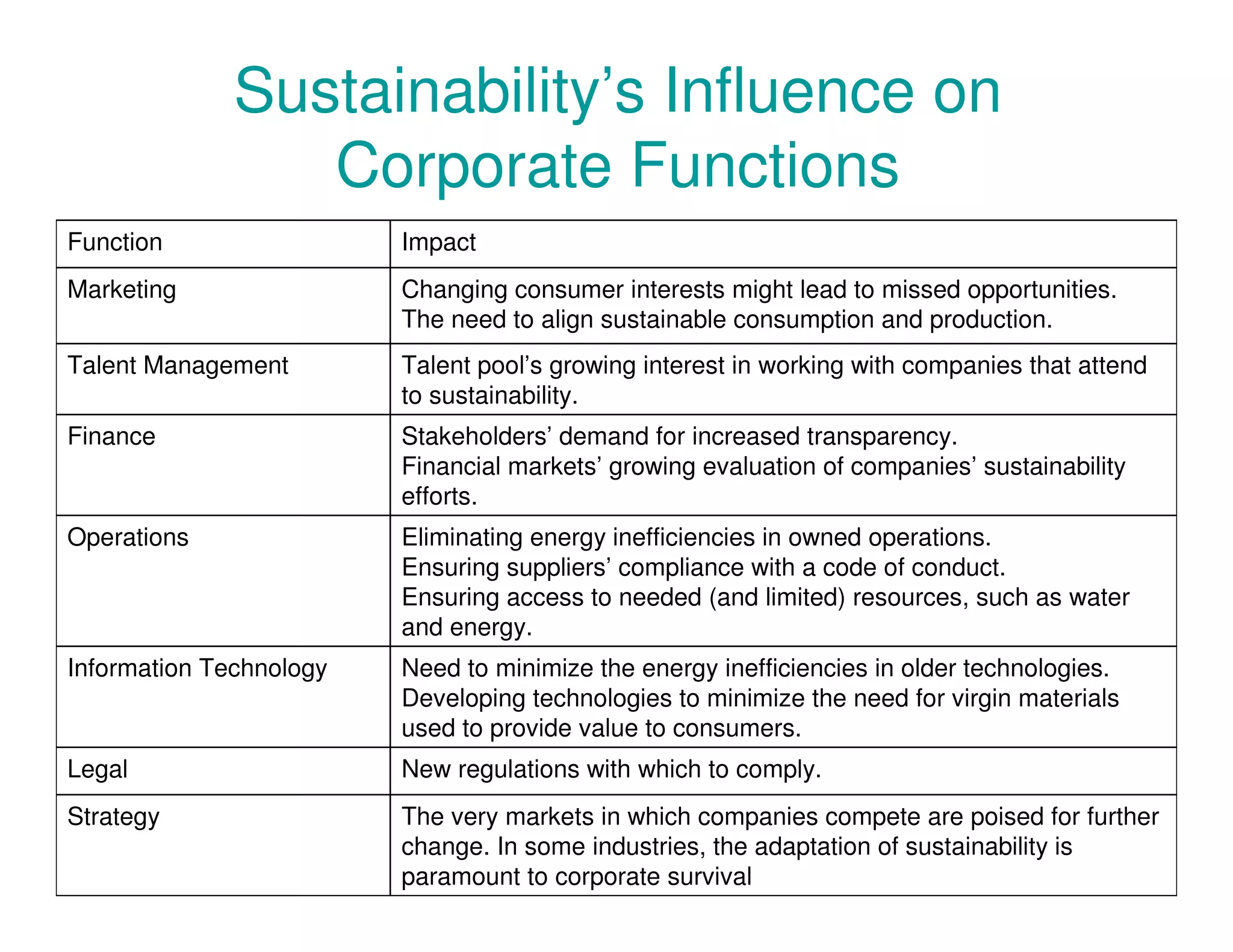

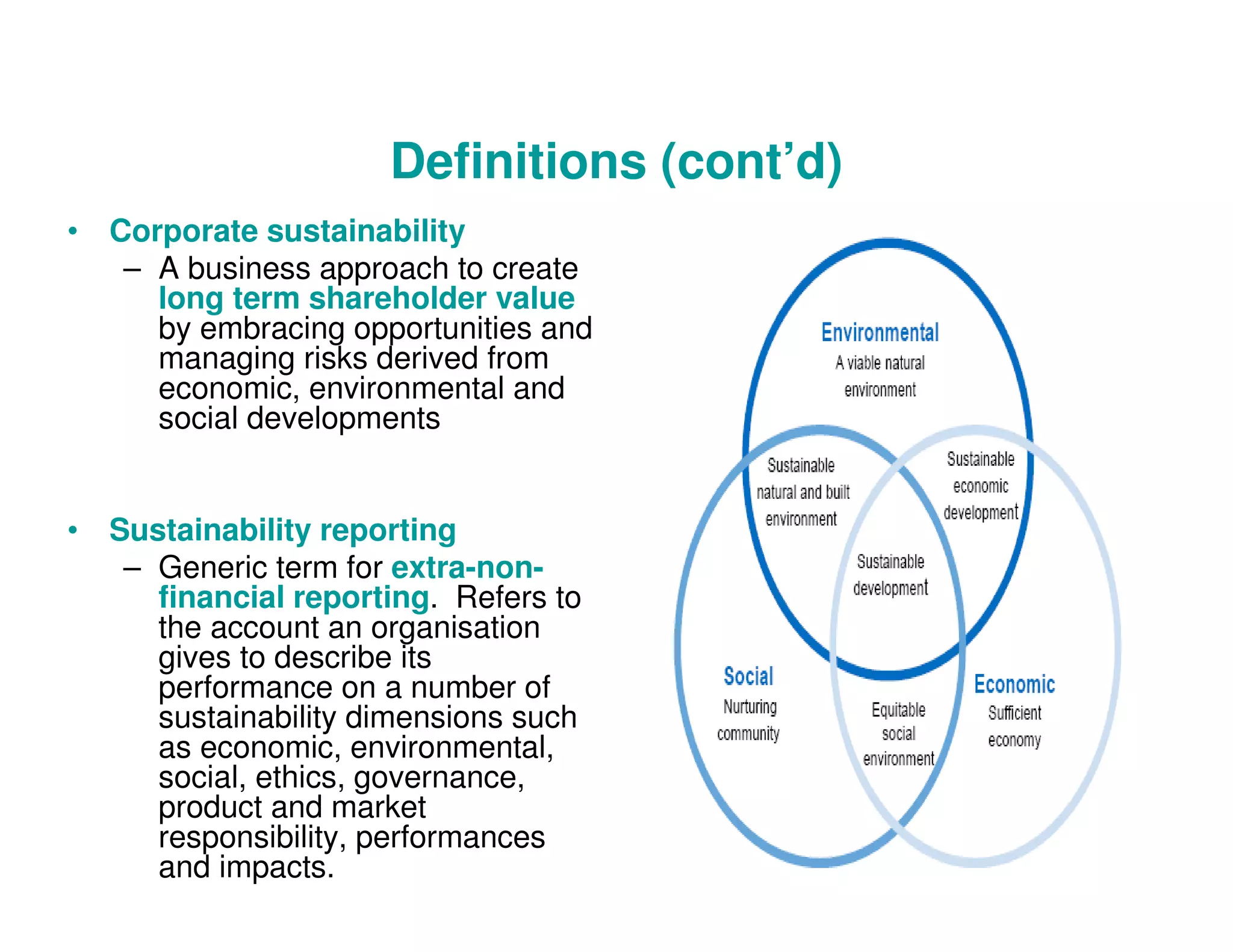

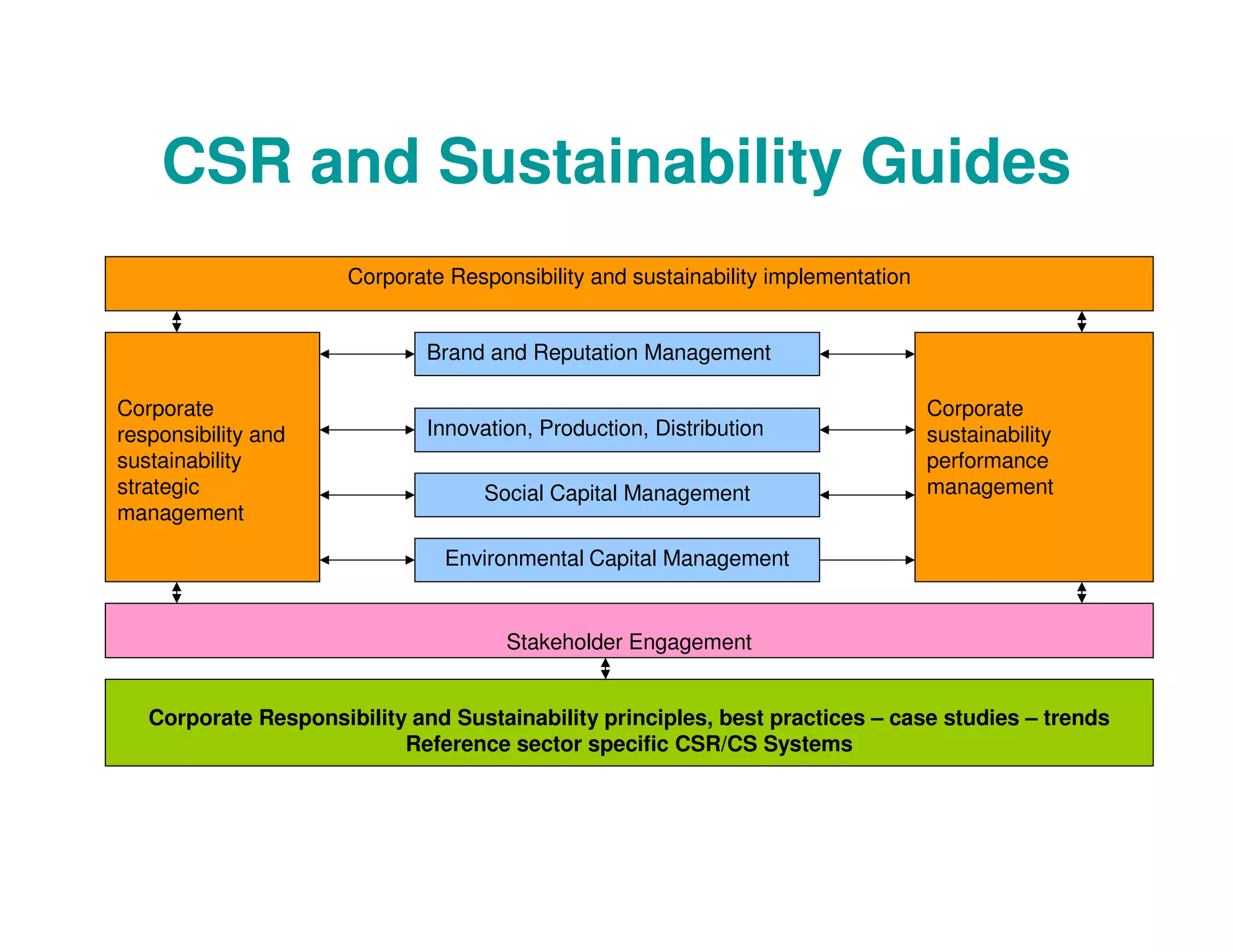

