Materiality In Financial Reporting Bellandi Francesco

Materiality In Financial Reporting Bellandi Francesco

Materiality In Financial Reporting Bellandi Francesco

Materiality In Financial Reporting Bellandi Francesco

Materiality In Financial Reporting Bellandi Francesco

1.

Materiality In FinancialReporting Bellandi

Francesco download

https://ebookbell.com/product/materiality-in-financial-reporting-

bellandi-francesco-7438088

Explore and download more ebooks at ebookbell.com

2.

Here are somerecommended products that we believe you will be

interested in. You can click the link to download.

Materiality In Roman Art And Architecture Aesthetics Semantics And

Function Annette Haug Editor Adrian Hielscher Editor M Taylor

Lauritsen Editor

https://ebookbell.com/product/materiality-in-roman-art-and-

architecture-aesthetics-semantics-and-function-annette-haug-editor-

adrian-hielscher-editor-m-taylor-lauritsen-editor-50378400

Materiality In Institutions Spaces Embodiment And Technology In

Management And Organization 1st Ed Franoisxavier De Vaujany

https://ebookbell.com/product/materiality-in-institutions-spaces-

embodiment-and-technology-in-management-and-organization-1st-ed-

franoisxavier-de-vaujany-9960528

Materiality In Roman Art And Architecture Aesthetics Semantics And

Function Annette Haug

https://ebookbell.com/product/materiality-in-roman-art-and-

architecture-aesthetics-semantics-and-function-annette-haug-49443606

Materiality In Roman Art And Architecture Annette Haug Adrian

Hielscher

https://ebookbell.com/product/materiality-in-roman-art-and-

architecture-annette-haug-adrian-hielscher-232649434

3.

Religious Materiality InThe Early Modern World Suzanna Ivanic Editor

Mary Laven Editor Andrew Morrall Editor

https://ebookbell.com/product/religious-materiality-in-the-early-

modern-world-suzanna-ivanic-editor-mary-laven-editor-andrew-morrall-

editor-51756430

Ma Materiality In Teaching And Learning New Boyd White Pauline

Sameshima

https://ebookbell.com/product/ma-materiality-in-teaching-and-learning-

new-boyd-white-pauline-sameshima-58166966

Inhuman Materiality In Gothic Media Aspasia Stephanou

https://ebookbell.com/product/inhuman-materiality-in-gothic-media-

aspasia-stephanou-23823624

Religious Materiality In The Early Modern World Visual And Material

Culture 13001700 Mary Laven

https://ebookbell.com/product/religious-materiality-in-the-early-

modern-world-visual-and-material-culture-13001700-mary-laven-43220156

Crafting In The World Materiality In The Making 1st Ed Clare Burke

https://ebookbell.com/product/crafting-in-the-world-materiality-in-

the-making-1st-ed-clare-burke-7321884

Emerald Publishing Limited

HowardHouse, Wagon Lane, Bingley BD16 1WA, UK

First edition 2018

Copyright r 2018 Emerald Publishing Limited

Reprints and permissions service

Contact: permissions@emeraldinsight.com

No part of this book may be reproduced, stored in a retrieval system, transmitted

in any form or by any means electronic, mechanical, photocopying, recording or

otherwise without either the prior written permission of the publisher or a licence

permitting restricted copying issued in the UK by The Copyright Licensing Agency

and in the USA by The Copyright Clearance Center. Any opinions expressed in the

chapters are those of the authors. Whilst Emerald makes every effort to ensure the

quality and accuracy of its content, Emerald makes no representation implied or

otherwise, as to the chapters’ suitability and application and disclaims any

warranties, express or implied, to their use.

British Library Cataloguing in Publication Data

A catalogue record for this book is available from the British Library

ISBN: 978 1 78743 737 1 (Print)

ISBN: 978 1 78743 736 4 (Online)

ISBN: 978 1 78743 843 9 (Epub)

Certificate Number 1985

ISO 14001

ISOQAR certified

Management System,

awarded to Emerald

for adherence to

Environmental

standard

ISO 14001:2004.

