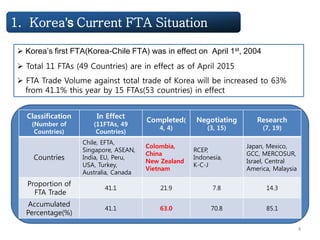

![Iceland, Norway, Switzerland,

Liechtenstein

Chile

Singapore

EFTA

ASEAN

KOREA

Indonesia, Laos,

Vietnam, Philippines,

Thailand, Cambodia,

Malaysia, Brunei,

Singapore, Myanmar

India

Peru

EU

K-Chile FTA

(Apr.2004)

K-Singapore]

(March 2006)

K-EFTA FTA

(Sept. 2006

K-ASEAN FTA

(June 2007)

K-India CEPA

(Jan. 2010)

K-EU FTA

(July 2011)

K-PERU FTA

(Aug. 2011)

K-USA FTA

(Mar. 2012)

USA

Turkey

2. Korea’s Current FTA Map

Australia

Canada

K-Turkey FTA

(May 2013)

K-Australia FTA

(Dec. 2014)

K-Canada FTA

(Jan. 2015)

China

Vietnam

Columbia

New Zealand](https://image.slidesharecdn.com/rooinftasystems-150611080534-lva1-app6891/85/Policy-of-Free-Trade-Agreement-in-Korea-5-320.jpg)

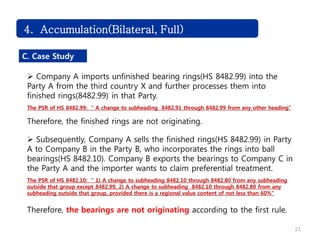

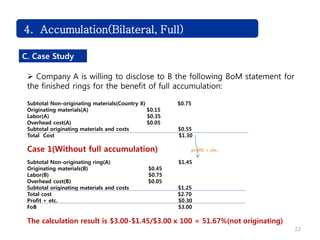

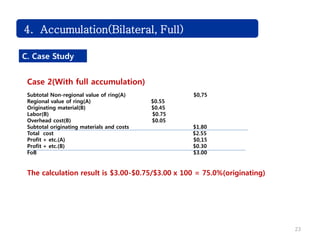

This document discusses rules of origin under free trade agreements (FTAs) in Korea. It begins with an overview of Korea's FTAs, noting it currently has 11 FTAs in effect covering 49 countries, accounting for 41.1% of its total trade. The rest of the document covers key rules of origin concepts under Korean FTAs, including wholly obtained rules, change of tariff classification rules, regional value content rules, and accumulation. Case studies are provided to illustrate how each rule would apply to sample product scenarios.