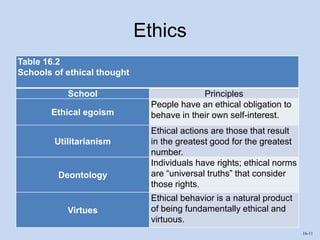

This document discusses professionalism, ethics, and career planning in accounting. It begins by outlining the learning objectives, which are to define professionalism and ethics, discuss models of ethical decision making, and explain how to resolve ethical dilemmas. It then defines professionalism and lists characteristics of professionals, such as specialized knowledge and adherence to codes of ethics. Next, it defines ethics and discusses schools of ethical thought, as well as a model for ethical decision making. Finally, it analyzes several past accounting scandals as cases involving ethics issues.