Contents

List of Figuresxix

About the Author xxv

Preface xxvii

Part I. Introduction and Background 1

Main Focus of Part I 2

1. Why Does Materiality Matter in Financial Statements? 2

2. Powerful and Dangerous 3

3. The Disclosure Framework 4

4. The Disclosure Initiative 5

5. The Disclosure Effectiveness Initiative 6

6. Objectives of the Book 7

Part II. Conceptual Bases of Materiality 9

Main Focus of Part II 10

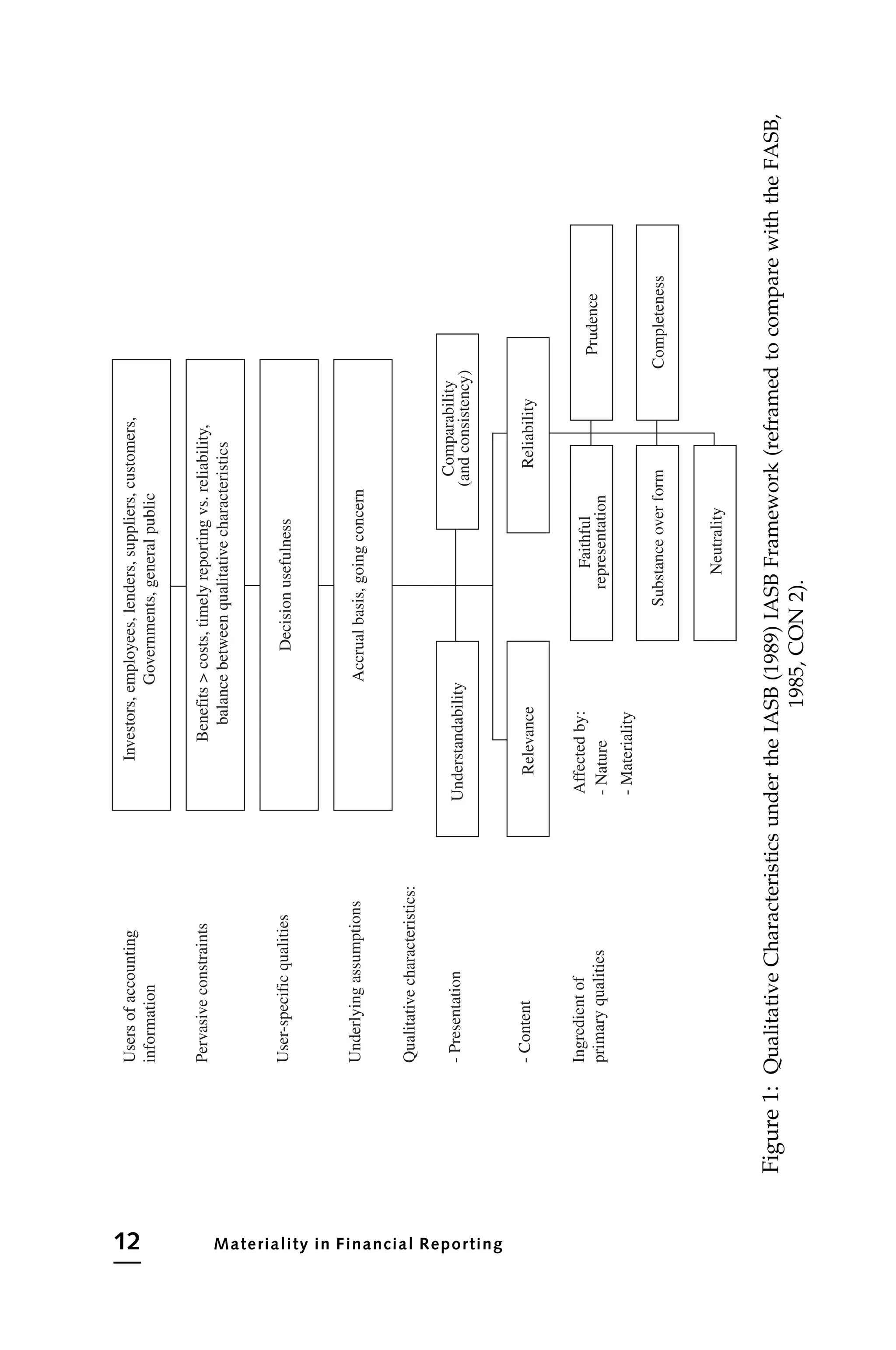

1. Materiality in the Conceptual Frameworks 10

1.a. The Objective of Materiality 10

1.b. Level of Interaction in the Conceptual Frameworks 10

1.c. A Pervasive Concept or a Qualitative Characteristic? 11

1.d. Is Materiality a Constraint? 15

1.e. Interaction with Qualitative Characteristics of

Accounting Information 16

1.f. Materiality versus Relevance 16

1.g. Entity Specificity 20

1.h. Materiality versus Reliability and Faithful

Representation 22

1.i. Completing the Picture: Materiality versus

Completeness 24

1.j. Materiality versus Understandability 25

vii

10.

1.k. Does Prudenceor Neutrality Affect Materiality? 27

1.l. The Link to Recognition in the Conceptual

Frameworks 28

1.m. Cost/Benefit Constraint versus Materiality 30

1.n. Impracticability versus Materiality 30

1.o. Significance 31

2. Definitions of Materiality 33

2.a. Can a Definition of Materiality Be Given? 33

2.b. Summary of Definitions 39

2.c. US Supreme Court’s Definition 39

2.d. FASB (1985), CON 2 40

2.e. SEC Rules and Regulations 41

2.f. Common Law 43

2.g. IASB Framework 43

2.h. Common Conceptual Framework 43

2.i. The International Financial Reporting Standards 44

2.j. Auditing Standards 45

2.k. COSO Framework 45

2.l. AccountAbility 46

2.m. Integrated Reporting 46

2.n. WRI and WBCSD 46

3. Attributes of Materiality 47

3.a. Subject Matter 47

3.b. What Is an Item? 47

3.c. An Item versus Its Content 48

3.d. Omissions or Misstatements 49

3.e. Material Disclosures of An Item versus Its Required

Disclosures 50

3.f. Materiality Test from Users’ Perspective 50

3.g. Materiality Test Contrasted with the Objective of

General-Purpose Financial Statements 51

3.h. Materiality Test from the Standpoint of Objective

Metrics 52

3.i. Addressees of Test 52

3.j. Reasonable Investor and Reasonable Person 52

3.k. Clusters versus Individuals 53

3.l. Primary versus Intended versus Other Users 53

3.m. Stakeholders versus Users 54

3.n. Assessor 55

3.o. Degree of Likelihood 55

3.p. Understanding Influence versus Influencing 57

3.q. Degree of Magnitude 59

3.r. Context 59

viii Contents

11.

3.s. Degree ofSpecificity 60

3.t. Time Horizon 60

Solutions and Recommendations 61

Conclusion 67

Part III. Actors and Models of Materiality 69

Main Focus of Part III 70

1. Uses and Effects of Materiality 70

1.a. Is Materiality Exclusively a Legal Concept? 70

1.b. Are Legal and Accounting Definitions of Materiality

Incompatible? 71

1.c. Practical Interactions of Legal and Accounting

Concepts of Materiality 73

1.d. The Different Nature of an Accounting Concept of

Materiality 74

1.e. The Quest for an Accounting Definition of Materiality 75

1.f. Materiality in Audit versus in Financial Statements 76

1.g. Other Uses of Materiality by Auditors 77

1.h. Materiality as a Managerial Concept 79

2. Who Decides about Materiality? 79

2.a. Who Allows Materiality? 79

2.b. Who Uses Materiality? 80

2.c. Who Decides Materiality? 80

2.d. Who Assesses Materiality? 81

3. Models of Materiality 82

3.a. Do We Need a Framework of Materiality? 82

3.b. A Positive versus a Negative Concept 82

3.c. A Discrete versus a Continuous Notion 83

3.d. Different Disclosure Regimes 85

3.e. Simulating User Decision Model 86

3.f. Probability/Magnitude Mapping 86

3.g. Severity of Deviancies 90

3.h. Range of Fluctuation 91

3.i. Opportunity Loss 91

3.j. Statistical Use of Information 91

3.k. Doctrine of Differential Disclosure 92

3.l. Expanded Dimensions of Materiality 95

3.m. The Flexibility Zone 97

3.n. Eyes of Management versus Eyes of Investors 98

3.o. The Ownership Triangle 100

3.p. Active versus Passive Role 101

3.q. The Sender Receiver Distortion 102

Contents ix

12.

3.r. U-Materiality 103

3.s.Objective versus Subjective Determination 103

3.t. Materiality as a Planning Tool 104

3.u. Consensus Materiality 104

3.v. Adjustment Method 105

3.w. From Materiality to Materiality Determination Process 106

3.x. Qualitative Factors 106

3.y. Zero Materiality 107

Solutions and Recommendations 107

Conclusion 112

Part IV. Application of Materiality 113

Main Focus of Part IV 114

1. Materiality Applied to Recognition and Measurement 114

1.a. Does Materiality Apply to Recognition and

Measurement? 114

1.b. Inapplicability by Analogy 115

1.c. De Minimis 115

1.d. Significant Accounting Policies 115

1.e. Accounting Policies with Immaterial Effects 117

1.f. Scope of a Change in Accounting Policies 117

1.g. Materiality in Disclosing Voluntary Changes in

Accounting Policies 117

1.h. Materiality in Disclosing Involuntary Changes in

Accounting Policies 118

1.i. The Case of Accounting Errors 119

2. Materiality Applied to Presentation and Disclosure 120

2.a. Does Materiality Apply to Presentation and

Disclosure? 120

2.b. An Item versus Information of An Item 122

2.c. Required Disclosure of Immaterial Information 122

2.d. Allowed Disclosure of Immaterial Information 123

2.e. The Disclosure Overload Debate 124

2.f. Obscuring Material Information 125

2.g. Minimum Set of Required Disclosures 126

2.h. Classification 127

2.i. Interaction of Aggregation and Disaggregation of

Information 128

2.j. Top-down Model of Disaggregation in the Financial

Statements 129

2.k. Bottom-up Model of Aggregation in the Financial

Statements 130

x Contents

13.

2.l. Classes ofAggregation 132

2.m. Alternative Model of Aggregation in the Financial

Statements 133

2.n. General Models of Disaggregation for Disclosure

Purpose 134

2.o. Review Assessment 137

2.p. Quality of Disclosure 138

2.q. Material Items 138

2.r. Disclosure Objectives 139

2.s. Gains and Losses 140

2.t. Effect of Measurement Bases 140

2.u. Third Statement of Financial Position 141

2.v. Rounding 141

2.w. When Required Disclosure Is Not Enough 142

3. Materiality Applied to Management Commentary 143

3.a. Management Commentary versus the Notes 143

3.b. Views of Materiality in Management Commentary 144

3.c. Material Known Trends or Uncertainties in SEC’s

MD&A 145

3.d. Material Changes 149

3.e. Critical Accounting Estimates in MD&A 149

3.f. Immaterial Information in MD&A 150

3.g. Segment Analysis 150

3.h. Layered Disclosure 151

4. Does Materiality Apply to Bookkeeping? 151

4.a. Bookkeeping versus Financial Statements:

A Separate Perspective 151

4.b. Bookkeeping versus Financial Statements:

An Integrated Perspective 152

4.c. The Direct Impact on Financial Statements of

Bookkeeping Errors 153

4.d. The Indirect Impact on Financial Statements of

Bookkeeping Errors 153

4.e. The Delicate Link to Intentional Immaterial Errors 154

4.f. Immaterial Misstatements versus Bookkeeping Errors 155

4.g. Can Immaterial Bookkeeping Errors Be Left

Uncorrected? 155

4.h. Does Materiality Apply to Bookkeeping? 156

4.i. Reasonableness versus Materiality 156

4.j. Legal Implications 157

4.k. Should Accountants Care of Materiality at All? 158

5. Materiality in Auditing 159

5.a. Audit Definition of Materiality 159

Contents xi

14.

