Download as PDF, PPTX

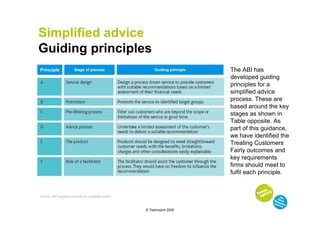

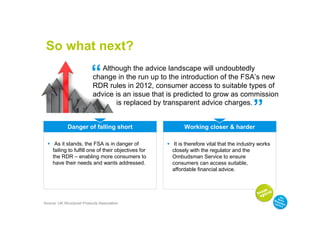

![Simplified advice

Overcoming barriers

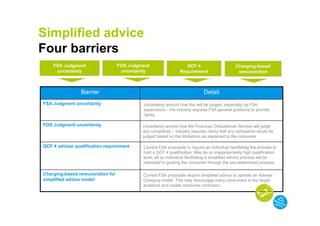

FSA director of conduct policy Sheila Nicoll said that where

simplified advice is delivered via an automated service, QCF level

four may not be required:

When asked whether the FSA accepts that a

Last year, in CP09/18, we suggested that

simplified advice process will deliver good, but not

[QCF level four] standards should apply necessarily the best outcomes, Nicoll said

equally to those giving simplified advice.

The responses to this were divided, and we

can see that there might be an argument in

terms of proportionality. There is also a I have a lot of sympathy with that view, but

question of how the qualification we have to decide what is meant by ’good’

requirements might apply in a simplified – I have no particular objections to that

advice process that is fully automated. statement, however](https://image.slidesharecdn.com/microsoftpowerpoint-simplifiedadvicemay2010-100607113748-phpapp01/85/RDR-Simplified-Advice-May-2010-15-320.jpg)

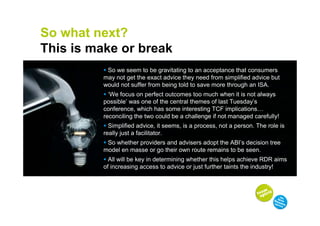

The document discusses the challenges and ongoing developments surrounding simplified financial advice in the UK, highlighting complaints from industry stakeholders about a lack of guidance from the FSA. It outlines the necessity for a streamlined advice process to better serve consumers disillusioned with current advice offerings, particularly given the impending implementation of the RDR rules. Furthermore, it emphasizes the need for collaboration between industry players and regulators to ensure accessibility to suitable financial advice for a broader audience.