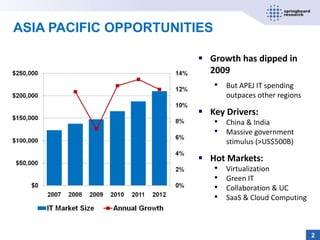

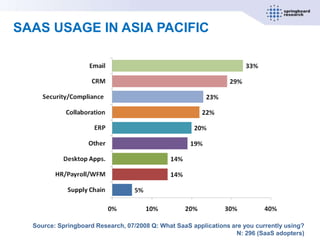

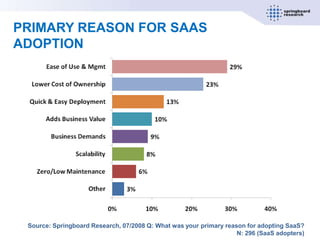

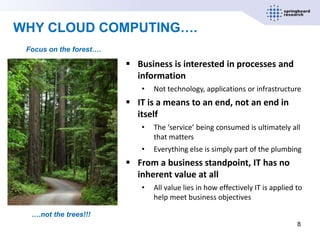

The document discusses the evolution and implications of SaaS and cloud computing in the Asia-Pacific region, highlighting growth trends and market drivers, particularly in 2009. Key challenges for CIOs include cost-saving measures, short-term ROI, and the need for process improvements. It emphasizes the need for businesses to focus on effective use of technology to meet objectives, while also acknowledging challenges such as data governance and integration management.

![5G Explained! A High Level Overview [Introduction]](https://cdn.slidesharecdn.com/ss_thumbnails/5gexplainedahighleveloverview-260119165306-cc137a3e-thumbnail.jpg?width=640&height=640&fit=bounds)