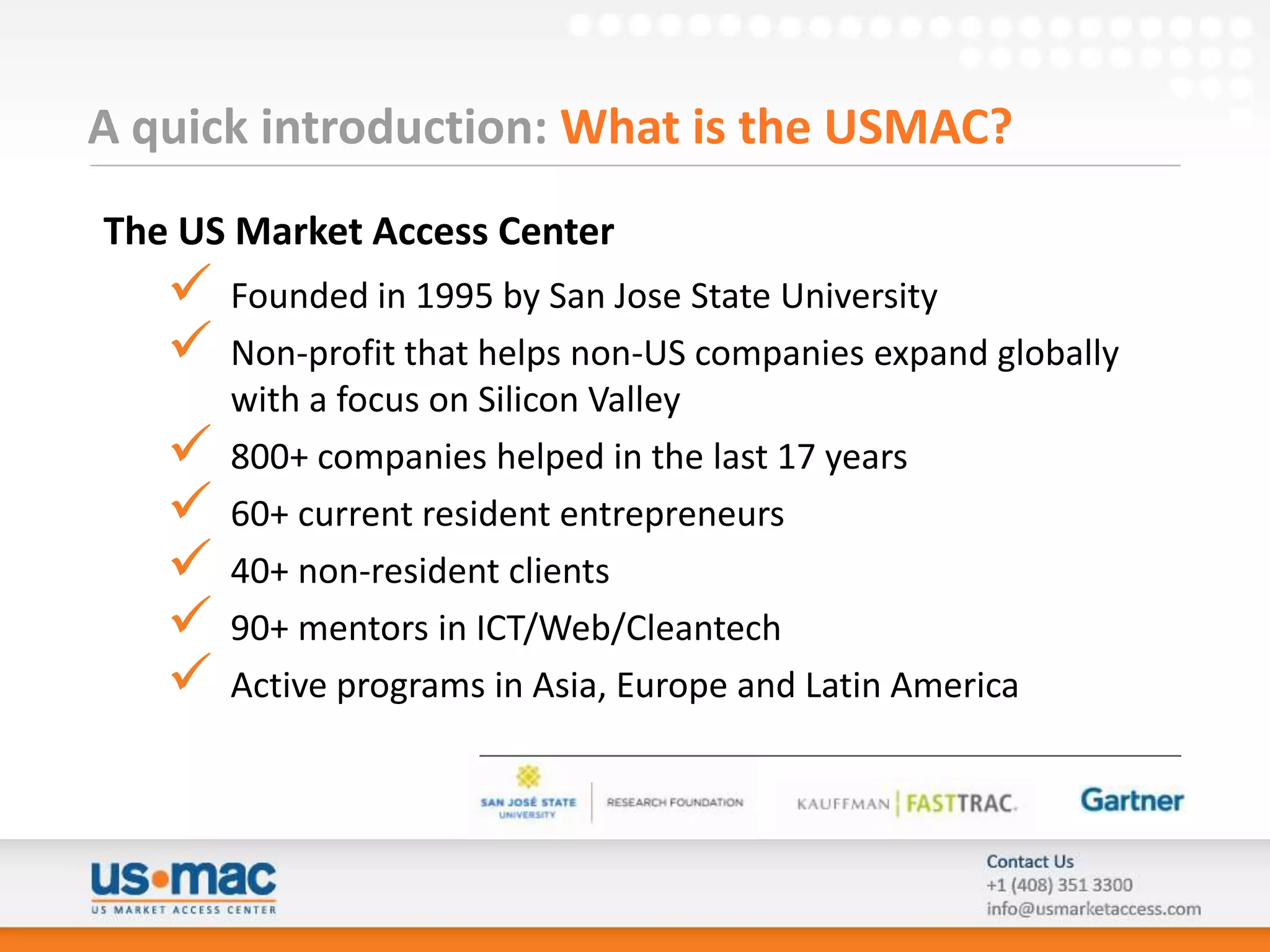

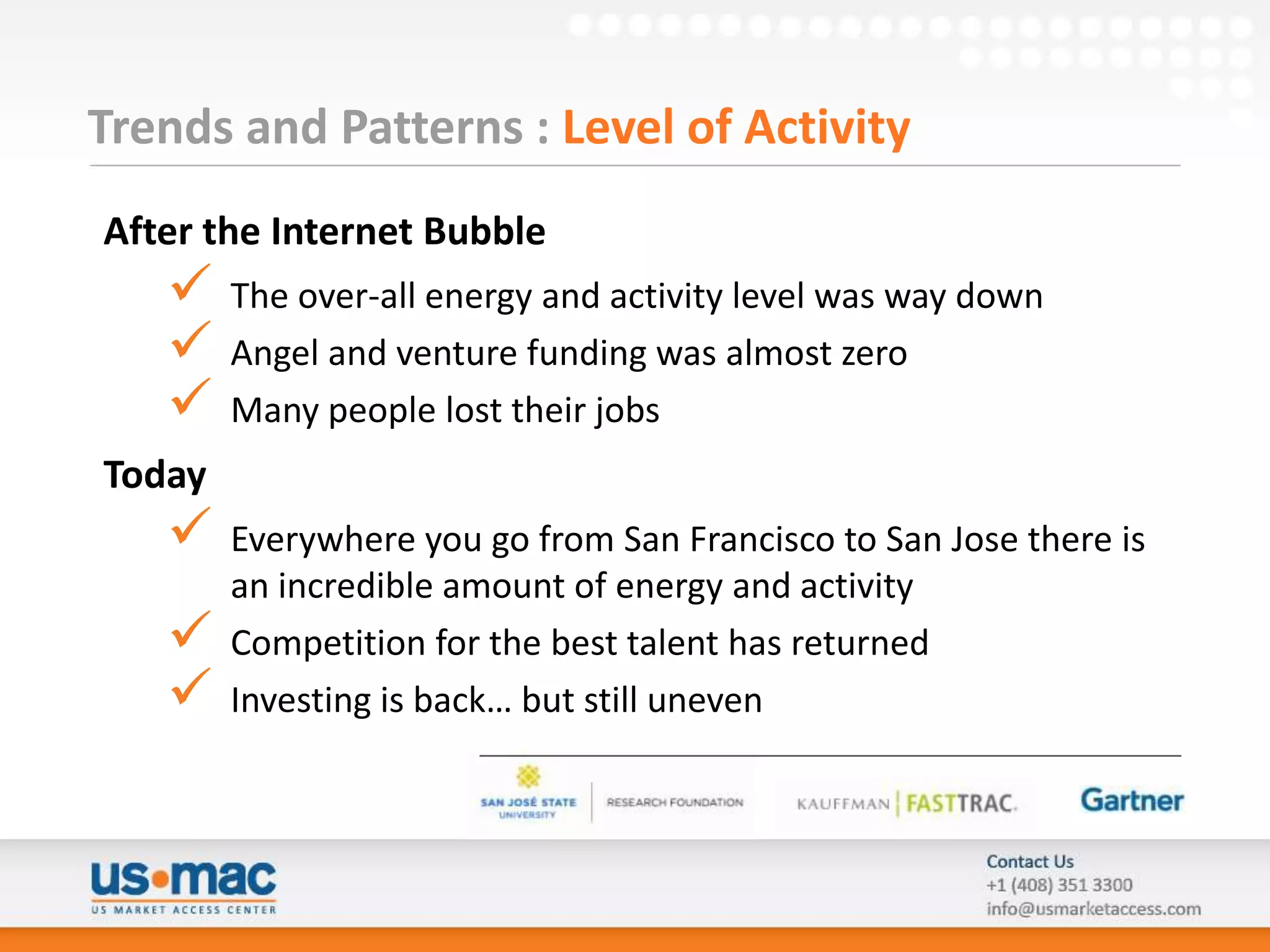

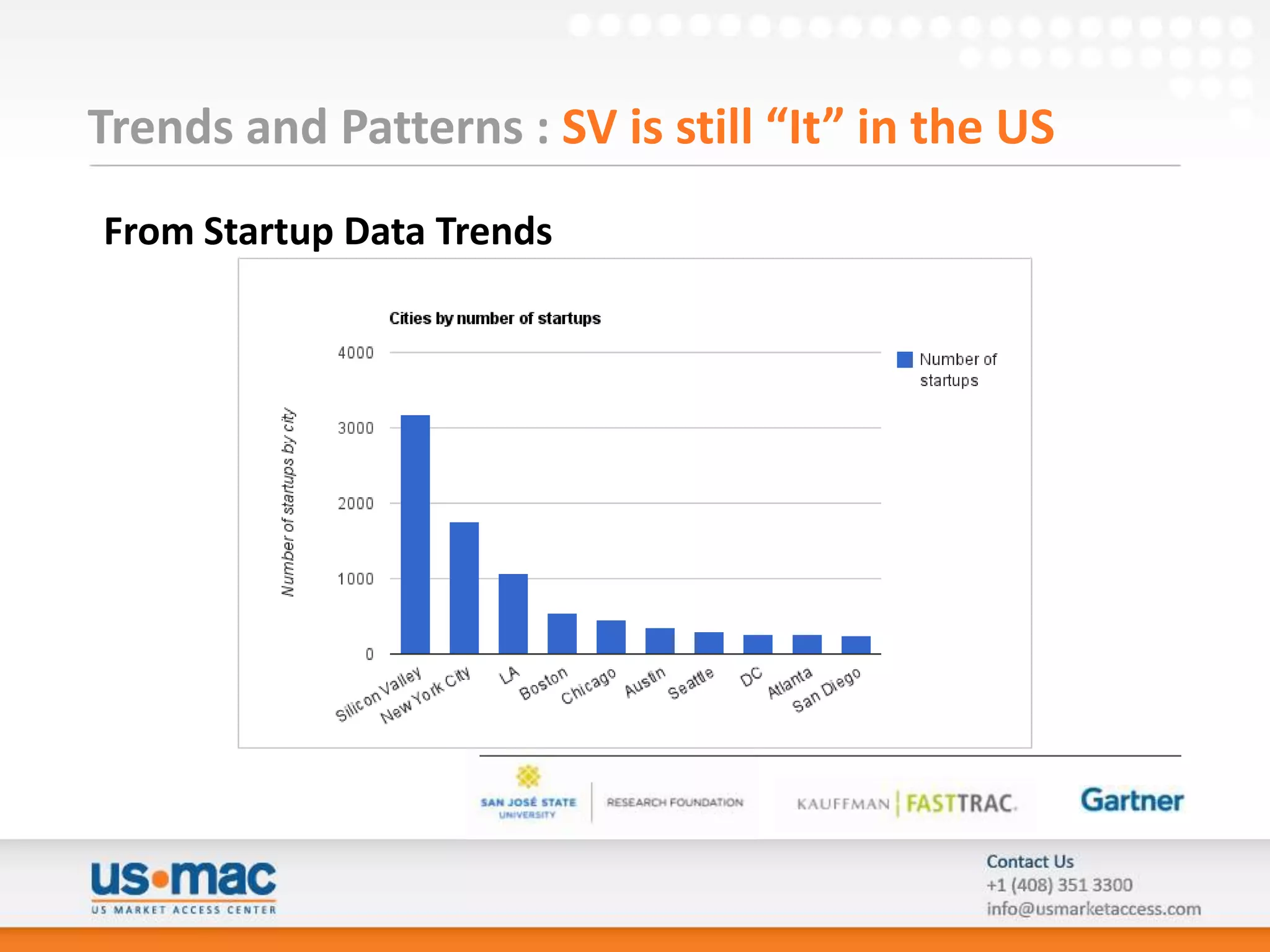

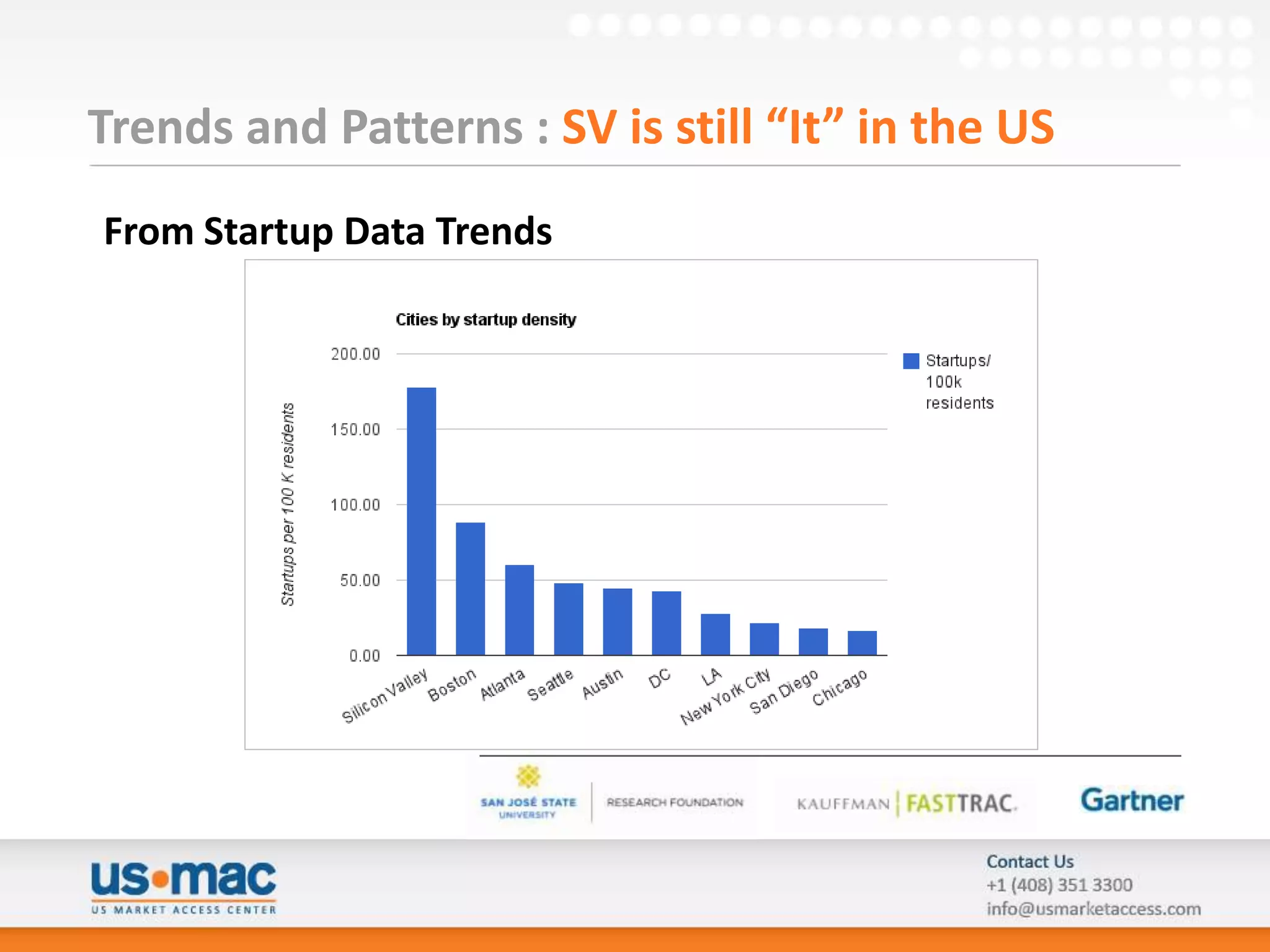

