Download as PDF, PPTX

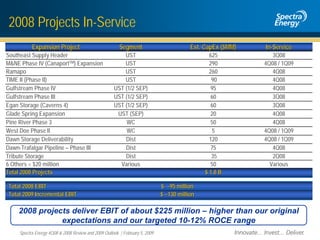

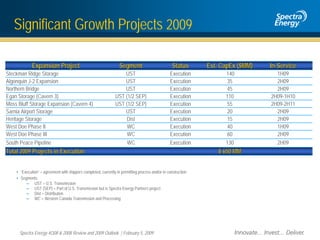

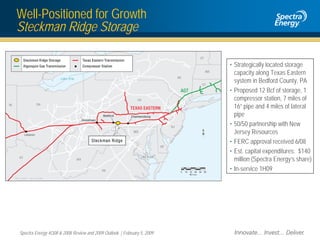

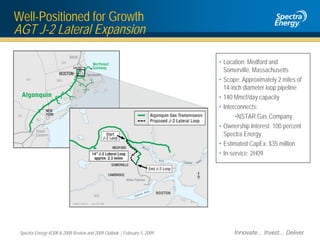

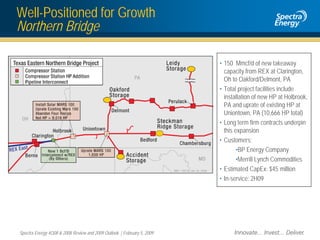

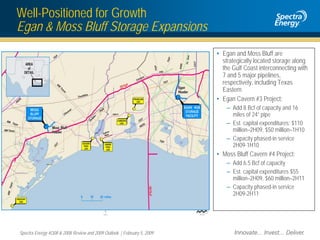

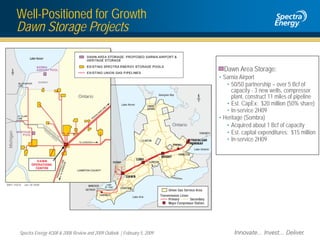

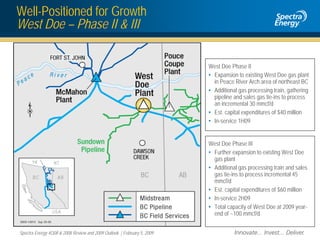

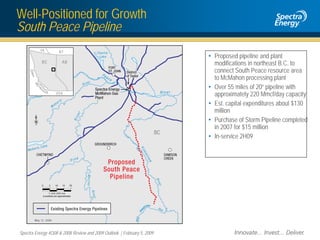

The document outlines Spectra Energy's major pipeline expansion projects for 2008 and 2009. It details 16 projects completed or under construction in 2008 with a total capital expenditure of $1.8 billion, generating estimated EBIT of $95 million in 2008 and $130 million in incremental EBIT in 2009. For 2009, 10 projects are outlined totaling $650 million in capital expenditures. The projects expand natural gas transmission and storage infrastructure across the United States and Canada.