Download as PDF, PPTX

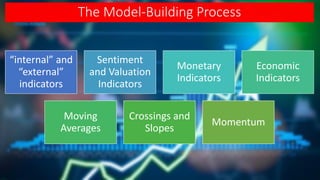

The document discusses the model-building process for a market-timing model. It describes including various types of indicators such as internal/price-based, external/macroeconomic, sentiment, valuation, monetary, and momentum. These indicators are tested individually and combined to form a composite reading. The composite reading can then be used to guide asset allocation decisions in a disciplined and objective manner. The goal is to create a stable, predictable model that avoids emotional decisions and captures risk and reward signals.