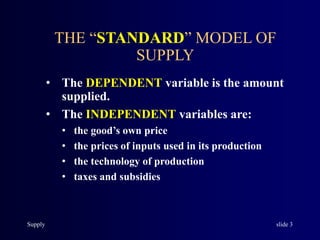

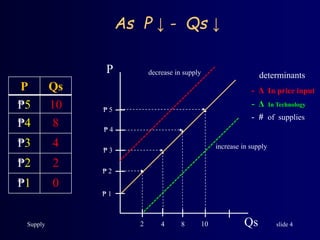

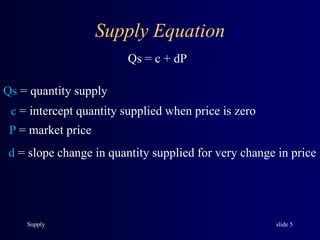

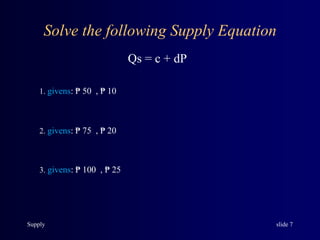

The document discusses the standard model of supply. It defines supply as a producer phenomenon and explains that the dependent variable in the supply model is the quantity supplied, while the independent variables are the good's own price, input prices, technology, and taxes/subsidies. It presents the law of supply graphically and shows that as price decreases, quantity supplied also decreases. The document also introduces the supply equation, where quantity supplied (Qs) equals the intercept (c) plus the slope (d) multiplied by price (P). It provides examples of using the supply equation to solve for the slope (d) given two data points of price and quantity supplied.