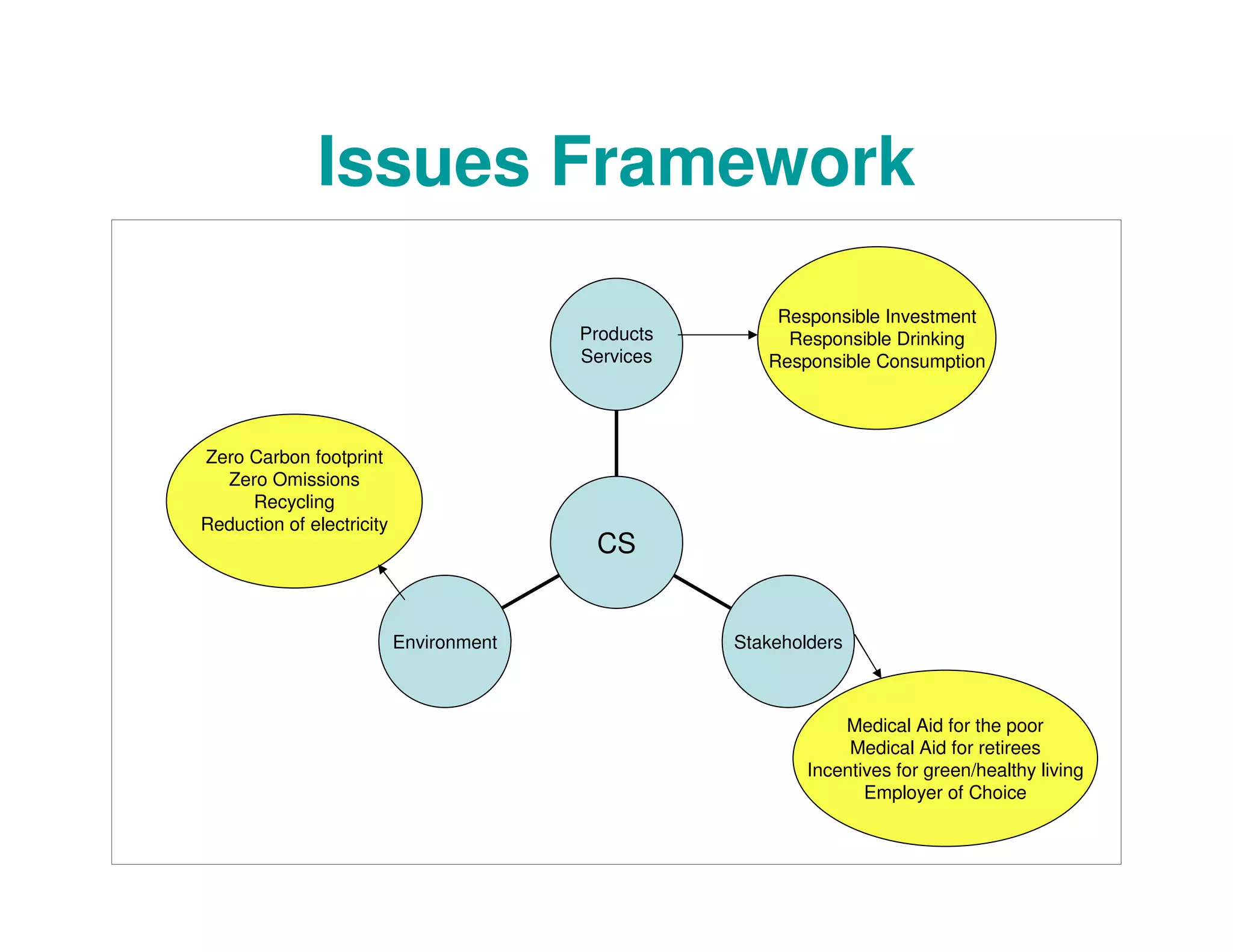

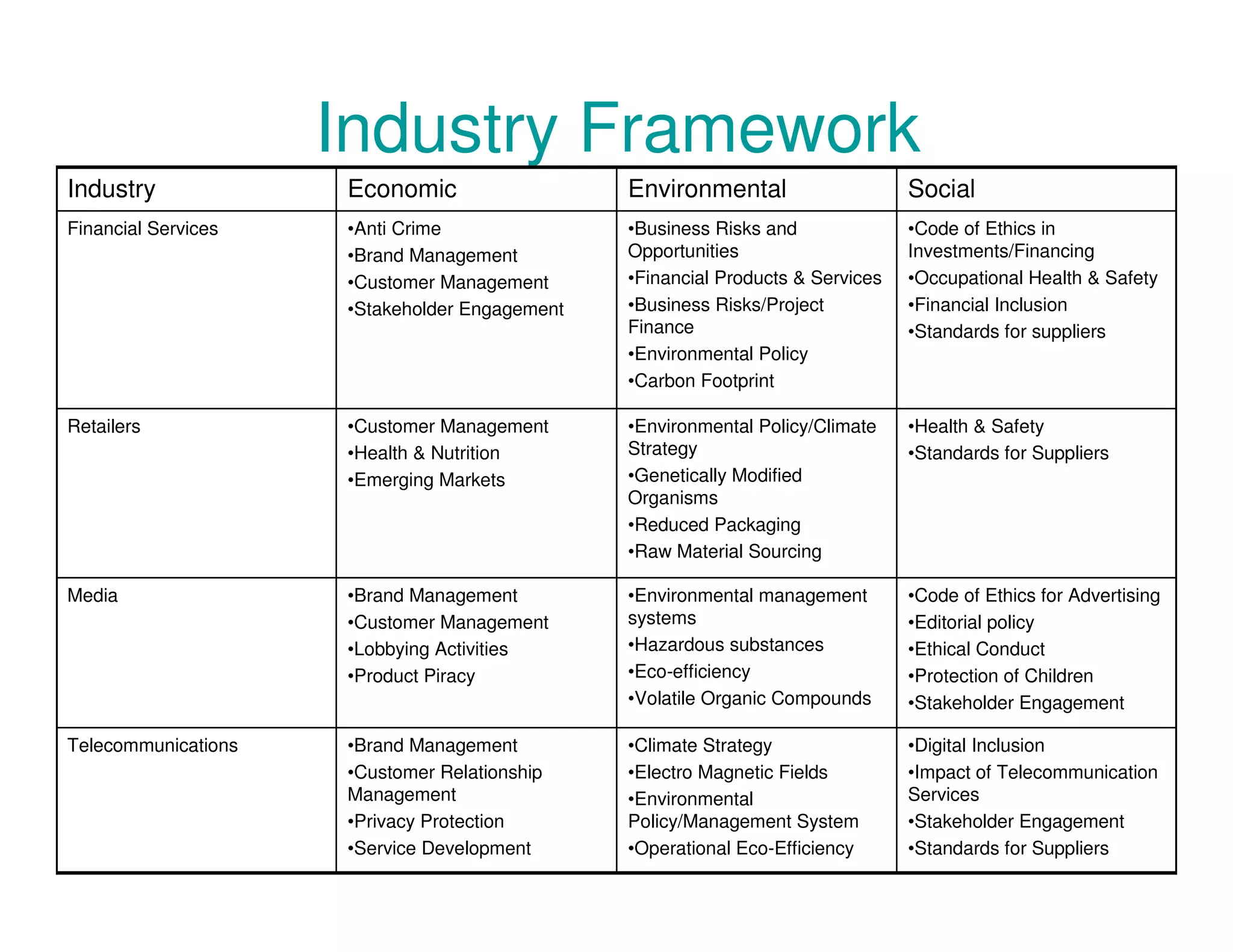

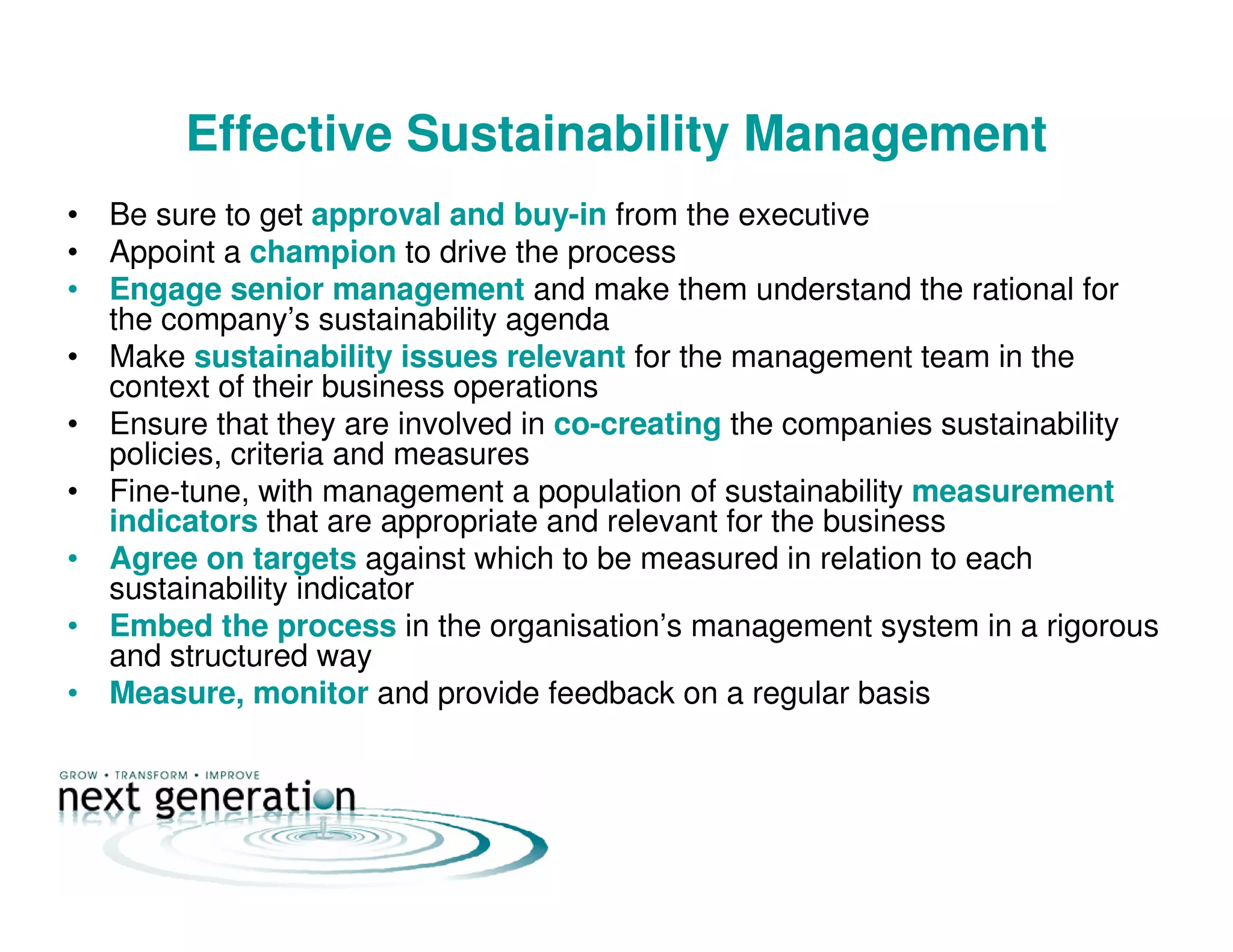

