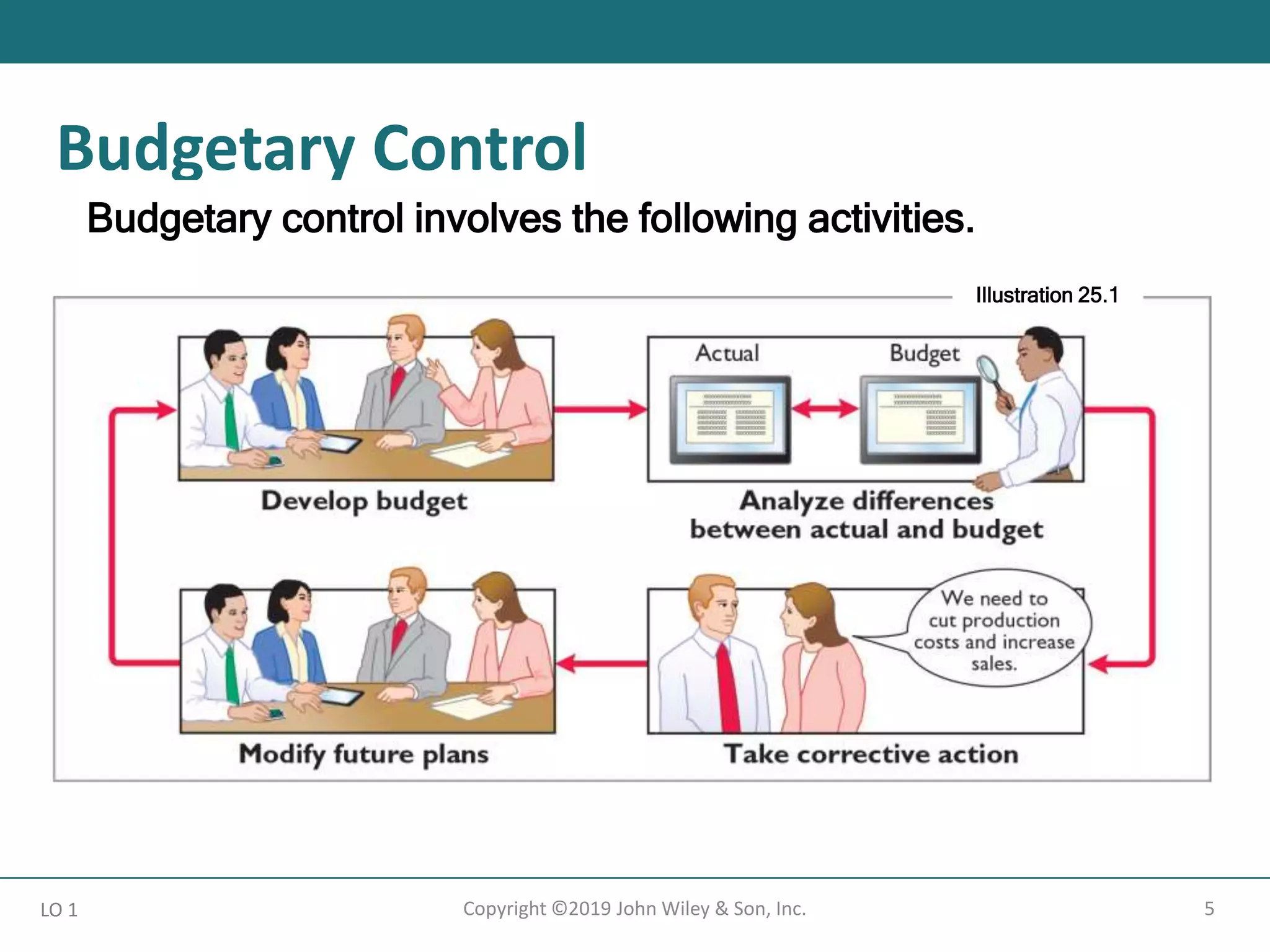

This document discusses budgetary control and responsibility accounting. It begins with an overview of budgetary control and static budget reports. It describes how static budgets compare actual results to planned budgets at a single activity level. The document then covers flexible budget reports, which allow budgets to vary with multiple activity levels. Finally, it discusses responsibility accounting and how costs and revenues can be tracked based on the level of management control. Key terms introduced include static budgets, flexible budgets, controllable vs. non-controllable costs, and responsibility centers.

![62

LO 4

Increasing Controllable Margin

ILLUSTRATION 25.27

Increase ROI by increasing sales or by reducing variable and

controllable fixed costs.

2. Decrease variable and fixed costs 10%.

► Total costs decrease €140,000 [(€1,100,000 + €300,000)

X 10%].

► Controllable margin becomes €740,000.

► New ROI becomes 14.8%.

Copyright ©2019 John Wiley & Son, Inc.](https://image.slidesharecdn.com/chapter24-budgetarycontrolandresponsibilityaccounting-221214165233-5992603e/75/Chapter-24-Budgetary-Control-and-Responsibility-Accounting-pptx-62-2048.jpg)

![Appendix 25A ROI vs. Residual Income

65

Copyright ©2018 John Wiley & Son, Inc.

How Tracker will effect ROI.

LO 5

Without With

Tracker Tracker Tracker

Contribution margin (a) €1,000,000 €260,000 €1,260,000

Average operating assets (b) €5,000,000 €2,000,000 €7,000,000

Return on investment [(a) ÷ (b)] 20% 13% 18%

ILLUSTRATION 25A.2

The problem with ROI analysis is that it ignores minimum rate

of return on a operating assets.

Assuming a minimum rate of return of 10%, it should invest in

Tracker because its ROI of 13% is greater than 10%.](https://image.slidesharecdn.com/chapter24-budgetarycontrolandresponsibilityaccounting-221214165233-5992603e/75/Chapter-24-Budgetary-Control-and-Responsibility-Accounting-pptx-65-2048.jpg)

![66

Copyright ©2018 John Wiley & Son, Inc.

LO 5

Residual

Income

Controllable

Margin

Minimum Rate of Return

x

Average Operating Assets

- =

€260,000 10% x €2,000,000 €60,000

- =

ILLUSTRATION 25A.3

Residual Income Compared to ROI

To evaluate performance using the minimum rate of return,

companies use the residual income approach.

Without With

Tracker Tracker Tracker

Contribution margin (a) €1,000,000 €260,000 €1,260,000

Average operating assets x 10% (b) 500,000 200,000 700,000

Residual income [(a) - (b)] € 500,000 € 60,000 € 560,000

ILLUSTRATION 25A.4

Residual income comparison](https://image.slidesharecdn.com/chapter24-budgetarycontrolandresponsibilityaccounting-221214165233-5992603e/75/Chapter-24-Budgetary-Control-and-Responsibility-Accounting-pptx-66-2048.jpg)

![67

Copyright ©2018 John Wiley & Son, Inc.

LO 5

Residual Income Weakness

To evaluate performance using the minimum rate of return,

companies use the residual income approach.

ILLUSTRATION 25A.5

Tracker SeaDog

Contribution margin (a) €260,000 €460,000

Average operating assets x 10% (b) 200,000 400,000

Residual income [(a) - (b)] € 60,000 € 60,000

If these two investments were evaluated using residual

income, they would be considered equal.

This ignores the fact that SeaDog required twice as many

operating assets to achieve the same level of residual income.](https://image.slidesharecdn.com/chapter24-budgetarycontrolandresponsibilityaccounting-221214165233-5992603e/75/Chapter-24-Budgetary-Control-and-Responsibility-Accounting-pptx-67-2048.jpg)