Download to read offline

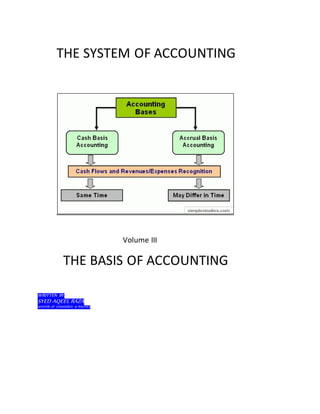

The document outlines the basis of accounting, focusing on cash and accrual methods, detailing their operations, advantages, and drawbacks. It emphasizes the importance of recognizing transactions accurately to present a clear financial picture and discusses methods for bank reconciliation. Additionally, it describes various bank account types, bank transactions, and common discrepancies that occur during reconciliation.

![W@=D@ [what is that?]](https://cdn.slidesharecdn.com/ss_thumbnails/wd-110922100250-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)