5.b. Definition ofMaterial Misstatement 160

5.c. The Risk of Material Misstatements and Assertions 161

5.d. Relationship between Audit Risk and Materiality 162

5.e. Iteration of Materiality and Inherent Risk 165

5.f. Second-Guessing Management’s Determination of

Users’ Needs 166

5.g. Timing of Auditor’s Consideration of Materiality 166

5.h. Undetected, Identified, Uncorrected, and Corrected

Misstatements 168

5.i. How Materiality Affects Auditors’ Responses to

Misstatements 168

5.j. How Materiality Affects Auditors’ Responses to Fraud 169

5.k. How Materiality Affects Auditors’ Responses to Illegal

Acts 170

5.l. Communications with the Management, Internal

Auditors, and Audit Committee 171

6. Materiality Applied to Internal Control Over Financial

Reporting 172

6.a. Internal Control over Financial Reporting versus Audit 172

6.b. Materiality and Technical Classifications of Internal

Control Deficiencies in SOX 173

6.c. Materiality and Internal Control Deficiencies in

COSO Framework 174

6.d. Materiality in PCAOB Audit Standard for ICOFR 175

6.e. Definition of Risk 175

6.f. Risk Tolerance 176

6.g. Risk Appetite 177

6.h. Risk Appetite and Risk Tolerance in the Context of

Corporate Guidance Systems 177

6.i. Interlock of Risk, Risk Appetite, Risk Tolerance, and

Precision of Internal Controls 178

6.j. Relationship between Risk Tolerance and Materiality 180

6.k. Planned Materiality versus Risk Tolerance and

Performance Materiality 181

6.l. Relationship between Risk Tolerance and Precision

of Controls 181

6.m. Inherently Imprecise Controls 183

6.n. Other Drivers of the Precision of Controls 183

6.o. The Importance of Immaterial Misstatements

in ICOFR 184

6.p. Documentation of Determination of Immateriality 185

6.q. Role of Materiality in Testing ICOFR 185

6.r. Management Review Controls 186

xii Contents

15.

Solutions and Recommendations187

Conclusion 197

Part V. Assessing Materiality 199

Main Focus of Part V 200

1. Types of Assessment and Professional Judgment 200

1.a. Quantitative versus Qualitative Criteria 200

1.b. Is Quantitative an Assurance? 202

1.c. Is Magnitude Exclusively a Quantitative Concept? 202

1.d. What Is the Meaning of Qualitative? 203

1.e. When a Qualitative Assessment Is Always Required 204

1.f. When a Fact Is Always Material 204

1.g. Management Discretion 208

1.h. Auditor and Other External Professional Judgment 210

1.i. How Can the Management Judgment Be Professional? 211

1.j. What Is the Scope of Professional Judgment? 212

1.k. Who Is a Professional Judge? 213

1.l. When Is the Judgment Process Professional? 213

1.m. Documentation of Judgment 214

1.n. How to Evaluate Judgment Reasonableness? 214

1.o. Changes in Judgment and Reassessment 216

2. Quantitative Thresholds of Materiality 217

2.a. Thresholds for Whom? 217

2.b. Role of Quantitative Thresholds 217

2.c. The Case of an Absolute Dollar Amount 218

2.d. When a Relatively Small Misstatement May Be

Material 219

2.e. When a Large Misstatement Can Be Immaterial 219

2.f. Performance Materiality 221

2.g. The Adjustment Method 223

2.h. Process Analysis of Materiality 223

2.i. Should the Management Use Materiality

Set by Auditors? 223

3. Levels of Application of Materiality 224

3.a. The Concept of Whole Financial Statements 224

3.b. Periods of Whole Financial Statements 225

3.c. Materiality at Lower Levels 225

3.d. Consolidated versus Entity or Separate Financial

Statements 227

3.e. Component Materiality 227

4. Benchmarks 231

4.a. Common Benchmarks 231

Contents xiii

16.

4.b. Relative versusAbsolute Measures 232

4.c. Rules of Thumbs Used in Practice 232

4.d. Choosing Benchmarks 234

4.e. Normalizing Benchmarks 235

4.f. Deciding Percentages 236

4.g. Volatility 236

4.h. Industry Type 237

4.i. Capital Structure 237

4.j. Company Life Cycle 238

4.k. Pervasiveness 238

4.l. Degree of Aggregation 239

5. Comparative Information 239

5.a. Basic Period in Focus 239

5.b. Materiality in Prior Period 240

5.c. Corresponding Figures versus Comparative Financial

Statements Approach 240

5.d. Third Statement of Financial Position 243

5.e. Materiality in Future Periods 243

5.f. Uncorrected Immaterial Misstatements Adding

Up to Materiality in the Current Period 244

5.g. Effect of Changes of Materiality Benchmarks 250

5.h. Effect of Misstatement of Comparative Information 250

5.i. Counterbalancing and Noncounterbalancing

Misstatements 251

5.j. Structure of the Notes 252

5.k. Effect on Financial and Forensic Analysis 252

6. Estimates 253

6.a. Risk of Material Misstatement of an Accounting

Estimate 253

6.b. Inherent Level of Imprecision of an Accounting

Estimate 254

6.c. The Linkage between Estimation Uncertainty and

Materiality 254

6.d. Judgmental Misstatements 256

6.e. The Linkage between Inherent Imprecision and

Misstatements 257

6.f. Management Bias 258

6.g. Effect of Materiality on Changes in Estimates 259

6.h. Linkage between Materiality and Sources of

Estimation Uncertainty 259

6.i. Critical Accounting Estimates 260

6.j. Effect on Reliability of Materiality of a

Misstatement of Estimate 261

xiv Contents

17.

7. Individual versusCumulative Misstatements 261

7.a. Analysis at Individual Item Level 261

7.b. Analysis at a Cumulative Level 262

7.c. Offsetting Misstatements 262

7.d. Aggregation Technique and Absolute Value 263

7.e. Trends and Ratios 263

8. Verification 264

8.a. Assessing Decisions 264

8.b. Documentation 265

8.c. Approaches to Verify Materiality Ex Post 265

8.d. The Implication in Terms of Accounting Changes 266

8.e. Methods to Assess Estimates 267

9. Immaterial Misstatements 267

9.a. Does GAAP Really Not Apply to Immaterial Items? 267

9.b. Are Misstatements of Immaterial Items Errors? 269

9.c. Intentional Immaterial Misstatements 269

9.d. Does Intention Make a Misstatement Always Material? 270

9.e. How to Judge Intentions? 271

9.f. The Difference between Achieving a Particular

Presentation and Influencing Users 271

9.g. Investigating the Objective Element 272

9.h. A Policy to Ignore Immaterial Misstatements 272

9.i. Are Immaterial Misstatements Relevant to an Audit? 273

9.j. Material Effect of Accumulation of Immaterial Errors 273

9.k. Correction of Immaterial Errors 274

9.l. Tone from the Top 275

9.m. Legal Consequences 275

9.n. Summary of Treatment of Errors 275

10. Assessing Materiality in Interim Reporting 277

10.a. Reference Period of Materiality under IFRS 277

10.b. Reference Period of Materiality under US GAAP 278

10.c. Materiality in Interim Reporting for

Correction of Errors 278

10.d. Materiality in Interim Reporting for Changes in

Estimates and Changes in Accounting Policies 279

10.e. Relationship between Materiality to Interim and

to Annual Financial Statements 280

10.f. Relationship between Estimation Uncertainty and

Materiality in Interim Periods 281

10.g. Materiality for the Condensed Format of Interim

Financial Statements 283

10.h. Audit Considerations 283

10.i. Interim Periods in MD&A 284

Contents xv

18.

