Download to read offline

![ “In an attempt to achieve further growth,

Enron pursued a diversification strategy. The

company owned and operated a variety of

assets including gas pipelines, electricity

plants, pulp and paper plants, water plants,

and broadband services across the globe. The

corporation also gained additional revenue by

trading contracts for the same array of

products and services with which it was

involved.[10]”](https://image.slidesharecdn.com/theenronscandal-231229200733-8ba29c82/75/THE-ENRON-SCANDAL-ppt-4-2048.jpg)

![ Enron and other energy suppliers earned

profits by providing services such as

wholesale trading and risk management in

addition to building and maintaining electric

power plants, natural gas pipelines, storage,

and processing facilities.

Service providers, when classified as agents,

are able to report trading and brokerage fees

as revenue.[18] This is called the “agent

model” and is used by most trading

institutions (ie. Merrill Lynch)](https://image.slidesharecdn.com/theenronscandal-231229200733-8ba29c82/75/THE-ENRON-SCANDAL-ppt-22-2048.jpg)

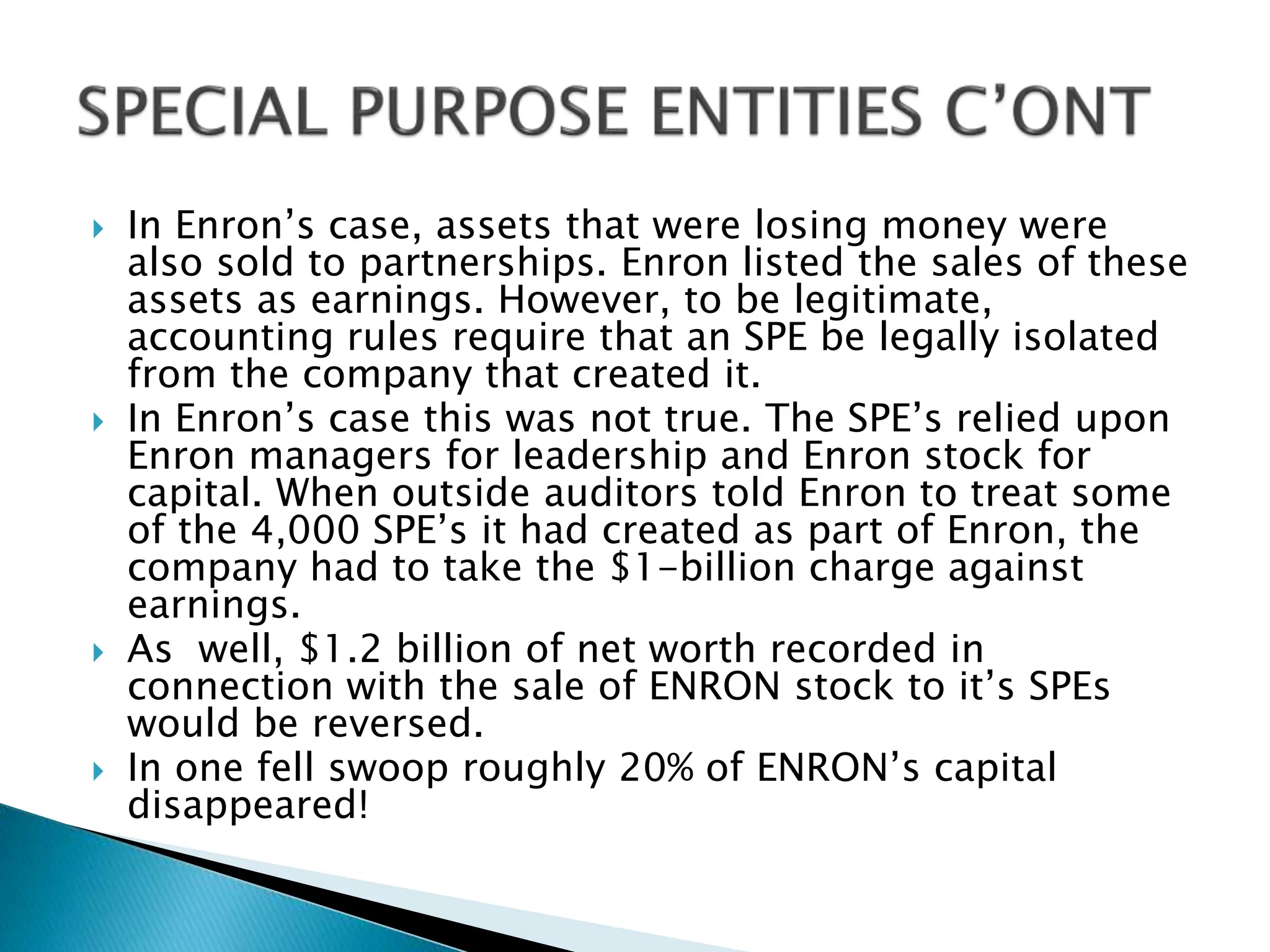

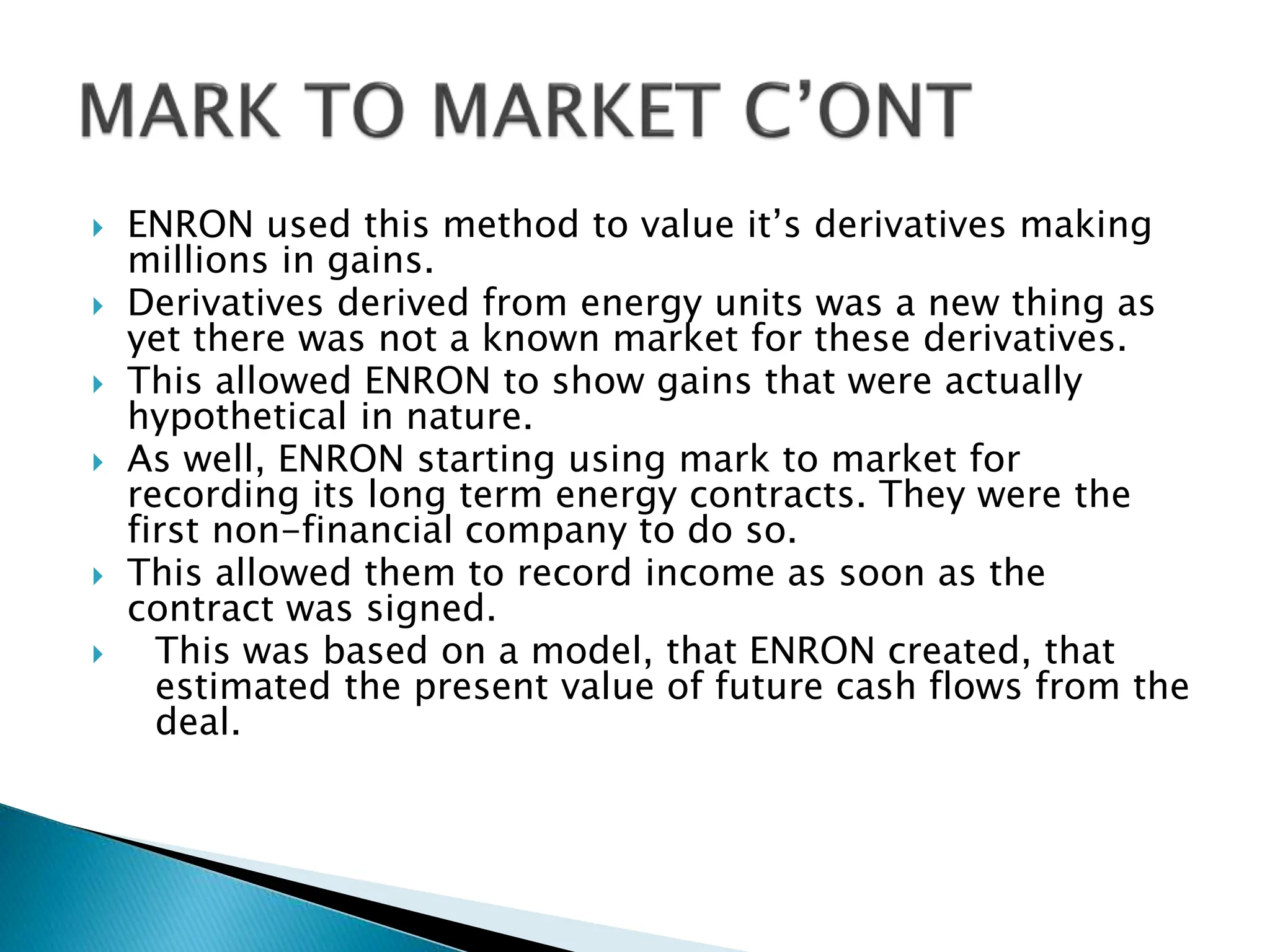

Enron was an energy company that grew rapidly in the 1990s but collapsed in 2001 due to widespread corporate fraud. Top executives, including CEO Ken Lay and CFO Andrew Fastow, had set up off-balance sheet partnerships and used mark-to-market accounting to hide billions in debts and inflate profits. When Enron's fraudulent activities came to light after an accounting scandal, the company filed for bankruptcy in 2001, resulting in losses of over $60 billion for shareholders.