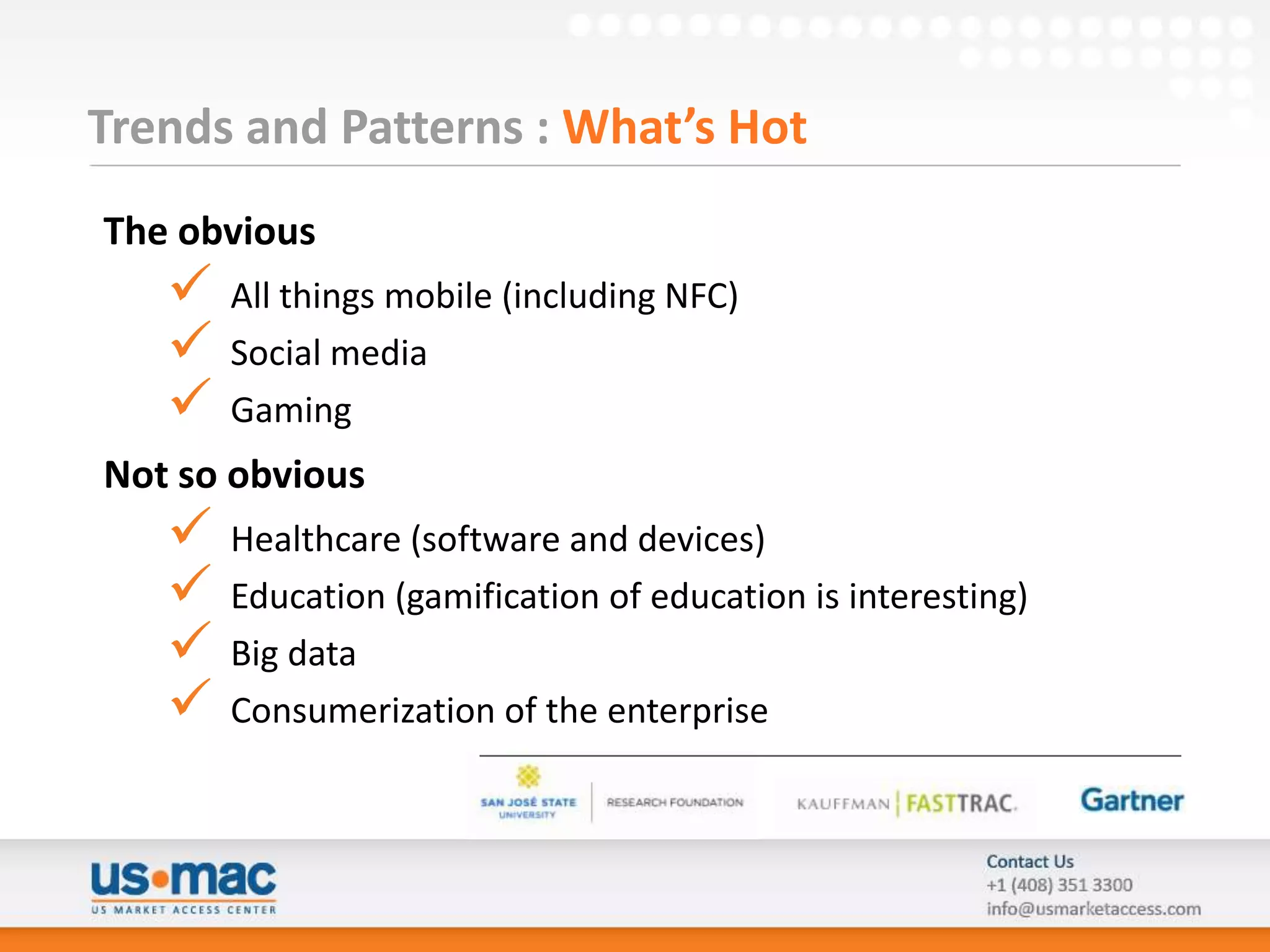

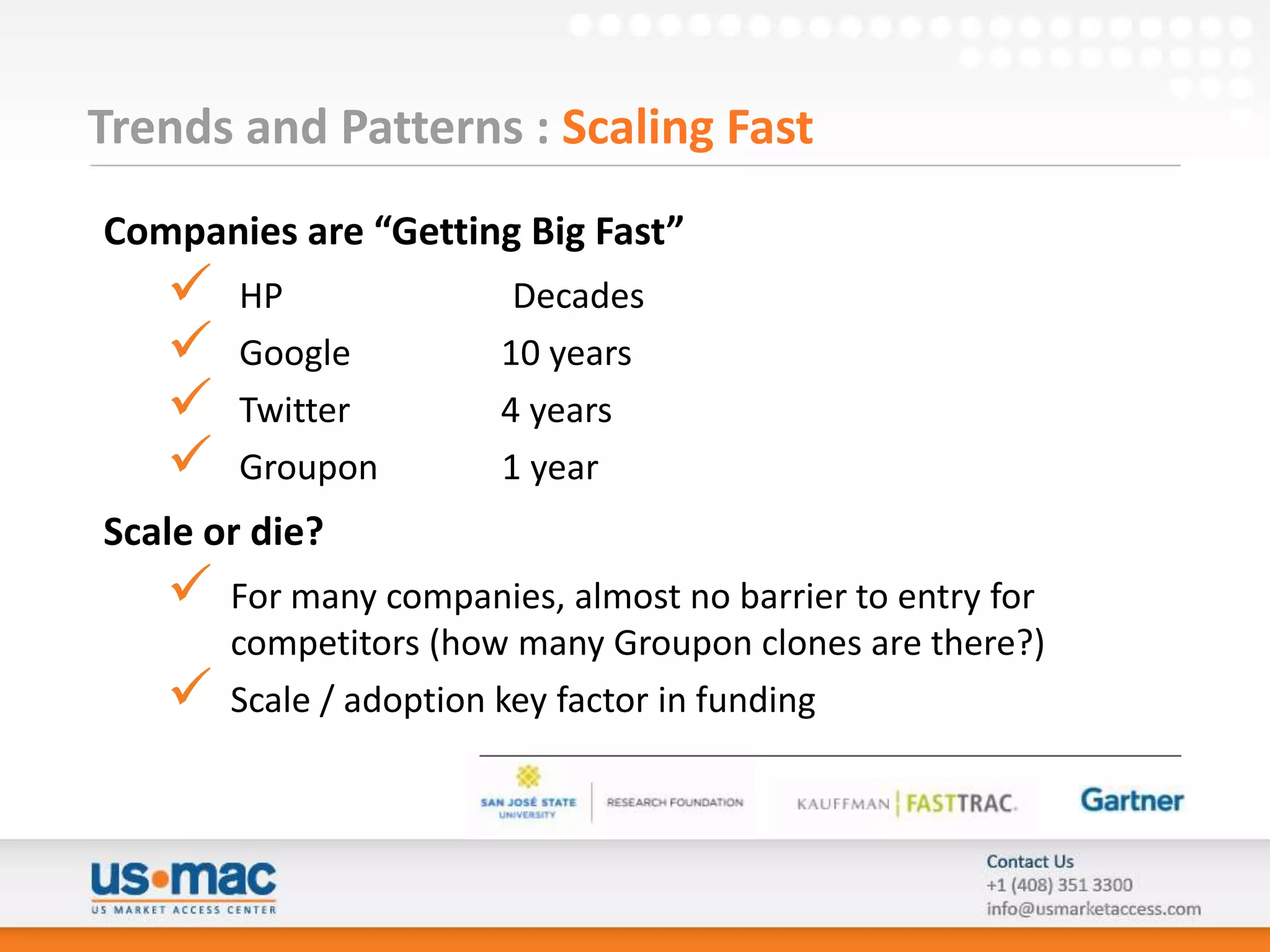

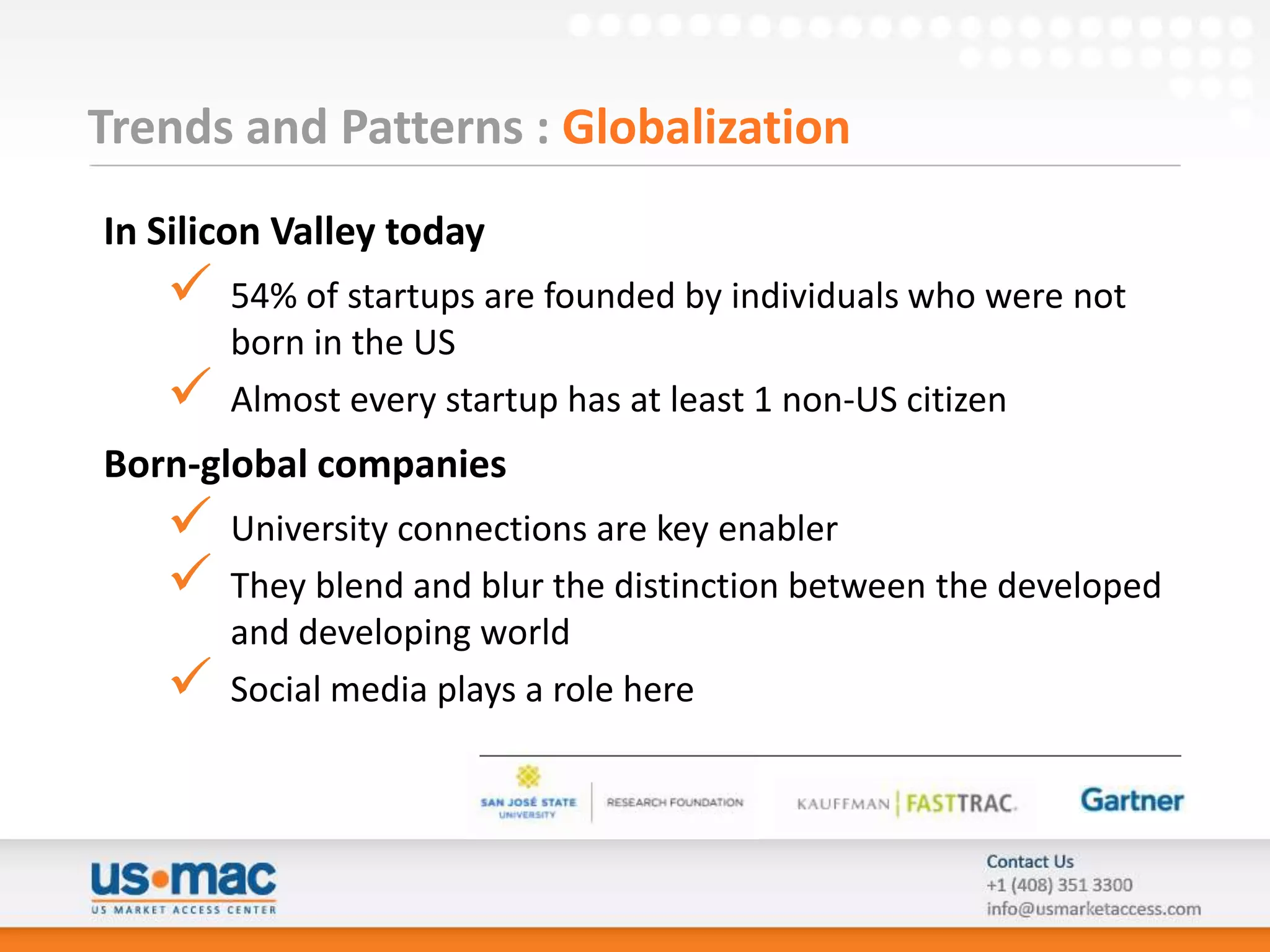

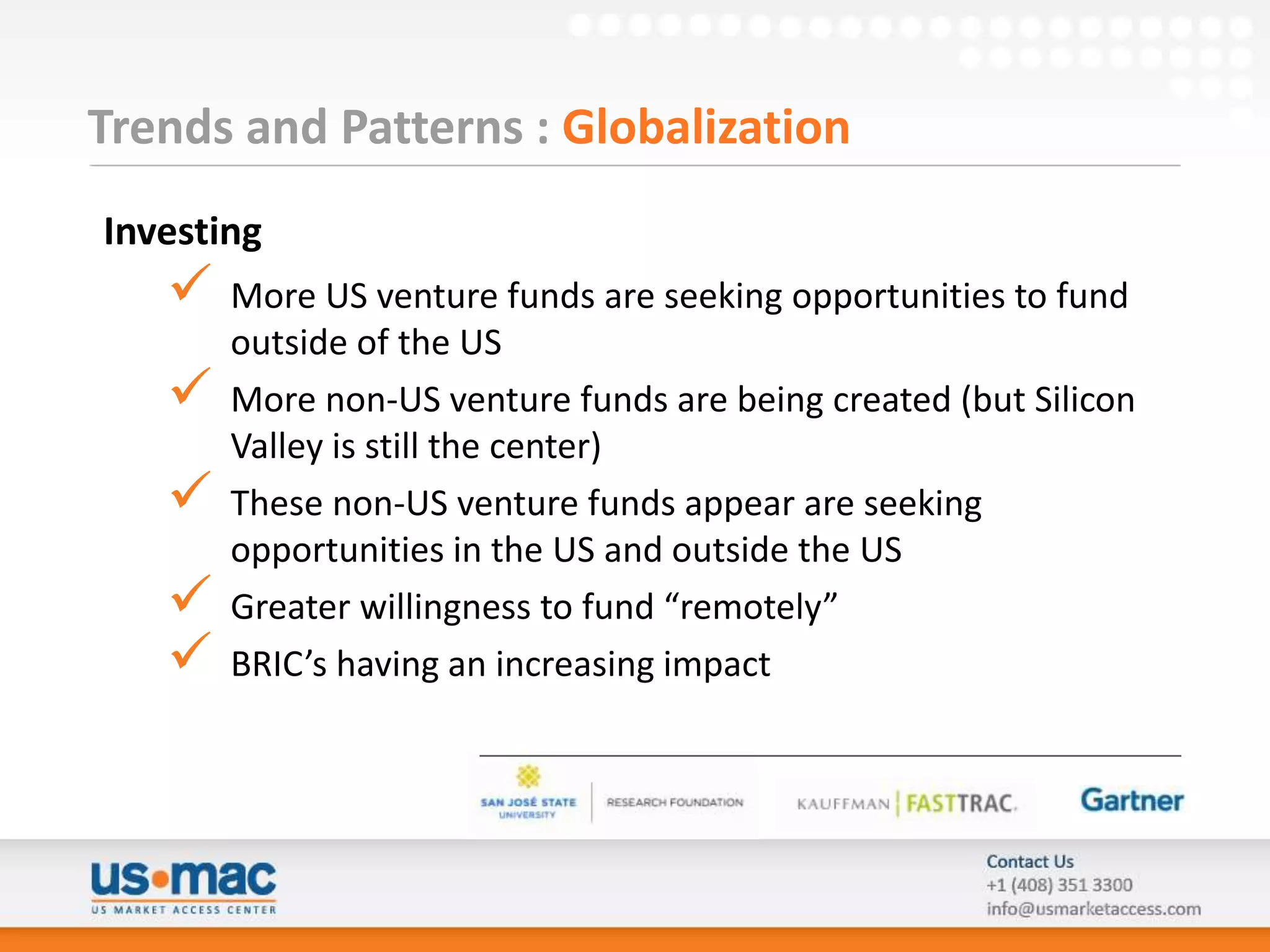