11. Assessing Materialityin Segment Reporting 285

Solutions and Recommendations 287

Conclusion 300

Part VI. The Materiality Determination Process 301

Main Focus of Part VI 302

1. Processes and Methods 302

1.a. Linkage to the Judgment Process 302

1.b. Frameworks to Determine Materiality 302

2. Accounting-derived Approaches 303

2.a. The Qualitative Factors 303

2.b. The IASB’s Four-Step Approach 303

3. Audit-derived Approaches 304

3.a. Audit Procedures 304

3.b. Audit Red Alerts 304

3.c. Materiality Benchmark Selection 310

3.d. Analytical Procedures 311

4. Risk-derived Approaches 311

4.a. Risk-Level Graphs 311

4.b. Heat Maps 311

5. Approaches Derived from Larger Frameworks 312

5.a. Materiality Determination in Integrated Reporting 312

5.b. Materiality Determination in AA1000 313

5.c. The Materiality Matrix 314

5.d. Five-Part Materiality Test 315

5.e. Significance/Influence Matrix 315

5.f. The Materiality Map 316

6. Disclosure of the Materiality Process 316

6.a. The Integrated Reporting Disclosures of the Materiality

Process 316

6.b. The GRI Disclosures of the Materiality Process 317

7. Model Disclosures of Material Matters 317

7.a. General Disclosures in Accounting Standards 317

7.b. General Disclosures in Audit Standards 318

7.c. Disclosure of Material Matters in Integrated Reporting 319

7.d. Disclosure of Material Aspects in Sustainability

Reporting 319

7.e. ITAC Principles-based Disclosures 320

Solutions and Recommendations 320

Conclusion 323

xvi Contents

19.

Part VII. WhereStandard Specifically Require Materiality

Judgments 325

Main Focus of Part VII 326

1. Is Materiality Standard-Specific? 326

2. What Standards Say Users Want 326

3. The Notion of Inconsequential or Perfunctory 340

4. Materiality Applied to Specific Unit of Account 341

4.a. Materiality to Assess Performance Obligations 341

4.b. Materiality of a Financing Component 341

4.c. Materiality of a Customer Option 341

5. Related Parties 341

6. Materiality Applied to Specific Items or Circumstances 345

Solutions and Recommendations 345

Conclusion 346

Part VIII. Accounting Materiality in the Real World 347

Main Focus of Part VIII 348

1. The Materiality Paradox 348

2. Improvement of the Effectiveness of Financial Statements:

The Standard-Setters’ View 348

3. Behavioral Issues 349

4. Is There Something Missing? 350

5. Materiality Comments on SEC Staff IFRS Reviews 351

6. Typical Materiality Abuses by Management 354

6.a. Uses and Misuses of Materiality 354

6.b. Failure to Disclose 355

6.c. Below Materiality Threshold 355

6.d. Setting Materiality High 356

6.e. Ignoring Aggregation Risk 357

6.f. Aggregated Benchmarks 357

6.g. Offset 357

6.h. Static versus Dynamic Benchmarks 358

6.i. Income Statement Orientation 358

6.j. The Presentation versus Disclosure Game 359

6.k. The Change in Materiality Game 360

6.l. Undue Cost or Effort or Impracticability 360

6.m. Contra-Asset and Provision Items 360

6.n. Income Shifting 361

6.o. Unbundling Misstatements 361

xvii

20.

6.p. Statements WereAudited 362

6.q. Absolute Amounts 363

6.r. Too Difficult to Understand 364

6.s. Too Far in Time 364

6.t. Agency Conflicts 365

6.u. Management Commentary 365

6.v. Watering Information 366

6.w. Reclassifications and Continuous Restatement 366

6.x. Change in Judgment 367

6.y. Entity’s Circumstances Are Different 368

6.z. Focus on Consolidated Financial Statements 368

6.aa. Delegation to a Service Organization 369

6.bb. Shooting a Moving Target 369

6.cc. Persistent Behaviors 370

6.dd. Manual Adjustments 371

6.ee. Incorrect Bookkeeping 371

Solutions and Recommendations 371

Conclusion 372

References 373

Index 397

xviii Contents

21.

List of Figures

PartII

Figure 1 Qualitative Characteristics under the IASB (1989)

IASB Framework (reframed to compare with the

FASB, 1985, CON 2). . . . . . . . . . . . . . . . . 12

Figure 2 Qualitative Characteristics under the Common

Conceptual Framework (reframed to compare

with the FASB, 1985, CON 2). . . . . . . . . . . . 13

Figure 3 Qualitative Characteristics under the IPSAS

Framework (reframed to compare with the FASB,

1985, CON 2). . . . . . . . . . . . . . . . . . . . . 14

Figure 4 Relevance and Materiality in FASB (1985), CON 2. 17

Figure 5 Relevance and Materiality in the IASB (1989),

IASB Framework. . . . . . . . . . . . . . . . . . . 18

Figure 6 Relevance and Materiality in Integrated

Reporting. . . . . . . . . . . . . . . . . . . . . . . 19

Figure 7 Reliability and Materiality in FASB (1985), CON 2. 22

Figure 8 Reliability and Materiality in the IASB (1989),

IASB Framework. . . . . . . . . . . . . . . . . . . 23

Figure 9 Relationships between Materiality, Relevance,

Completeness, and Reliability in FASB (1985),

CON 2. . . . . . . . . . . . . . . . . . . . . . . . 24

xix

22.

Figure 10 Relationshipsbetween Materiality, Relevance,

Completeness, and Reliability in the IASB, 1989,

IASB Framework. . . . . . . . . . . . . . . . . . . 25

Figure 11 Comparisons of Definitions of Materiality.. . . . . 34

Part III

Figure 12 A Positive versus a Negative Concept of

Materiality. . . . . . . . . . . . . . . . . . . . . . 83

Figure 13 Graduation of Materiality. . . . . . . . . . . . . . 85

Figure 14 Material Information in Users’ Decision Process. . 87

Figure 15 Multiplying Risk-Level Graphs. . . . . . . . . . . 88

Figure 16 Decoupled Effect Risk-Level Graphs.. . . . . . . . 89

Figure 17 Single Effect Risk-Level Graphs. . . . . . . . . . . 89

Figure 18 Recognition versus Disclosure along the

Likelihood Axis.. . . . . . . . . . . . . . . . . . . 90

Figure 19 The Materiality/Disclosure Dilemma. . . . . . . . 94

Figure 20 Possible Dimensions of Materiality. . . . . . . . . 96

Figure 21 The Flexibility Zone. . . . . . . . . . . . . . . . . 97

Figure 22 Eyes of Management versus Eyes of Investors. . . 98

Figure 23 The Ownership Triangle. . . . . . . . . . . . . . . 100

Figure 24 Materiality as a Planning Tool. . . . . . . . . . . . 104

Figure 25 Consensus Materiality. . . . . . . . . . . . . . . . 105

Part IV

Figure 26 IFRS Disaggregation or Aggregation Model for

Presentation and Disclosure. . . . . . . . . . . . . 128

Figure 27 Materiality Dimensions for Disclosure.. . . . . . . 137

Figure 28 Disclosure Based on Disclosure Relevance. . . . . 137

xx List of Figures

About the Author

FrancescoBellandi, US CPA (Certified Public Accountant);

CGMA (Certified Global Management Accountant); Dottore

Commercialista (Italian Chartered Accountant); Diploma in

International Financial Reporting from the ACCA (The

Association of Chartered Certified Accountants, UK); Degree in

Economics (summa cum laude), LUISS University; M.B.A., SDA

Bocconi School of Business, Bocconi University; Diploma in

Private Equity from the A.I.F.I. (Italy’s private equity association).