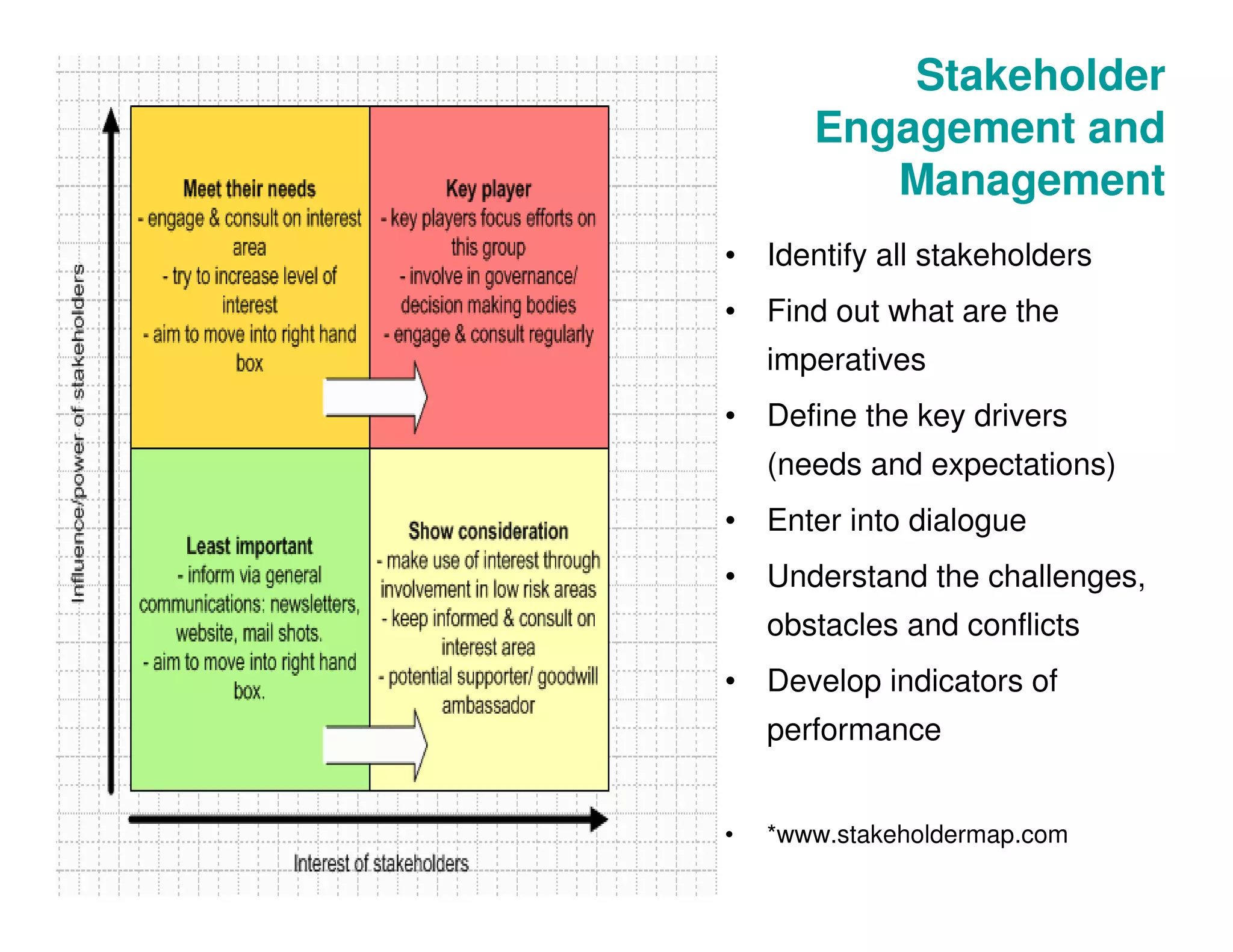

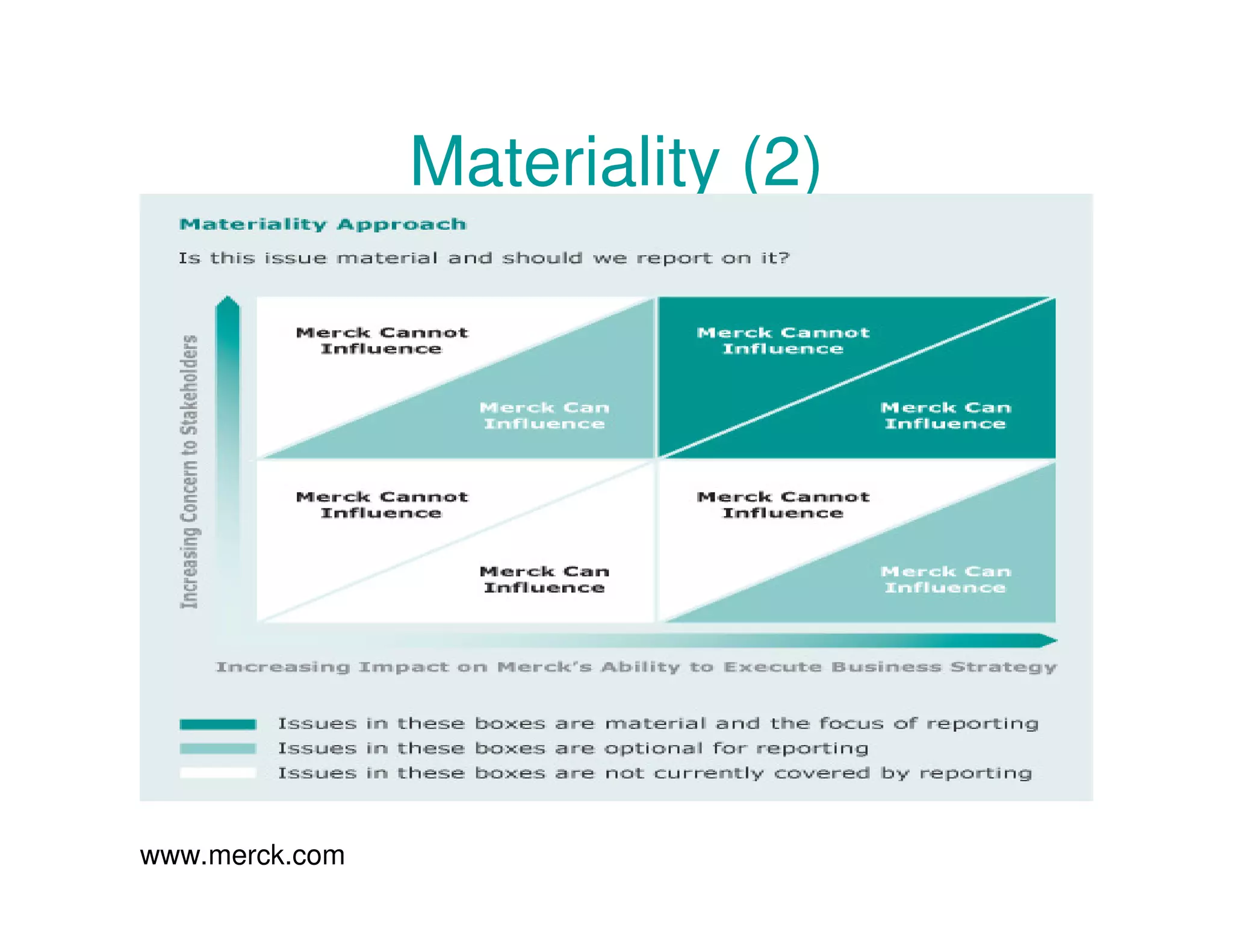

This document provides an overview of corporate responsibility, sustainability, and sustainability reporting. It defines key terms, discusses drivers and challenges, and outlines frameworks for implementing sustainability strategies. The key messages are that sustainability is important for managing risks and opportunities, meeting stakeholder demands, and gaining competitive advantages through innovation. Frameworks emphasize understanding impacts across economic, social, and environmental dimensions.

![Chapter 3 Total Quality Management [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter3totalqualitymanagementautosaved-190709035452-thumbnail.jpg?width=640&height=640&fit=bounds)