communicated to the user. Although it is

theoretical in nature, a conceptual framework

for financial reporting has highly practical

final aims.

4.

Conceptual Framework

• Thedanger of not having a conceptual

framework is demonstrated in the way some

countries' standards have developed over recent

years; standards tend to be produced in a

haphazard and fire-fighting approach. Where an

agreed framework exists, the standard-setting

body act as an architect or designer, rather than

a fire-fighter, building accounting rules on the

foundation of sound, agreed basic principles.

5.

Conceptual Framework

• Thelack of a conceptual framework also

means that fundamental principles are tackled

more than once in different standards, thereby

producing contradictions and inconsistencies

in basic concepts, such as those of prudence

and matching. This leads to ambiguity and it

affects the true and fair concept of financial

reporting.

6.

Conceptual Framework

• Aconceptual framework can also bolster

standard setters against political pressure from

various 'lobby groups' and interested parties.

Such pressure would only prevail if it was

acceptable under the conceptual framework.

7.

Generally Accepted AccountingPractice

(GAAP)

• GAAP signifies all the rules, from whatever

source, which govern accounting.

• In individual countries this is seen primarily as

a combination of:

• National company law

• National accounting standards

• Local stock exchange requirements

8.

Generally Accepted AccountingPrinciple

(GAAP)

• .

Although those sources are the basis

for the GAAP of individual countries,

the concept also includes the

effects of non-mandatory sources such

as:

• International accounting standards

• Statutory requirements in other

countries

9.

The IASB's Framework

•The Framework provides the conceptual

framework for the development of IFRSs/IASs.

• In July 1989 the IASB (then IASC) produced a

document, Framework for the preparation

and presentation of financial statements

('Framework').

10.

The IASB's Framework

•The Framework consists of several sections or chapters,

following on after a preface and introduction.

These chapters are as follows.

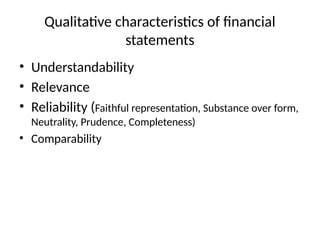

• The objective of financial statements

• Underlying assumptions

• Qualitative characteristics of financial statements

• The elements of financial statements

• Recognition of the elements of financial statements

• Measurement of the elements of financial statements

• Concepts of capital and capital maintenance

11.

IASB’s standard settingprocess

1. Setting the agenda: The IASB identifies a

subject (mainly by reference to the needs of

the investors). The IASB can also add topics

to its work plan if necessary between agenda

consultations. This can include topics

following post-implementation reviews of

Standards; the IFRS Interpretations

Committee may also request the IASB review

an issue.

12.

IASB’s standard settingprocess

2. Planning the project: After considering the

nature of the issues and the level of interest

among constituents, the IASB may establish a

working group at this stage.

13.

IASB’s standard settingprocess

3. Developing and publishing the discussion

paper

4. Developing and publishing the exposure

draft:for public comment, which is a draft

version of the intended standard. To gather

additional evidence, members of the IASB and

IFRS Foundation technical staff consult with a

range of stakeholders from all over the world.

IASB’s standard settingprocess

• 6. After the standard is issued, the staff and the

IASB members hold regular meetings with

interested parties, to help understand

unanticipated issues related to the practical

implementation and potential impact of its

proposals. If issues arise, the IFRS Interpretations

Committee may decide to create an IFRIC

Interpretation of the Accounting Standard or

recommend a narrow-scope amendment

16.

Recognition and Measurement

•Recognition. The process of incorporating in the

statement of financial position or statement of

comprehensive income an item that meets the

definition of an element and satisfies the following

criteria for recognition:

• (a) it is probable that any future economic benefit

associated with the item will flow to or from the

entity; and

• (b) the item has a cost or value that can be measured

with reliability.

17.

Measurement.

• The processof determining the monetary

amounts at which the elements of the

financial statements are to be recognized and

carried in the statement of financial position

and statement of comprehensive income.

18.

Measurement of theelements of financial

statements

• A number of different measurement bases are

used in financial statements. They include

• Historical cost

• Current cost

• Realizable (settlement) value

• Present value of future cash flows

19.