Francesco Bellandi is a practitioner in US GAAP/IFRSs dual report-

ing. Named by the AICPA as a worldwide IFRS US GAAP Subject

Matter Expert, he is a member of the AICPA, the NYSSCPA (New

York State Society of Certified Public Accountants), the NYSSCPA’s

International Accounting & Auditing Committee where he has chaired

the IFRS and the FASB subcommittees. He has been an Editorial Review

Board Member of The CPA Journal, New York, USA.

Francesco Bellandi is a forensic auditor. He has served as a board

director, chief financial officer, and finance director in several mul-

tinational companies around the globe and contract university

professor in Audit and in IFRS.

He has authored several publications, including two books pub-

lished by Wiley & Sons, 2012: The Handbook to IFRS Transition and

to IFRS U.S. GAAP Dual Reporting and Dual Reporting for Equity

and Other Comprehensive Income under IFRS and U.S. GAAP.

He can be reached at francesco bellandi@yahoo.com or francesco.

bellandi@dualgaap.com.

xxv

27.

Preface

For financial statementneophytes, materiality looks like a philo-

sophical issue, thought to be of little importance to practitioners

and financial statements preparers adept to hard life. Yet, most of

the internal management battles for what to filter through the

internal reporting layers and what and how to disclose it in the

external financial statements run on the verge of materiality.

Experienced financial statements preparers know that much of

the discussion at the top management and board levels is on what

to or not to present and disclose, justified on the grounds of mate-

riality, but often for some other reason indeed. Auditors know

that unless they can prove that a misstatement is material, their

bullet would be smoothed. And if they did uncover something,

they would pray that it was immaterial. Forensic analysts are

aware that when a company says that something is not material,

this alone is a good reason to investigate what this statement is

trying to conceal.

Materiality is a slippery issue. Being so difficult and tricky, the

FASB appears determined not to search for its definition in an

accounting context. Standard-setters must serve a large audience,

from preparers to investors. But preparers, indeed, are also among

their stakeholders. They must find some trade-off: accounting is

not for scientists and cannot be so difficult to be impossible or

excessively costly. So, preparers push for materiality, invoking

users, but really do users invoke materiality? Is this license too

wide? It depends on how sophisticated the glasses of readers are,

and from what angle they are viewing the scene. What could seem

xxvii

28.

a departure fromGAAP may in essence be acceptable as — some-

body heard the auditor saying — it is not material. In a win-win

situation, proving immateriality may give apparent relief to man-

agement for light sins and on the other hands be a useful defense

to auditors. Investors, at least the most sophisticated of them, and

financial analysts would rather have more information, because

they know how to decide what is material to them. Securities

regulators are obviously stricter than standard-setters.

Take it to the limit, somebody may have said after the fact, that

it was too an immaterial issue to be of interest to users, and so this

statement would be used to prove that before the fact there was

an intent of fraud. The Court may have to say the last word.

This book offers an integrated perspective of materiality from

the different angles of accounting standards for annual, interim,

and segment reporting (including IFRS, US GAAP and SEC Rules

and Regulations), auditing standards (including US and inter-

national ones), internal control over financial reporting, manage-

ment commentary, financial analysis and management control,

forensic analysis, sustainability reporting, corporate responsibility,

assurance standards, integrated reporting, and limited legal

considerations.

Part I introduces the background, including the scenario of

the current debate as part of the IASB’s Disclosure Initiative,

the FASB’s Disclosure Framework and the SEC’s Disclosure

Effectiveness Initiative.

Part II contrasts the views of the accounting conceptual frame-

works. It then compares the definition of materiality in different

standards and contexts, to then draw a taxonomy of materiality

and its attributes.

Part III reviews the uses and effects of materiality as an account-

ing, legal, audit, and managerial concept. It counterbalances

the interests and positions of the various stakeholders involved,

such as investors, preparers, standard-setters, auditors, regulators,

financial analysts, and other users of the financial statements. It

then capitalizes on the author’s vast experience in industry to

devise alternative and complementary models of materiality with

their pros and cons.

xxviii Preface

29.

Part IV providesreaders with interlinked guidance in account-

ing and audit about the extant requirements for the application of

materiality to recognition, measurement, presentation and disclo-

sure in the financial statements. It also expands to issues that are

typical of management commentary. It informs about the com-

plexities and subtle differences between financial statements and

bookkeeping on the subject. Two full sections cover the applica-

tion of materiality in auditing and in internal control over financial

reporting, respectively.

Part V of the book goes into the details of how to assess materi-

ality. It draws from a plethora of different disciplines to go to the

essence of the very meaning and application of professional judg-

ment and its multifaced aspects in specific scenarios and decisions.

This section goes into practical guidance that rarely can be found

on a such judgmental topic.

Part VI illustrates different approaches concerning the processes

and methods that an entity can establish to determine materiality.

Given the highly subjective nature of materiality assessments,

proper processes, systems and methodologies are at the forefront

of the recent and future developments in this area.

Part VII tackles specific issues of application of materiality. This

section includes an illustration of SEC Staff comments on material-

ity in the review of Form 20-F of foreign private issuers and a

checklist of specific accounting pronouncements relating to spe-

cific materiality decisions.

Part VIII of the book wraps up the whole content in showing

how an experienced professional can handle discussions with

management to uncover inappropriate schemes, manipulation tac-

tics, if not frauds.

Preface xxix

30.

I

▾

Part

Introduction and

Background

Abstract

Part Iintroduces the background of why materiality matters in

financial statements. One of the main reasons for determining

whether a fact is material is to check whether its misstatement

overtakes the watershed which makes financial statements not

comply with the relative financial reporting framework.

This part also introduces one of the themes of the book: the

interaction of the views of the different subjects involved in

materiality assessment, i.e., users, preparers, auditors, regula-

tors, and the related conflicts of interest. Materiality plays a

different role in this depending on who is looking at it.

The part also comprises an overview of the main projects underly-

ing the current debate about materiality, that is, the International

Accounting Standards Board’s Disclosure Initiative, the Financial

Accounting Standards Board’s Disclosure Framework and the

SEC’s Disclosure Effectiveness Initiative, including a list of their

main steps and documents issued to date.

Keywords: Accounting; Compliance; Disclosure; Effectiveness;

IASB; IFRS; Impracticability; Initiative; Maturity; Override;

SEC; Undue; US GAAP

1

31.

Main Focus ofPart I

1. Why Does Materiality Matter in Financial Statements?

First and foremost, materiality in financial reporting is the focus of

the lens of financial statement users in making their economic

decisions. The Financial Accounting Standards Board (FASB) and

International Accounting Standards Board (IASB) conceptual fra-

meworks contemplate this as the main argument, as discussed in

Paragraph II.1 below.

