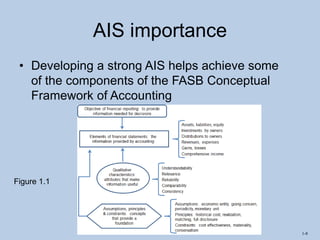

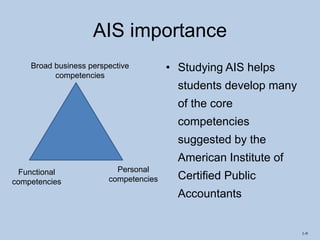

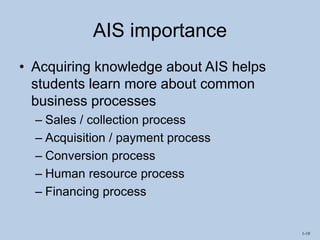

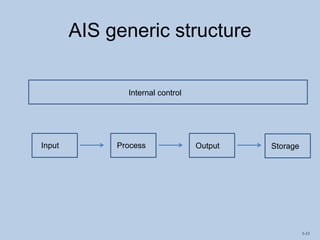

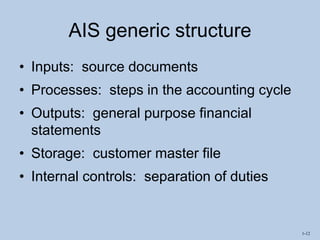

This document discusses accounting information systems (AIS) and their importance. It defines AIS as a set of interrelated activities, documents, and technologies designed to collect, process, and report financial information to internal and external decision makers. The document outlines learning objectives and discusses why studying AIS is important for accountants, such as understanding business processes and developing competencies. It also describes the generic structure of AIS, including inputs, processes, outputs, storage, and internal controls. Finally, the document discusses information literacy and criteria for evaluating information sources.

![How Big Brands are Taking Your Traffic in Alberta [Data Inside].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/howbigbrandsaretakingyourtrafficinalbertadatainside-260123180142-42d276f3-thumbnail.jpg?width=640&height=640&fit=bounds)