Measurement of theelements of financial

statements

• Historical cost. Assets are recorded at the amount

of cash or cash equivalents paid or the fair value

of the consideration given to acquire them at the

time of their acquisition. Liabilities are recorded

at the amount of proceeds received in exchange

for the obligation, or in some circumstances (for

example, income taxes), at the amounts of cash or

cash equivalents expected to be paid to satisfy

the liability in the normal course of business.

20.

Measurement of theelements of financial

statements

• Current cost. Assets are carried at the amount

of cash or cash equivalents that would have to

be paid if the same or an equivalent asset was

acquired currently.

• Liabilities are carried at the undiscounted

amount of cash or cash equivalents that would

be required to settle the obligation currently.

21.

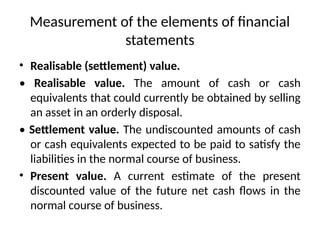

Measurement of theelements of financial

statements

• Realisable (settlement) value.

• Realisable value. The amount of cash or cash

equivalents that could currently be obtained by selling

an asset in an orderly disposal.

• Settlement value. The undiscounted amounts of cash

or cash equivalents expected to be paid to satisfy the

liabilities in the normal course of business.

• Present value. A current estimate of the present

discounted value of the future net cash flows in the

normal course of business.

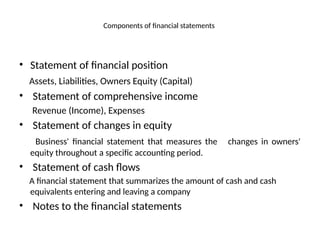

Components of financialstatements

• Statement of financial position

Assets, Liabilities, Owners Equity (Capital)

• Statement of comprehensive income

Revenue (Income), Expenses

• Statement of changes in equity

Business' financial statement that measures the changes in owners'

equity throughout a specific accounting period.

• Statement of cash flows

A financial statement that summarizes the amount of cash and cash

equivalents entering and leaving a company

• Notes to the financial statements

24.

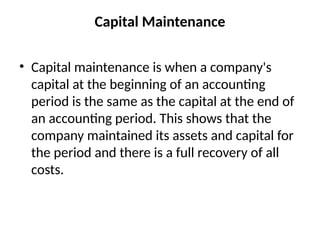

Capital Maintenance

• Capitalmaintenance is when a company's

capital at the beginning of an accounting

period is the same as the capital at the end of

an accounting period. This shows that the

company maintained its assets and capital for

the period and there is a full recovery of all

costs.

25.

Capital Maintenance

• Tocalculate the profit of a company, the

capital of a company must be restored to its

initial level and an additional monetary

amount or net assets recorded at the end of a

period. It is the excess amount that is

calculated as the company's profit.

26.

Financial Capital Maintenance

•Financial capital maintenance deals with the actual funds

that a company has. When the funds are adequately

maintained in such a way that the amount recorded at the

end of an accounting period is more than the amount

recorded at the beginning of the period, profit is

recorded.

• The International Financial Reporting Standards (IFRS)

when calculating profit earned through financial capital

maintenance excludes contributions and distributions. The

Financial capital maintenance measures profit using net

assets, excess net assets translate to profit.

27.

Physical Capital Maintenance

•The ability and effectiveness of a business to

maintain cash flows, including managing

assets that generate revenue for the business

are known as physical capital maintenance.

Unlike financial capital maintenance, physical

capital maintenance is not concerned with the

actual funds or money of a firm, rather, it pays

attention to how well the business maintains

its income-generating assets.

28.

Physical Capital Maintenance

•Physical capital maintenance also excludes

contributions and distributions when

determining the profit earned by a firm at the

end of an accounting period.

Editor's Notes

#26 All the inflows such as the sale of stock to shareholders, the addition of capital from owners, and payment of dividends to shareholders payment of bonus to shareholders are excluded.

#27 any amount adjusted towards any amount paid to owners during the year or any amount raised by the owner excluded