However, in practice, materiality is so important is for its impli-

cations for preparers of financial statements and auditors. In fact,

International Financial Reporting Standards (IFRS) presumes that

compliance with IFRS results in financial statements achieving fair

presentation of the financial position, financial performance, and

cash flows of an entity. IFRS compliance means that the financial

statements adhere to all the requirements of IFRS. The notes must

state an explicit and unreserved statement to this respect. Any

departure from IFRS requirements would undermine such compli-

ance of the whole financial statements, unless:

1. the management concludes and discloses that in an

extremely rare circumstance compliance with IFRS would be

so misleading to conflict with the objective of the financial

statements specified in the Framework;

2. applying an IFRS requirement has a material effect, but the

IASB has explicitly provided for an impracticability excep-

tion (for its meaning, see Paragraph 1.n below), and the

company is in such an impracticability situation and gives

the specific disclosures as required;

3. applying an IFRS requirement has a material effect, but the

IASB has explicitly provided an exception based on an undue

cost and effort basis (for its meaning, see Paragraph 1.m below);

4. the entity does not provide a specific disclosure required by

the IFRS or does not apply a required accounting policy or

does not correct an error, because such information or the

2 Materiality in Financial Reporting

32.

effects of applyingthe policy or the error is immaterial.

However, the entity cannot use this argument if it does so to

achieve a particular presentation of the financial position,

financial performance, or cash flows (IASB, 2014, IAS 8,

paras. 8, 41, BC24; IASB, 2016, IAS 1, paras. 15, 16, 19, 31,

BC36).

The first situation would be extremely rare. The second and

third situations are strictly defined by the IASB, not by preparers.

Therefore, the management can only resort to a materiality argu-

ment to avoid a departure from Generally Accepted Accounting

Principles (GAAP) having serious consequences. Paragraph V.9.a

below discusses immaterial misstatements.

An entity that describes its financial statements as prepared in

conformity with US generally accepted accounting principles must

also apply all relevant authoritative accounting pronouncements.

This concept is similar to compliance to IFRSs. US GAAP does

not explicitly require a statement of compliance, as compliance is

ordinarily taken for granted. Although it does not mandate an

exact placement, it encourages a separate section before the notes

or as a first note (FASB, 1993, FASB Interpretation no. 40, paras.

Summary, 2, 5, 16; FASB, 2016, FASB ASC 235-10-05-3, 235-10-50-

1, 235-10-50-6). However, US GAAP does not have an overriding

case as described in the first point above. US GAAP also has some

exceptions due to impracticability or undue cost or effort.

Symmetrically, auditors express an opinion on the financial

statements to present fairly the financial position, financial perfor-

mance, and cash flows of the entity, but they attest that this holds

true in all material respects. Drawing a line on what is material per-

mits auditors, on one hand, to assess and respond to financial

statements compliance with GAAP and, on the other hand, defend

themselves against claims concerning their audit work.

2. Powerful and Dangerous

Formally, materiality is assessed from the eyes of the users of

financial statements, yet the management decides it. What lenses

Introduction and Background 3

33.

does the managementuse? If challenged, the management can eas-

ily say that an item is not material and in most occurrences a dif-

ferent opinion would likely be subjective as that of the

management.

Readers of financial statements cannot be aware of something

that is not recognized, not measured, or not presented if this fact

is not disclosed. They cannot be aware of something that is not

disclosed.

In theory, the management would be able to justify virtually

everything based on materiality, also because a fact cannot be

challenged until another party becomes aware of it. If this hap-

pens, the management would be most of the time able to dis-

charge its liability on the grounds of professional judgment.

From all these perspectives, it is evident why a loose concept of

materiality is powerful but dangerous at the same time. It presup-

poses a high level of maturity of management and a strong sense

of business ethics, a solid system of checks and balances in corpo-

rate governance, and an effective regulatory enforcement.

3. The Disclosure Framework

Much of the recent development on materiality takes its origin

from the Disclosure Framework project (FASB, 2012, File no. 2012-

220). The FASB added this project in its agenda in July 2009 and

issued an Invitation to Comment in 2012. It pursued a field study

in 2013.

The FASB and the AICPA’s Center for Audit Quality-sponsored

forums on financial statement disclosure effectiveness at Columbia

University’s Center for Excellence in Accounting and Security

Analysis on October 4, 2012 and at Stanford University Graduate

School of Business on October 8, 2012 (Center for Audit Quality,

2012).

Several organizations have contributed with their independent

analyses and studies, including the EFRAG, the IAASB, the ASB,

the FRC, the ICAEW, the CPA Institute, and others as mentioned

in several sections of this book.

4 Materiality in Financial Reporting

34.

Concurrently, the FASBis carrying out the Simplification

Initiative, which consists in a series of a narrow-scope short-term

project to simplify accounting standards and reduce their cost and

complexity. The current projects include:

Balance Sheet Classification of Debt;

Nonemployee Share-Based Payment Accounting Improvements;

Accounting for Financial Instruments — Hedging;

Liabilities and Equity — Targeted Improvements.

4. The Disclosure Initiative

In the IASB’s world, the Disclosure Initiative is the analog to the

Disclosure Framework. Regarding materiality, the project has pro-

duced certain amendments to IAS 1 and the Practice Statement on

materiality. Further discussion on the definition of materiality is

expected to be part of the Principles of Disclosure project within

the Disclosure Initiative.

Both the FASB’s Disclosure Framework and the IASB’s

Disclosure Initiative projects intent to improve the overall disclo-

sures and the notes to the financial statements through enhanced

effectiveness of information. It can be argued that this is the

underlying motif of every system of information, and in fact virtu-

ally all financial reporting standards and management reporting

systems worldwide deal with sorting out a hierarchy of qualities

of accounting and financial information. Materiality is only one of

several aspects treated in the Disclosure Initiative, centered into

the difficulties in applying materiality in practice which have been

mostly portrayed as a conduit to ineffective disclosure (IASB,

2017, PS 2, para. BC2).

Unlike the position of the FASB, where the impossibility to

arrive to an accounting definition of materiality would likely cut

any further discussion short, the IASB anticipated that this will

not significantly affect the short-term conclusions drawn in the

IASB (2017), PS 2 (IASB, 2017, PS 2, para. BC15).

Introduction and Background 5

35.

5. The DisclosureEffectiveness Initiative

The Disclosure Effectiveness Initiative is a review by the SEC

Staff of disclosure requirements, their presentation and delivery

as required by the Jumpstart Our Business Startups Act. In

December 2013, the SEC issued a Staff Report to Congress

about the review of its disclosure requirements in Regulation

S-X and Regulation S-K to facilitate timely and material disclo-

sures. The Fixing America’s Surface Transportation Act (2015)

required the SEC to carry out a study on the modernization

and simplification of the disclosure requirements in Regulation

S-K.

Several documents have been issued in this context, including:

SEC Staff’s Report on Review of Disclosure Requirements in

Regulation S-K — “S-K Study” (The US Securities and

Exchange Commission [SEC], 2013);

SEC Release no. 33-10064, Business and Financial Disclosure

Required by Regulation S-K, April 13, 2016 (SEC, 2016);

SEC Release no. 33-10110, Proposed Rule, Disclosure Update

and Simplification, July 13, 2016 (SEC, 2016);

Report on Modernization and Simplification of Regulation S-

K, November 23, 2016.

On September 25, 2015, the SEC announced that it is seeking

public comment on the effectiveness of financial disclosure of

Regulation S-X. So far, this has produced the Release no. 33-9929,

Request for Comment on the Effectiveness of Financial Disclosures about

Entities Other than the Registrant, September 25, 2015. The SEC will

also review the differences and possible ways of aligning the dis-

closure requirements under the Securities Act of 1933 and the

Securities Exchange Act of 1934, working with the FASB to

address overlapping requirements in US GAAP and SEC rules,

and improve the delivery and navigability of information through

technology.

