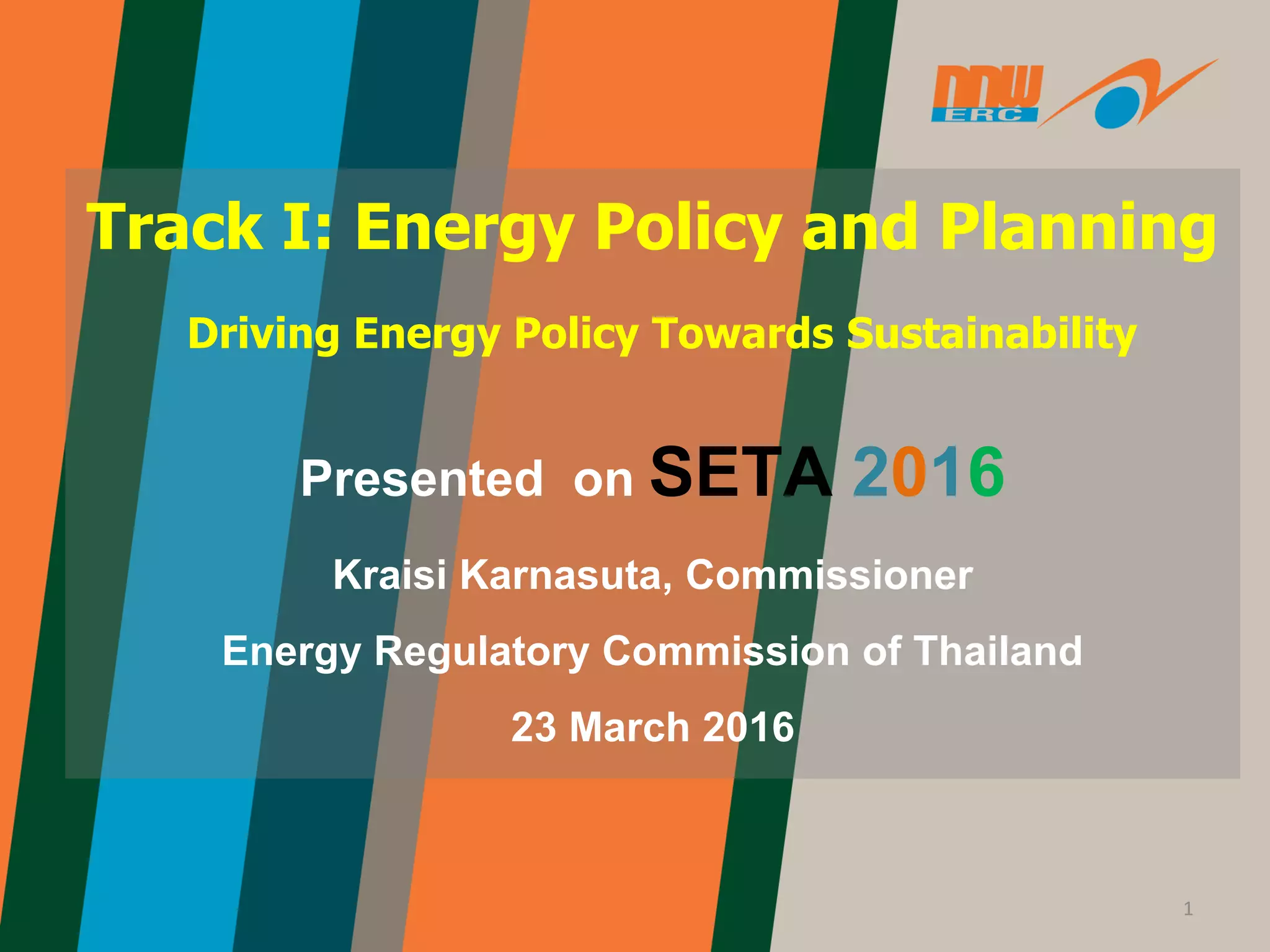

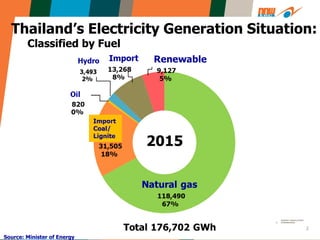

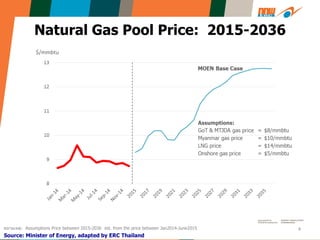

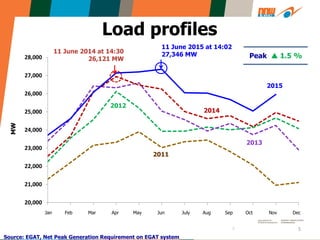

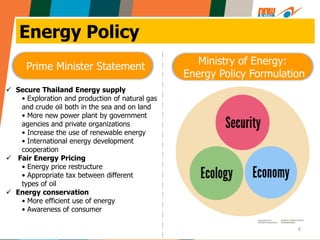

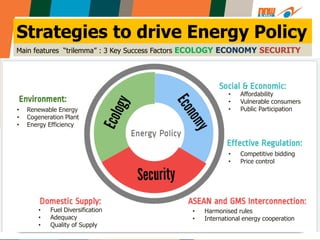

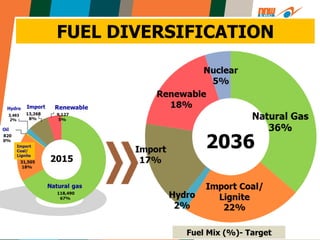

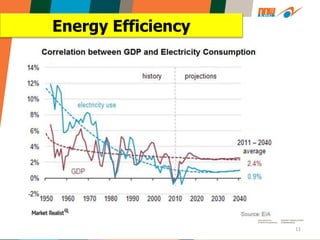

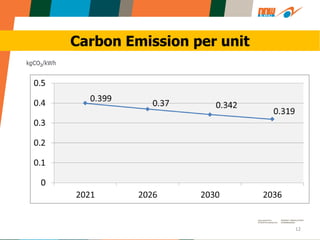

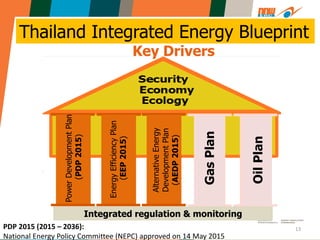

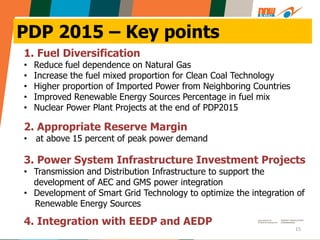

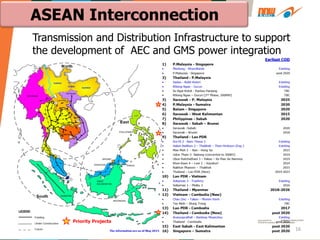

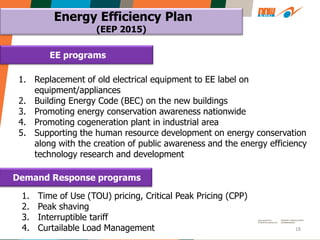

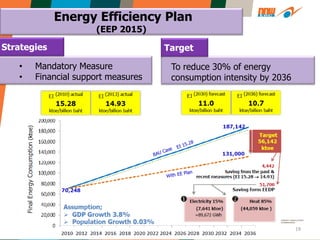

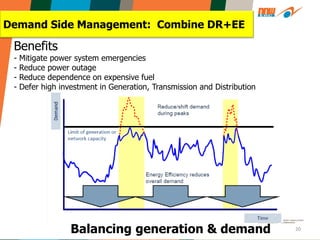

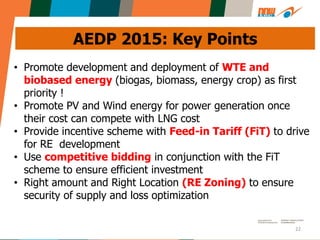

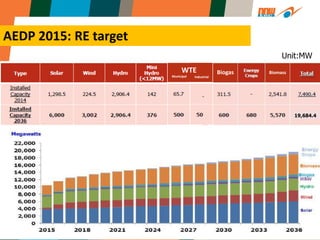

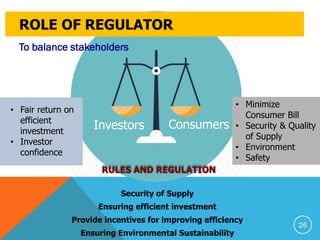

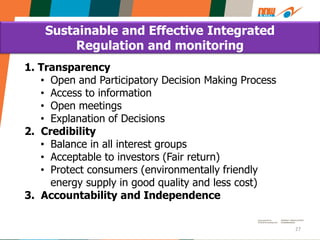

The document discusses Thailand's energy policy and planning aimed at achieving sustainability through a diversified fuel mix, increased renewable energy use, and enhanced energy efficiency from 2015 to 2036. It outlines key strategies to secure energy supply, ensure fair pricing, and promote conservation, emphasizing a 'trilemma' of ecology, economy, and security. The comprehensive energy plans include improvements in power generation infrastructure, demand management, and regulatory frameworks to support energy development and consumer protection.

![[2] Keynote presentation](https://cdn.slidesharecdn.com/ss_thumbnails/2keynotepresentation-151118184147-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Task 1 2] Final energy consumption and reduction scenarios for lao's mecon h...](https://cdn.slidesharecdn.com/ss_thumbnails/task1-2finalenergyconsumptionandreductionscenariosforlaosmeconhouseholdsin2030-151118184259-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Task 6 2] Institutional challenges to implement energy efficiency policy in ...](https://cdn.slidesharecdn.com/ss_thumbnails/task6-2institutionalchallengestoimplementenergyefficiencypolicyinlaopdr-151118190854-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Task 6 1] Institutional conditions for encouragement of energy efficiency in...](https://cdn.slidesharecdn.com/ss_thumbnails/task6-1institutionalconditionsforencouragementofenergyefficiencyingms-151118190737-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)