Download as PDF, PPTX

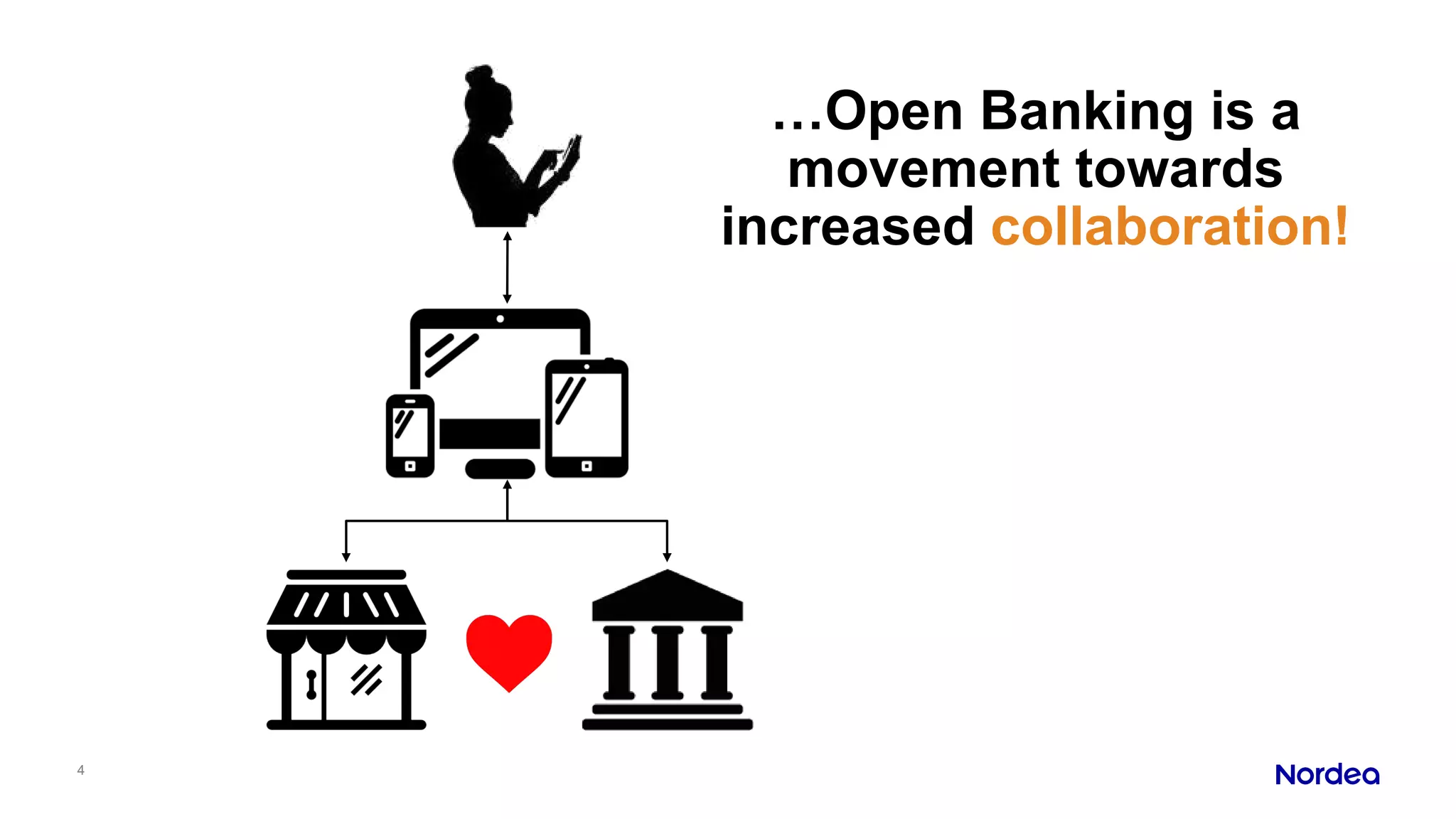

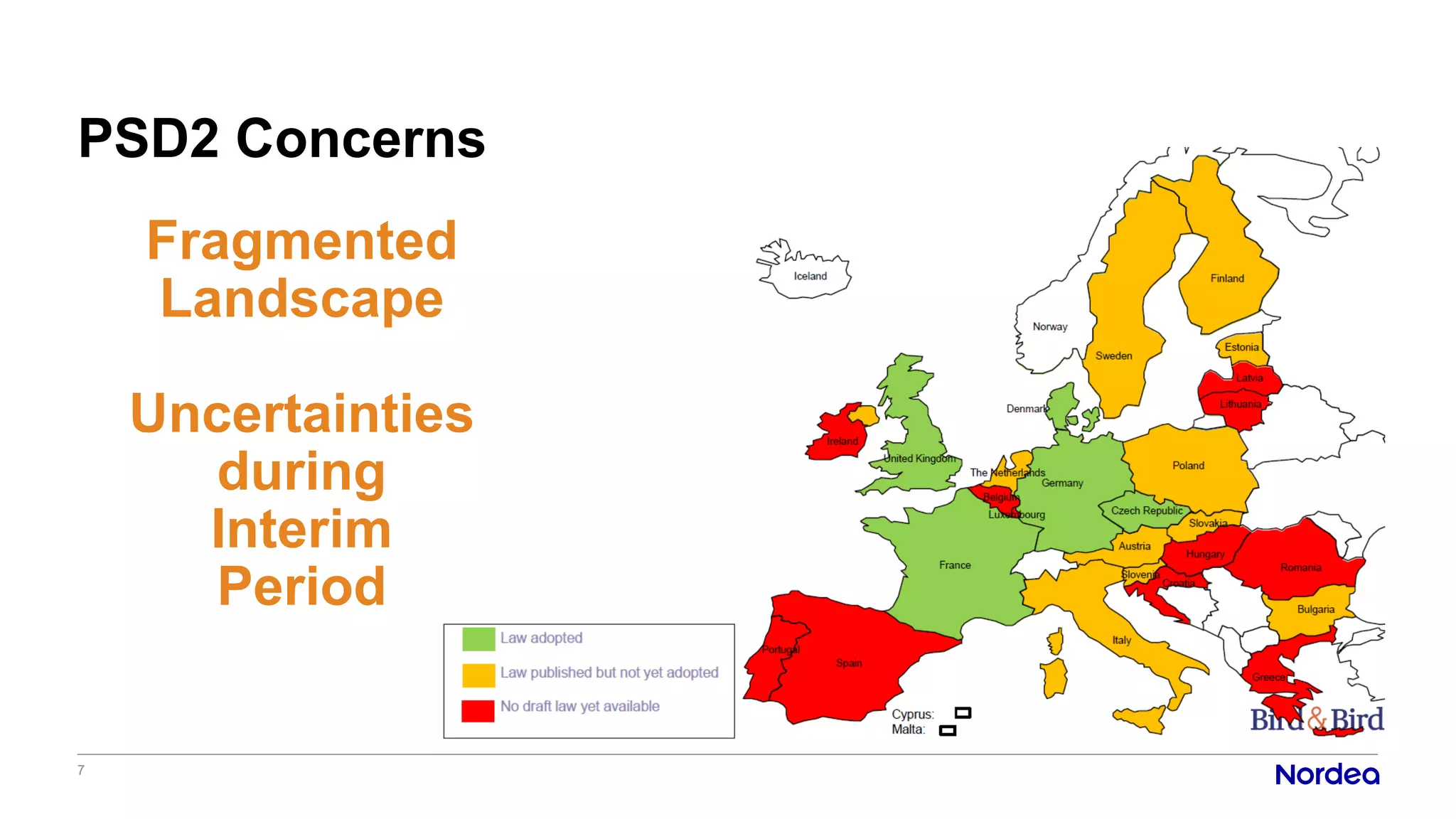

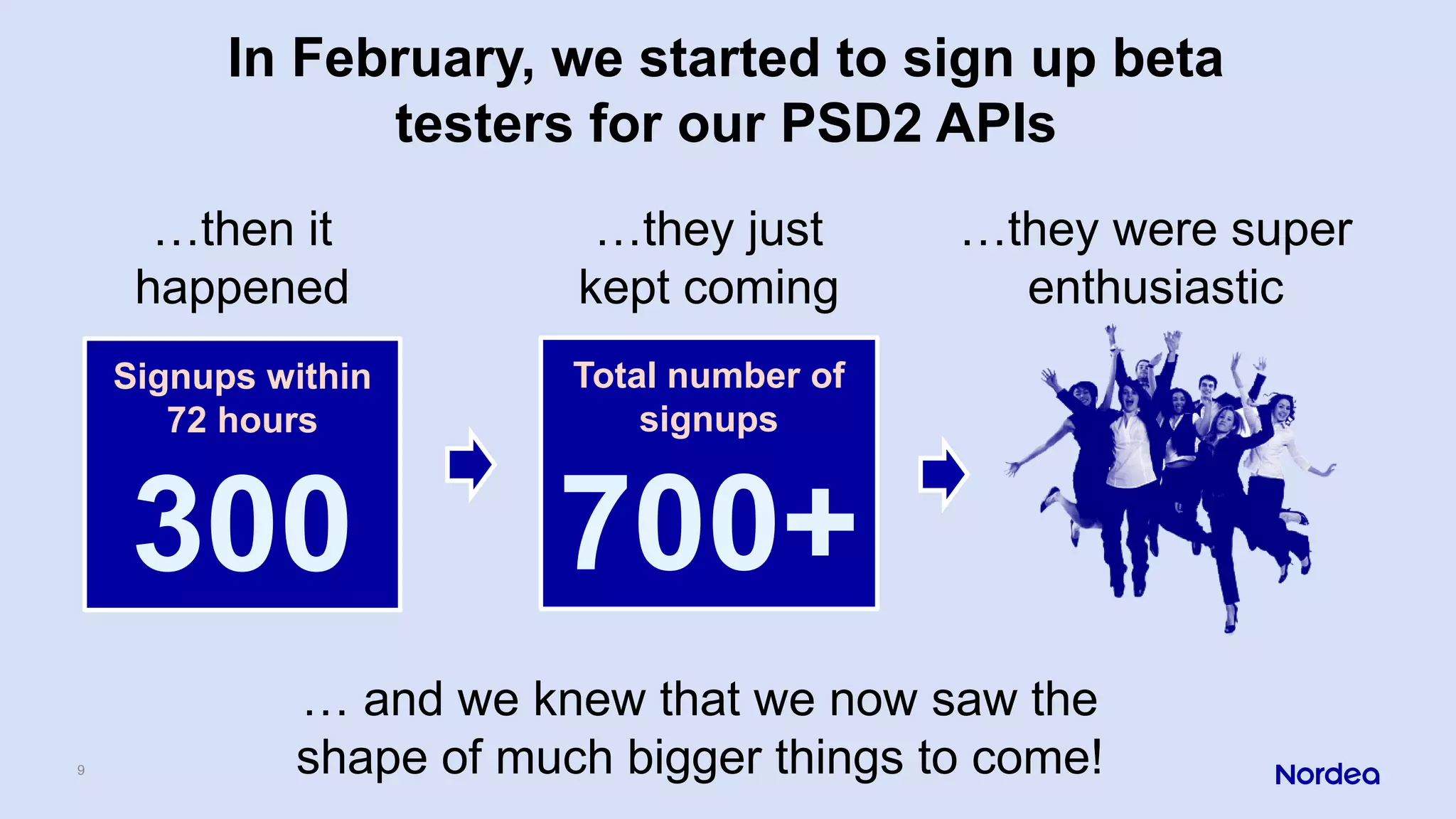

Open Banking will increase collaboration and competition in the banking industry. While PSD2 empowers non-banks, Open Banking is about changing mindsets and working together. Nordea started signing up beta testers for their PSD2 APIs in February and saw unexpected interest, with over 700 signups in just 72 hours. In response, Nordea accelerated their Open Banking plans and launched partner pilots a year early.

![[WSO2 Integration Summit Brazil 2019] Open Banking](https://cdn.slidesharecdn.com/ss_thumbnails/wso2integrationsummitbrazil2019openbanking-191118040222-thumbnail.jpg?width=640&height=640&fit=bounds)

![[WSO2Con EU 2018] WSO2 Open Banking, So Good I Bought it Twice](https://cdn.slidesharecdn.com/ss_thumbnails/wso2coneu2018-openbankingsogoodboughttwice-v0-181113094843-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Workshop] Business Benefits and Digital Transformation through Open Banking](https://cdn.slidesharecdn.com/ss_thumbnails/businessbenefitsanddigitaltransformationthroughopenbanking-191029105735-thumbnail.jpg?width=640&height=640&fit=bounds)