6 Materiality in Financial Reporting

36.

Some of otherprior documents on the topic include:

Report of the Task Force on Disclosure Simplification, March

5, 1996;

Report of the Advisory Committee on the Capital Formation

and Regulatory Processes, July 24, 1996;

Final Report of the Advisory Committee on Improvements

to Financial Reporting in the United States Securities and

Exchange Commission, August 1, 2008.

6. Objectives of the Book

The objective of this book is twofold. First, it intends to review the

different angles of the literature of materiality and integrate them

into an overall systemic perspective. Second, the book proposes

new ways of looking at materiality that originate from the above

integration of diverse existing disciplines. This entails the consid-

eration of accounting standards, auditing standards, internal con-

trol over financial reporting, management commentary, financial

analysis and management control, forensic analysis, sustainability

reporting, corporate responsibility, assurance standards, inte-

grated reporting, and limited legal considerations.

To accomplish the first objective, the book deals with both the-

ory and practice. It pursues a theoretical analysis of the conceptual

frameworks and of the definitions of materiality. It compares the

actors involved in materiality decisions and their roles. On the

practice side, it analyzes existing guidance on the application and

assessment of materiality and contrasts it to identify gray areas. It

shows real-world illegitimate uses of materiality to misstate finan-

cial results.

To achieve the second objective, the book first creates a taxon-

omy of the materiality attributes that are embedded in the differ-

ent definitions. Then it elaborates the existing views to materiality

or creates new ones, to show that this subject can be seen from

different angles and applied to different contexts. It proposes

attention to the unstated recognition and measurement problems

Introduction and Background 7

37.

of materiality andthe often-found hidden agenda of management

in manipulating financial results. It shows the leading practice of

zero materiality in bookkeeping and advocates a good faith

approach in genuinely separating the understanding of users’ per-

spective from applying the highest standard of due diligence in

accounting practice. In integrating disciplines that are generally

seen separately, it derives practical suggestions on how to assess

and judge materiality, and explains how the management can

reuse tools that other actors, such as auditors or regulators, adopt

to address materiality issues. Finally, it makes a systematic reorga-

nization of materiality determination processes and leading prac-

tice that are at the forefront of future developments.

8 Materiality in Financial Reporting

38.

II

▾

Part

Conceptual Bases

of Materiality

Abstract

PartII contrasts the views of materiality in the Conceptual

Frameworks of the IASB, FASB, IPSAS, and other framework

such as the Integrated Reporting. In particular, it analyzes at

what level and how differently that concept interacts with the

qualitative characteristics of financial information in each of

those frameworks. It looks at its pervasiveness and entity

specificity, the interlock with the concept of relevance, reliabil-

ity and faithful representation, completeness, understandabil-

ity, neutrality, and drills down to the link to recognition.

This part then compares the definitions of materiality in differ-

ent standards and contexts, to then draw a taxonomy of mate-

riality and its attributes, such as the subject matter, the context

of assessment, the addressees, the assessor, and the materiality

test. A large part of the analysis involves the comparison

between legal definitions of materiality and characterizations

in the accounting, financial, and larger management contexts.

Keywords: AA1000; CDSB; framework; GRI; IPSAS; ISO;

qualitative characteristics; relevance; reliability; significance;

supreme court; understandability; WBCSD

9

39.

Main Focus ofPart II

1. Materiality in the Conceptual Frameworks

1.a. The Objective of Materiality

This section illustrates several points of contact between the concept

of materiality and the qualitative characteristics of useful accounting

or financial information. Indeed, usefulness of information is the pri-

mary objective of financial statements in the common Conceptual

Framework, and the interaction of materiality with the features that

qualify such usefulness is its raison d’etre (International Accounting

Standards Board [IASB], 2010, Conceptual Framework, para. OB2),

(IASB, 2017, PS 2, para. 7), (IASB, 2016, IAS 1, para. 9). However,

the level of interaction varies depending on the framework used.

1.b. Level of Interaction in the Conceptual Frameworks

Different financial reporting frameworks have different levels

at which materiality operates in the hierarchy of qualitative

characteristics.

The superseded IASB Framework had four principal qualitative

characteristics, one of which is relevance, and other characteristics

that make the principal ones possible. In this scheme, materiality

mainly interacted with relevance (IASB, 1989, IASB Framework,

para. 24).

Superseded CON 2 had user-specific qualities (understandabil-

ity and decision-usefulness), primary decision-specific qualities

(relevance and reliability), ingredients of the primary quality of

relevance (timeliness, predictive value, and feedback value), ingre-

dients of the primary quality of reliability (representational faith-

fulness, verifiability, and neutrality) and secondary and interactive

qualities (comparability and consistency). Benefits over costs was

the pervasive constraint. Materiality was none of them, but a

threshold for recognition, which affected all qualitative character-

istics and mainly interacted with relevance and reliability (FASB,

1985, CON 2, paras. 32 33).

The IASB and FASB common Conceptual Framework has two

fundamental characteristics (relevance and faithful representation)

10 Materiality in Financial Reporting

40.

and enhancing characteristics.Materiality is an entity-specific

aspect of relevance (IASB, 2010, Conceptual Framework, paras.

QC5, QC11), (FASB, 2010, CON 8, paras. QC5, QC11), although a

FASB, 2015, File no. 2015-300 would delete this from the US side.

Under the International Public Sector Accounting Standards

(IPSAS) framework, materiality affects not only relevance but also

a number of qualitative characteristics of financial or nonfinancial

information (The International Public Sector Accounting

Standards Board [IPSASB], 2013, paras. 3.3, 3.34, BC3.31).

Figures 1 3 picture the qualitative characteristics of the above-

mentioned frameworks and depict the placement of materiality

within each of them.

1.c. A Pervasive Concept or a Qualitative Characteristic?

Under both FASB (1985), CON 2 and the IASB (1989), IASB

Framework, materiality is not a qualitative characteristics of

accounting information. Under both those frameworks, it is a

cross-cutting feature.

Under FASB (1985), CON 2 materiality is a pervasive concept,

instrumental in nature, hence a threshold or screen to discriminate

other qualitative characteristics of accounting information. It does

not interact with only some characteristics but spans over them all

(i.e., a pervasive phenomenon) (FASB, 1985, CON 2, paras. 124,

126).

The IASB (1989), IASB Framework, discusses the interactions of

materiality with relevance, as a threshold or cutoff point to dis-

criminate information that is useful from that is not so (IASB,

1989, IASB Framework, paras. 29 30, 43 45). Indeed, it must be

pervasive if, in deciding to issue a Practice Statement instead of

incorporating guidance on materiality in IAS 1, the IASB gave

weight to the pervasive nature of the subject (IASB, 2017, PS 2,

para. BC6).

IASB (2015), ED/2015/8, seems to use the term pervasiveness in

a different way, though. It seems to use this term as a magnitude

of how many items a misstatement affects in the complete set of

financial statements (IASB, 2015, ED/2015/8, paras. 11, 71). This

might be intended as if pervasiveness would not really refer to the

Conceptual Bases of Materiality 11

scope and applicationof materiality to all items, but the assess-

ment of the overall impact to the whole financial statements.

The above views of materiality not being one of the qualitative

characteristics would to some extent contrast with Integrated

Reporting, where it is one of the six guiding principles, and with

AccountAbility [AA1000], 2008, where materiality, inclusivity, and

responsiveness are the three foundation principles. AccountAbility

[AA1000 AccountAbility Assurance Standard] (2008), as an

Assurance Standard, considers materiality as one of the qualitative

characteristics of corporate responsibility reporting, together with

completeness and responsiveness (Stakeholder Research

Associates Canada Inc., United Nations Environment Programme,

and AccountAbility, 2005, Vol. 2. p. 128).

