Downloaded 43 times

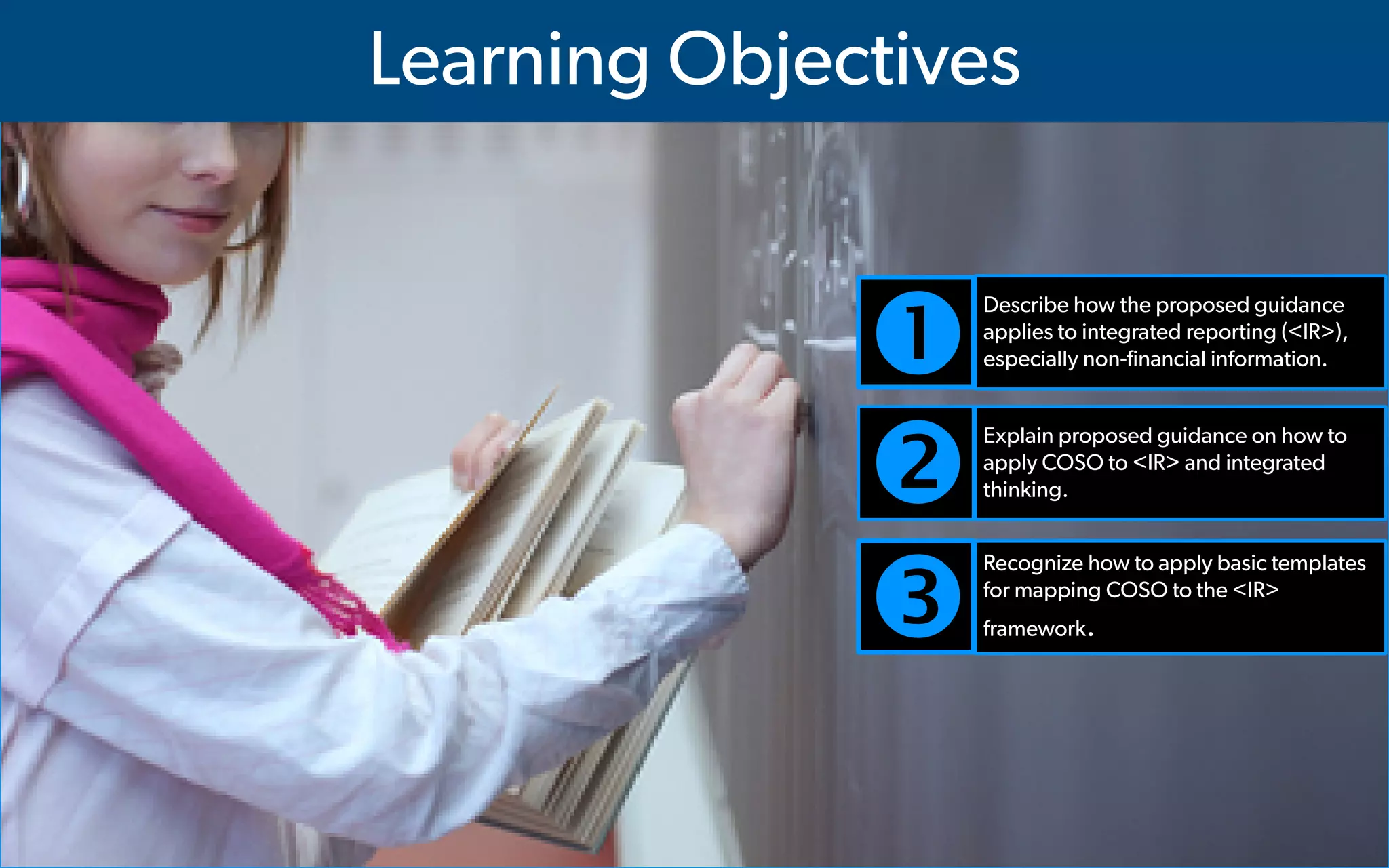

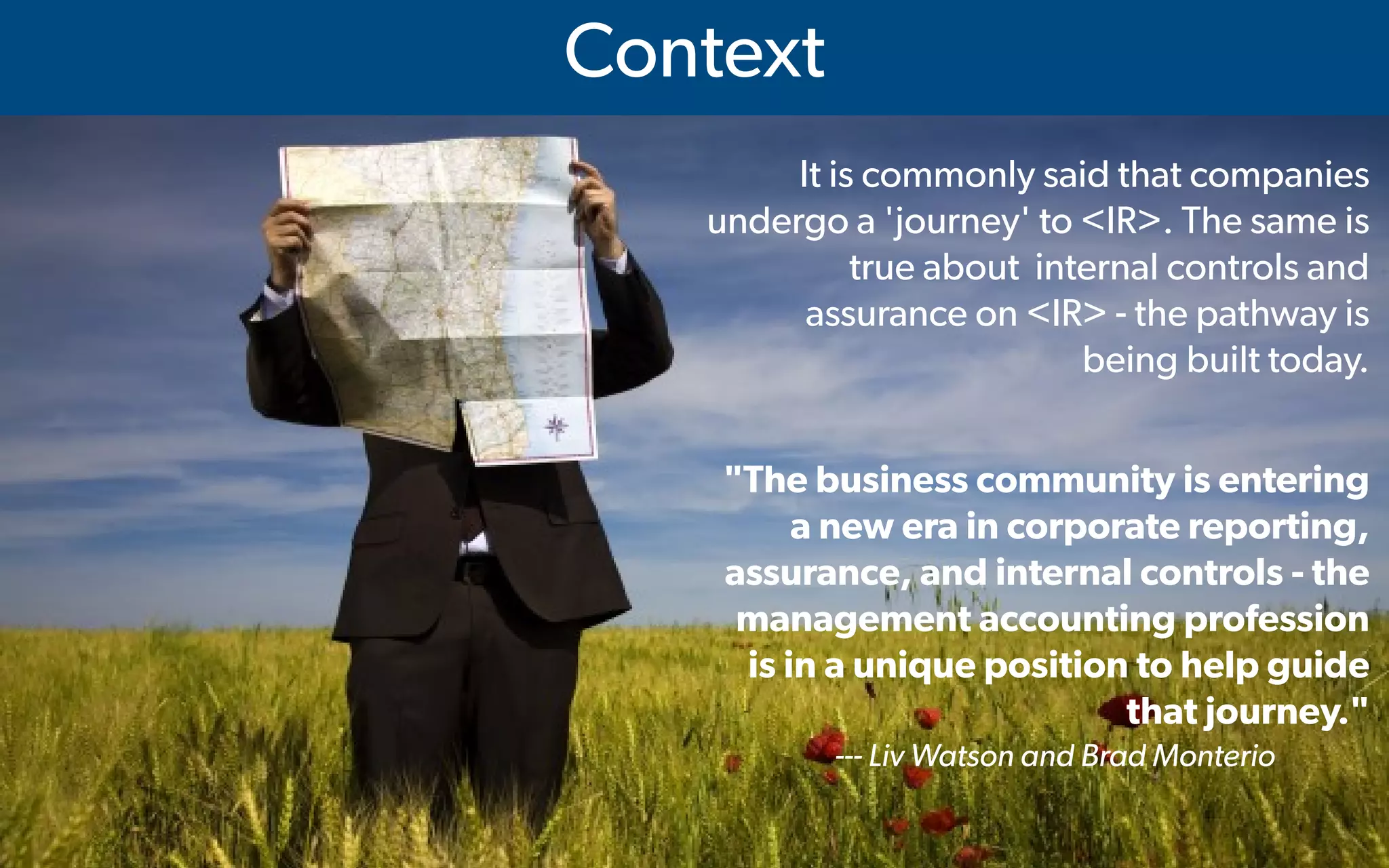

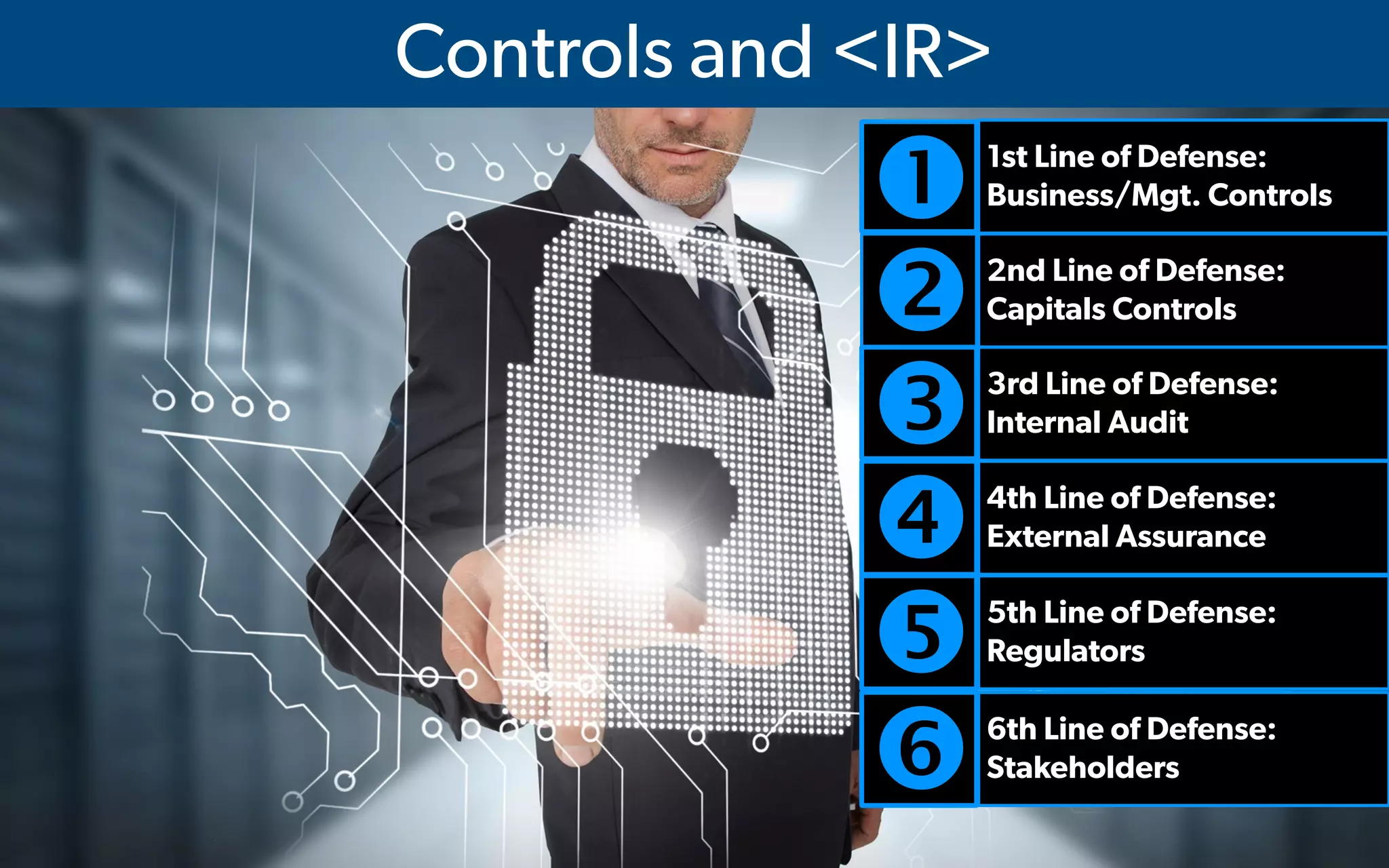

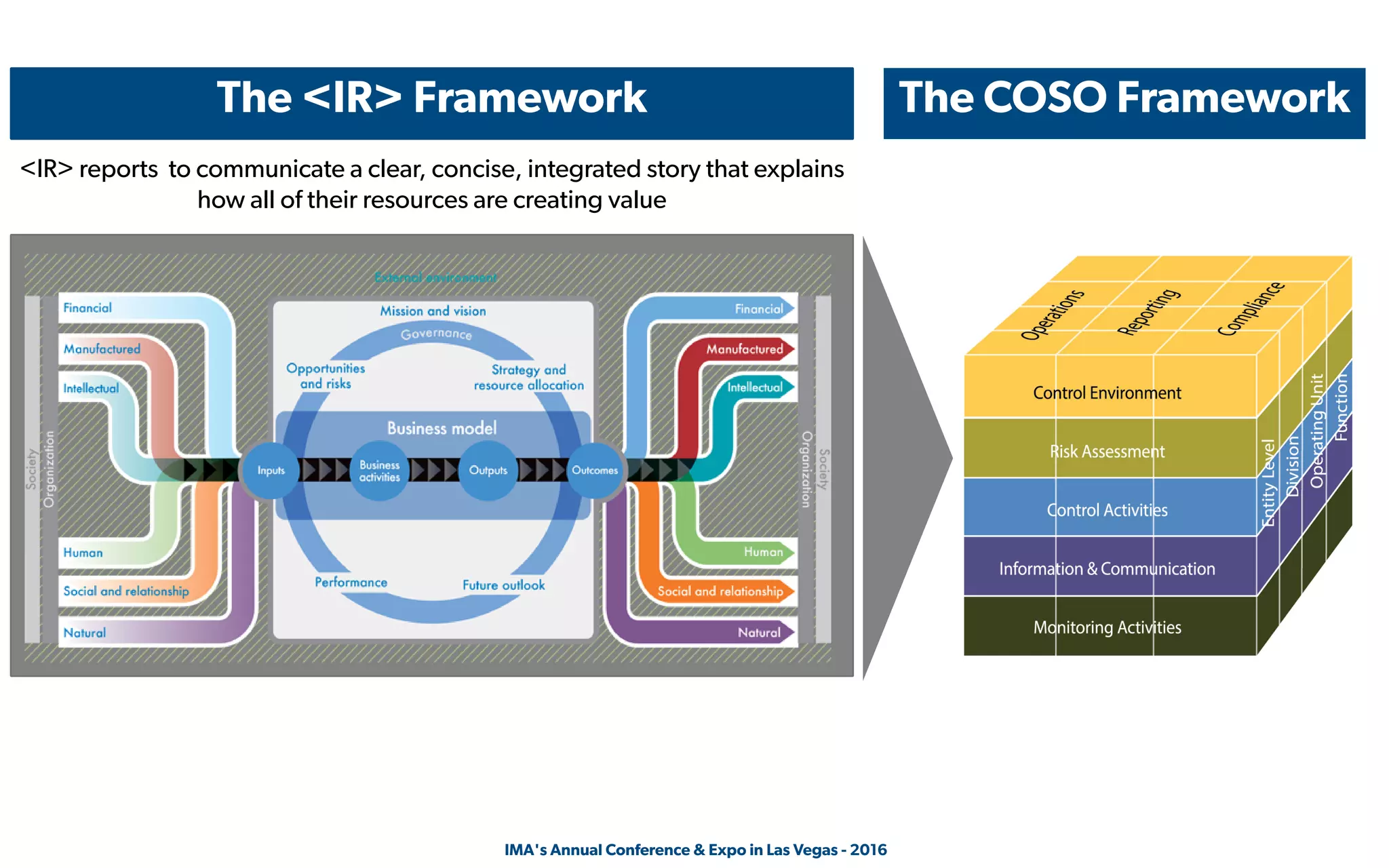

This document summarizes a presentation given at IMA's Annual Conference & Expo in Las Vegas in 2016. The presentation discussed proposed guidance on applying the COSO framework to integrated reporting and integrated thinking. It covered how COSO applies to non-financial information in integrated reports, how to map COSO controls to the integrated reporting framework, and challenges of assurance for integrated reports. The presentation aimed to help participants understand and apply the proposed guidance on internal controls for integrated reporting.