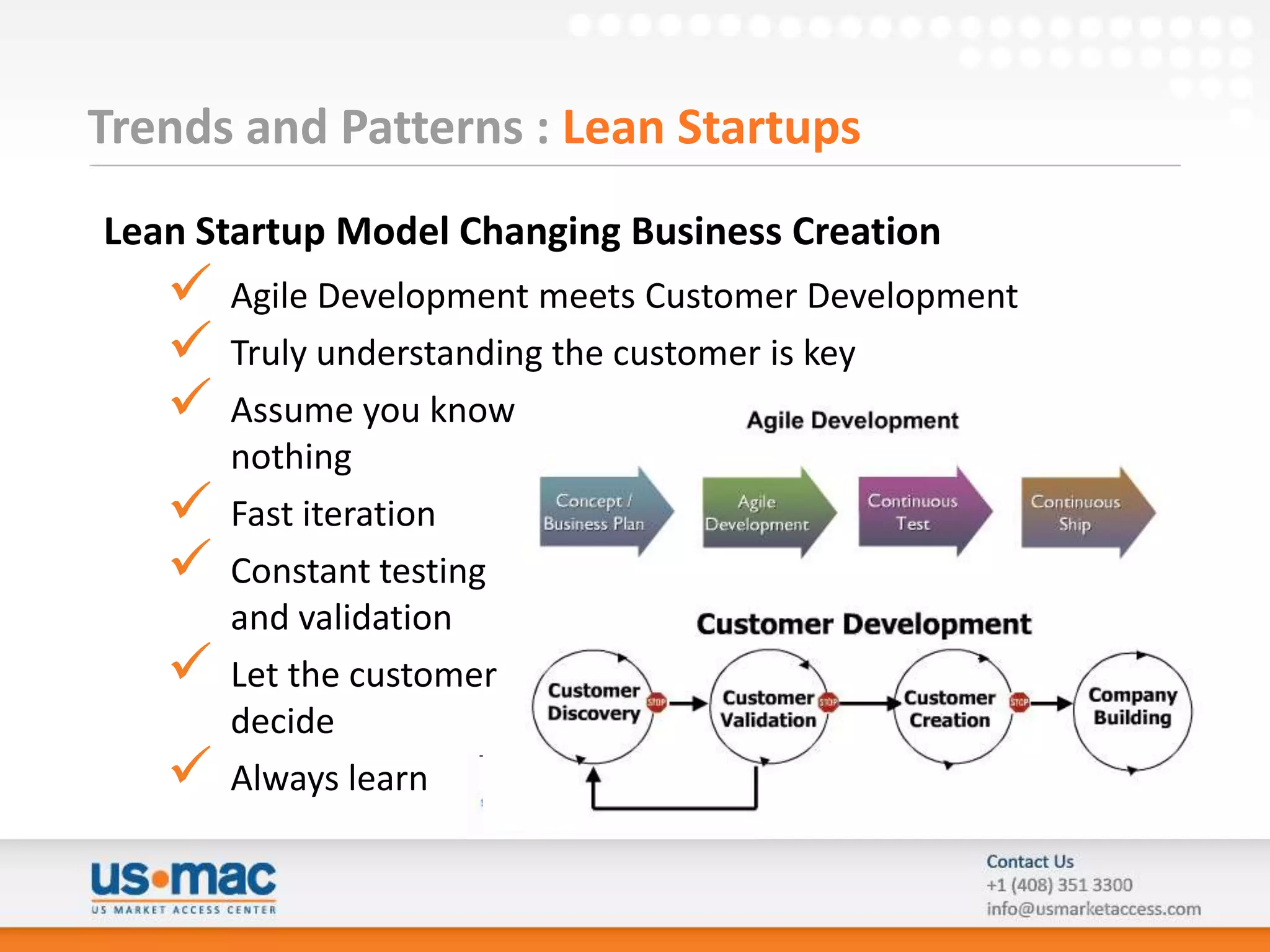

The document provides observations on trends in Silicon Valley from Chris Burry, a consultant with experience founding multiple companies. Some key trends discussed include: - Activity and investment levels rebounding after the dot-com crash - Mobile technologies, social media, healthcare, and big data among the hottest areas - Companies scaling very quickly, within a few years or less, to achieve global impact - Startups founded or led by individuals not born in the US are increasingly common - The Lean Startup methodology is gaining prominence, emphasizing customer validation

![Getting the Work Done [Code for America Summit 2018 Breakout Session]](https://cdn.slidesharecdn.com/ss_thumbnails/cfatalk9-180604135347-thumbnail.jpg?width=640&height=640&fit=bounds)

![INNOVATE YOUR BUSINESS AMIDST THE DIGITAL [R]EVOLUTION](https://cdn.slidesharecdn.com/ss_thumbnails/projectrevolution2-0-120903190533-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)