4

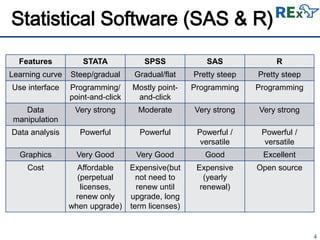

Statistical Software (SAS& R)

Features STATA SPSS SAS R

Learning curve Steep/gradual Gradual/flat Pretty steep Pretty steep

Use interface Programming/

point-and-click

Mostly point-

and-click

Programming Programming

Data

manipulation

Very strong Moderate Very strong Very strong

Data analysis Powerful Powerful Powerful /

versatile

Powerful /

versatile

Graphics Very Good Very Good Good Excellent

Cost Affordable

(perpetual

licenses,

renew only

when upgrade)

Expensive(but

not need to

renew until

upgrade, long

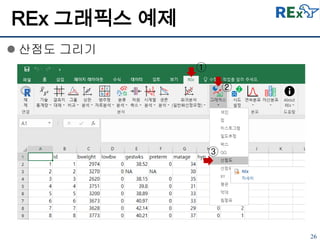

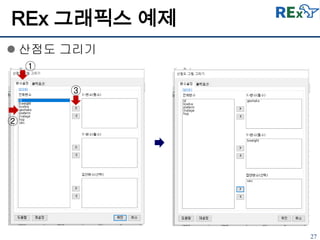

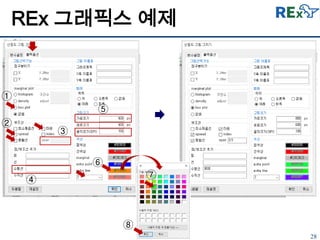

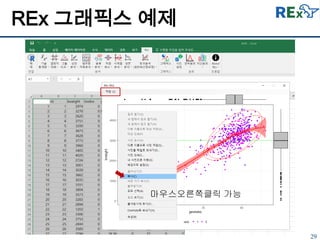

term licenses)

Expensive

(yearly

renewal)

Open source

5.

5

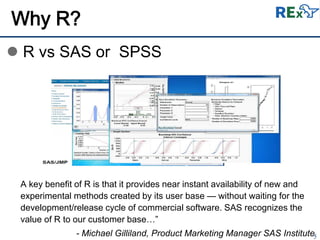

Why R?

Rvs SAS or SPSS

A key benefit of R is that it provides near instant availability of new and

experimental methods created by its user base — without waiting for the

development/release cycle of commercial software. SAS recognizes the

value of R to our customer base…”

- Michael Gilliland, Product Marketing Manager SAS Institute

31

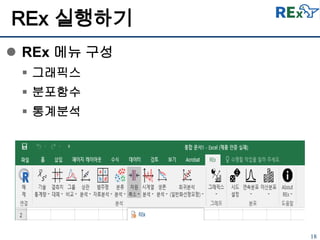

REx 통계 분석메뉴

기술

통계

그룹 비교 회귀분석 상관분석

범주형

자료 분석

분류 분석

차원

축소

시계열

분석

생존분석

데이터

요약

평균

비교

일표본 T 검정

선형회귀

분석

이변량

상관

분할표

분석

비지도

학습

K-평균

군집

요인분석

시계열

자료 탐색

생명표

독립표본 T

검정

가중선형

회귀분석

편상관

로그선형

분석

계층적 군집

대응일치

분석

지수평활법 Kaplan-Meier

대응표본 T

검정

편최소제곱 거리측도 DBSCAN

주성분

분석

ARIMA모형

Cox

비례위험모형

일원배치

분산분석

이분형

로지스틱

PAM 군집

GARCH

모형

다변량

분산분석

다항

로지스틱

지도

학습

의사결정

나무

비율

비교

일표본

비율검정

포아송

회귀분석

판별분석

이표본

비율검정

2-단계

최소제곱

K최근접

이웃기법

분산

비교

등분산검정

반복측정

회귀분석

SVM

다변량

회귀분석

분석메뉴

36

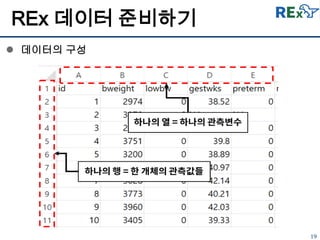

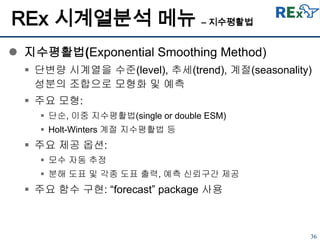

REx 시계열분석 메뉴– 지수평활법

지수평활법(Exponential Smoothing Method)

단변량 시계열을 수준(level), 추세(trend), 계절(seasonality)

성분의 조합으로 모형화 및 예측

주요 모형:

단순, 이중 지수평활법(single or double ESM)

Holt-Winters 계절 지수평활법 등

주요 제공 옵션:

모수 자동 추정

분해 도표 및 각종 도표 출력, 예측 신뢰구간 제공

주요 함수 구현: “forecast” package 사용

39

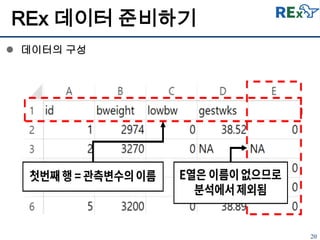

REx 시계열분석 메뉴– ARIMA 모형

ARIMA 모형

자기회귀 누적 이동평균(autoregressive integrated moving-

average) 모형

단변량 시계열을 ARIMA(p,d,q)(P,D,Q)s로 모형화 및 예측

주요 제공 옵션:

독립변수(외생변수) 도입 가능

ARIMA 차수 자동 선택

잔차진단 도표 제공

주요 함수 구현: “forecast” package 사용

42

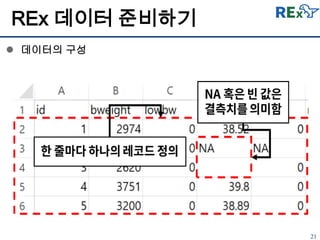

REx 시계열분석 메뉴– GARCH 모형

GARCH 모형

일반화 자기회귀 조건부 이분산 모형(generalized

autoregressive conditional heteroscedastic model)

단변량 시계열의 조건부 이분산을 모형화 및 예측

주요 모형:

standard GARCH, integrated GARCH,

exponential GARCH, GJR GARCH, Threshold GARCH 등

주요 제공 옵션:

다양한 오차 분포 결합 가능: normal, t, GED 등

조건부 평균을 위한 ARMA 모형 및 분수 차분 도입 가능

독립변수(외생변수) 도입 가능

조건부 이분산의 예측도표 제공

주요 함수 구현: “rugarch” package 사용

![34

[시계열자료 탐색] 대화상자 구성

REx 시계열분석 메뉴 – 시계열자료 탐색](https://image.slidesharecdn.com/ruck2017-rexr-171106135228/85/RUCK-2017-REx-R-33-320.jpg)

![35

[시계열자료 탐색] 실행 결과 예

REx 시계열분석 메뉴 – 시계열자료 탐색](https://image.slidesharecdn.com/ruck2017-rexr-171106135228/85/RUCK-2017-REx-R-34-320.jpg)

![37

[지수평활법] 대화상자 구성

REx 시계열분석 메뉴 – 지수평활법](https://image.slidesharecdn.com/ruck2017-rexr-171106135228/85/RUCK-2017-REx-R-36-320.jpg)

![38

[지수평활법] 실행 결과 예

REx 시계열분석 메뉴 – 지수평활법](https://image.slidesharecdn.com/ruck2017-rexr-171106135228/85/RUCK-2017-REx-R-37-320.jpg)

![40

[ARIMA 모형] 대화상자 구성

REx 시계열분석 메뉴 – ARIMA 모형](https://image.slidesharecdn.com/ruck2017-rexr-171106135228/85/RUCK-2017-REx-R-39-320.jpg)

![41

[ARIMA 모형] 실행 결과 예

REx 시계열분석 메뉴 – ARIMA 모형](https://image.slidesharecdn.com/ruck2017-rexr-171106135228/85/RUCK-2017-REx-R-40-320.jpg)

![43

[GARCH 모형] 대화상자 구성

REx 시계열분석 메뉴 – GARCH 모형](https://image.slidesharecdn.com/ruck2017-rexr-171106135228/85/RUCK-2017-REx-R-42-320.jpg)

![44

[GARCH 모형] 실행 결과 예

REx 시계열분석 메뉴 – GARCH 모형](https://image.slidesharecdn.com/ruck2017-rexr-171106135228/85/RUCK-2017-REx-R-43-320.jpg)

![[224] 번역 모델 기반_질의_교정_시스템](https://cdn.slidesharecdn.com/ss_thumbnails/242-150915010843-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![[빅데이터 컨퍼런스 전희원]](https://cdn.slidesharecdn.com/ss_thumbnails/random-120412212952-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[213] 의료 ai를 위해 세상에 없는 양질의 data 만드는 도구 제작하기](https://cdn.slidesharecdn.com/ss_thumbnails/213aidata-171016104902-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Open Technet Summit 2014] 쓰기 쉬운 Hadoop 기반 빅데이터 플랫폼 아키텍처 및 활용 방안](https://cdn.slidesharecdn.com/ss_thumbnails/open-technet-summit-2014-140313001107-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[파인트리오픈클래스] 엑셀을 활용한 데이터 분석과 이해](https://cdn.slidesharecdn.com/ss_thumbnails/selection1-170223035345-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Week5] Getting started with R](https://cdn.slidesharecdn.com/ss_thumbnails/week5rprogrammingpdf-150130233806-conversion-gate02-thumbnail.jpg?width=640&height=640&fit=bounds)