Downloaded 50 times

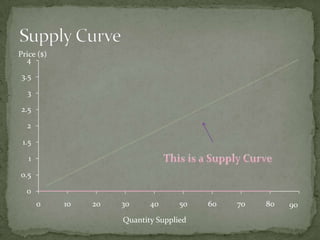

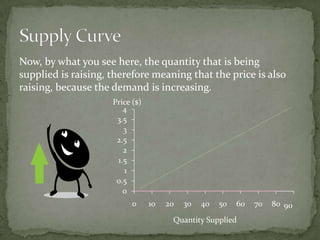

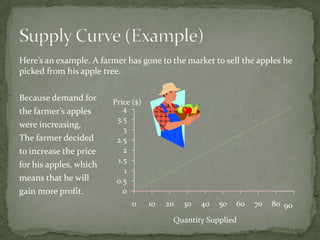

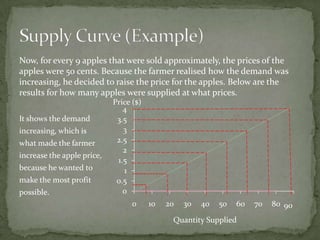

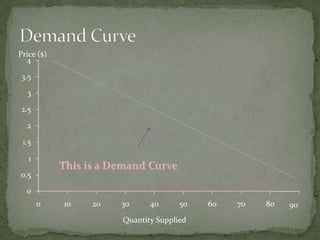

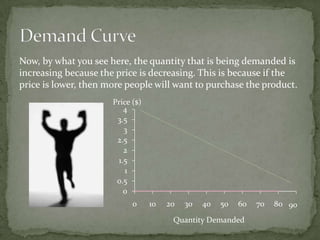

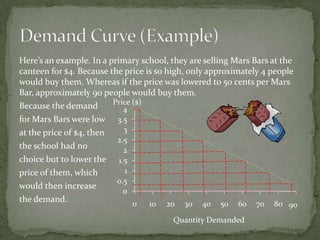

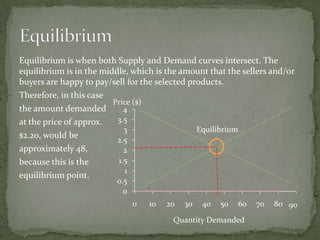

The document discusses supply and demand from the perspective of both businesses and consumers. It defines supply as the amount producers are willing to supply at a given price, and demand as the amount consumers are willing to buy at a given price. Equilibrium occurs when supply and demand are equal. The document provides an example of a farmer who increased the price of apples in response to increasing demand, resulting in higher profits. It also discusses how decreasing price can increase demand. Equilibrium is reached at the point where the supply and demand curves intersect.