1.d. Is Materiality a Constraint?

FASB (1985), CON 2, represents materiality as one of the two per-

vasive constraints. The first, benefit of information being greater

than cost, is a prerequisite to justify providing information. The

second, materiality, is the limit within which each of the qualita-

tive characteristics must exist to fit for purpose. The contempora-

neous presence of the qualitative characteristics above that limit

draws the line as a threshold for recognition (FASB, 1985, CON 2,

paras. Summary, 33). The common Conceptual Framework also

interprets FASB (1985), CON 2, in this way.

Under the IASB (1989), IASB Framework, materiality is not part

of the pervasive constraints, which are benefit over costs, the

tradeoff between timely reporting and reliability, and balance

between the qualitative characteristics.

The common Conceptual Framework specifies that, indeed

pervasive, materiality is not a constraint, as an entity would be

able to report immaterial information (IASB, 2010, Conceptual

Framework, para. BC3.18), (FASB, 2010, CON 8, para. BC3.18). The

IASB Disclosure Initiative and the Practice Statement on material-

ity explain the circumstances under which this is possible. This

reading appears to be symmetrical to the one used in FASB (1985),

CON 2, based on which it is a constraint because information to be

Conceptual Bases of Materiality 15

45.

recognized must reflectthe qualitative characteristics in all mate-

rial respects.

The IPSAS framework pushes materiality further as a pervasive

constraint, as it if affects not only relevance but a number of quali-

tative characteristics of financial or nonfinancial information, such

as faithful representation, understandability, or verifiability

(IPSASB, 2013, paras. 3.3, 3.34, BC3.31).

1.e. Interaction with Qualitative Characteristics of Accounting

Information

The span and points of interactions of materiality with the qualita-

tive characteristics are not the same under FASB (1985), CON 2

and the IASB (1989), IASB Framework.

In fact, under FASB (1985), CON 2 materiality interacts with all

the qualitative characteristics, especially relevance and reliability,

to which it works as a qualifying attribute.

Conversely, the IASB (1989), IASB Framework does not dis-

cuss materiality in relation to qualitative characteristics other

than relevance. However, some implicit interdependencies exist,

as it will be seen in the following paragraphs, as summarized in

Figure 10.

1.f. Materiality versus Relevance

In discussing the two concepts of relevance and materiality, FASB

(1985), CON 2, shows that they are very close to each other, as

they are both defined in terms of the effects on the decision-maker.

Information is not relevant when the decision-maker (e.g., investor)

has no need of it. However, information that would be relevant

may be immaterial if it is too small or nor sensitive enough to

make a difference in a decision. In this sense, materiality qualifies

relevance (FASB, 1985, CON 2, paras. 126 127) (Figure 4).

It is interested to see the interlock of the two concepts in the

FASB’s definition of disclosure relevance as part of the Disclosure

Framework as a characteristic of information to change users’

assessment of prospects for cash flows by a material amount

(FASB, 2012, File no. 2012-220, para. 4.4).

16 Materiality in Financial Reporting

46.

In the IASB(1989), IASB Framework, materiality also affects rel-

evance. However, it does not formulate the way this happens as

clearly as FASB (1985), CON 2 does, that is, as a two-step process

in qualifying relevance.

A second difference is that in the IASB (1989), IASB Framework

information may be relevant for its nature, irrespective of material-

ity (IASB, 1989, IASB Framework, paras. 29 30, 43). The nature of

information is here a factor that acts at the same level as material-

ity. Conversely, FASB (1985), CON 2 — like the Accounting

Standards Board (UK ASB, 1999, para. 3.2) — considers nature as

one of the attributes of materiality.

Unlike the IASB (1989), IASB Framework, IASB (2016), IAS 1,

reintroduces nature, not only size, as an attribute of materiality in

its definition. However, as discussed in Paragraph 2.b below, in

the operating guidance about presentation and disclosure it mainly

uses materiality to mean size (Figure 5).

The common Conceptual Framework confirms materiality as a

feature of relevance because, while relevant information may or

may not be material, immaterial information does not per se make

it irrelevant (IASB, 2010, Conceptual Framework, paras. QC11,

BC3.18), (FASB, 2010, CON 8, paras. QC11, BC3.18).

In the Proposed Accounting Standards Update (ASU) on notes,

the FASB concludes that it can broadly define relevance, not mate-

riality. This is a legal concept and its accounting application is left

Relevance?

No Yes

Materiality?

Would it make

a difference?

The more important

the item, the finer the

materiality screen

Figure 4: Relevance and Materiality in FASB (1985), CON 2.

Conceptual Bases of Materiality 17

47.

to management (FinancialAccounting Standards Board [FASB],

2015, File no. 2015-310, para. BC21) (see Paragraph III.1.a below

for a discussion on the legal vs. accounting concept of materiality).

Finally, the FASB Proposed FASB Concepts Statement would

deny the previous view that materiality is an aspect of relevance

(FASB, 2015, File no. 2015-300, para. BC3.18).

The FASB’s invitation to comment the Disclosure Framework

uses the term relevance, not materiality in deciding which disclosure

to produce. It defines relevance of disclosures as the potential to

make an assessment by investors and creditors of prospects for

future cash flows from an equity dividend, loan or other interest

(FASB, 2012, File no. 2012-220, para. Chapter 4). Some participants

to the Center for Audit Quality (CAQ) forums noted that in such a

context the term materiality would be more familiar to preparers

(CAQ, 2012).

The language used by IASB (2015), IFRS for SMEs seems to

assimilate materiality with relevance, i.e., if information is mate-

rial, it is relevant. It defines relevance as capability of influencing

the economic decisions of users, while materiality what could

influence them (IASB, 2015, IFRS for SMEs, paras. 2.5, 2.6).

The Integrated Reporting Framework notes that relevance is

necessary but is not sufficient for materiality to exist. It assesses

materiality in terms of value creation (The International Integrated

Reporting Council, 2013, para. 3.24). In Integrated Reporting,

material matters are those that substantively affect the organiza-

tion’s ability to create value.

Relevance?

-Size

-Circumstances

Nature

Materiality?

Figure 5: Relevance and Materiality in the IASB (1989), IASB

Framework.

18 Materiality in Financial Reporting

48.

While not explicitlystated, the materiality determination pro-

cess (see Paragraph VI.1 below) drills down from relevance to

materiality. Relevant matters are not necessarily material. After

identifying relevant matters, the organization evaluates and priori-

tize their effects in terms of magnitude and likelihood. Those that

are sufficiently important are the material ones.

Likewise, AA1000 (2008) has a process whereas materiality

results from determining both relevance and significance of an

issue (Figure 6).

Unlike the common Conceptual Framework, in the Framework

of the Climate Disclosure Standards Board, a consortium of

business and environmental organizations advocating reporting

of climate change, materiality is a component of both relevance

and reliability (Climate Disclosure Standards Board [CSDB],

2009, p. 8).

Commission of Sponsoring Organizations of the Treadway

Commission (COSO; 2013a) similarly states that materiality sets

the threshold for relevance. Materiality qualifies relevance insofar

as it defines the level of precision and accuracy required to present

the underlying activities, transactions and events within

acceptable limits (COSO, 2013a, p. 66). It uses the term materiality

for financial reporting, while the level of precision and accuracy

for compliance and operations (COSO, 2013a, p. 68). Materiality as

a qualification in terms of precision is an important point that

anticipates the relationship between risk tolerance and the level of

precision of internal controls (Paragraph IV.6.l below).

Relevant

matters

Material

matters

Magnitude /

likelihood

Figure 6: Relevance and Materiality in Integrated Reporting.

Conceptual Bases of Materiality 19

49.

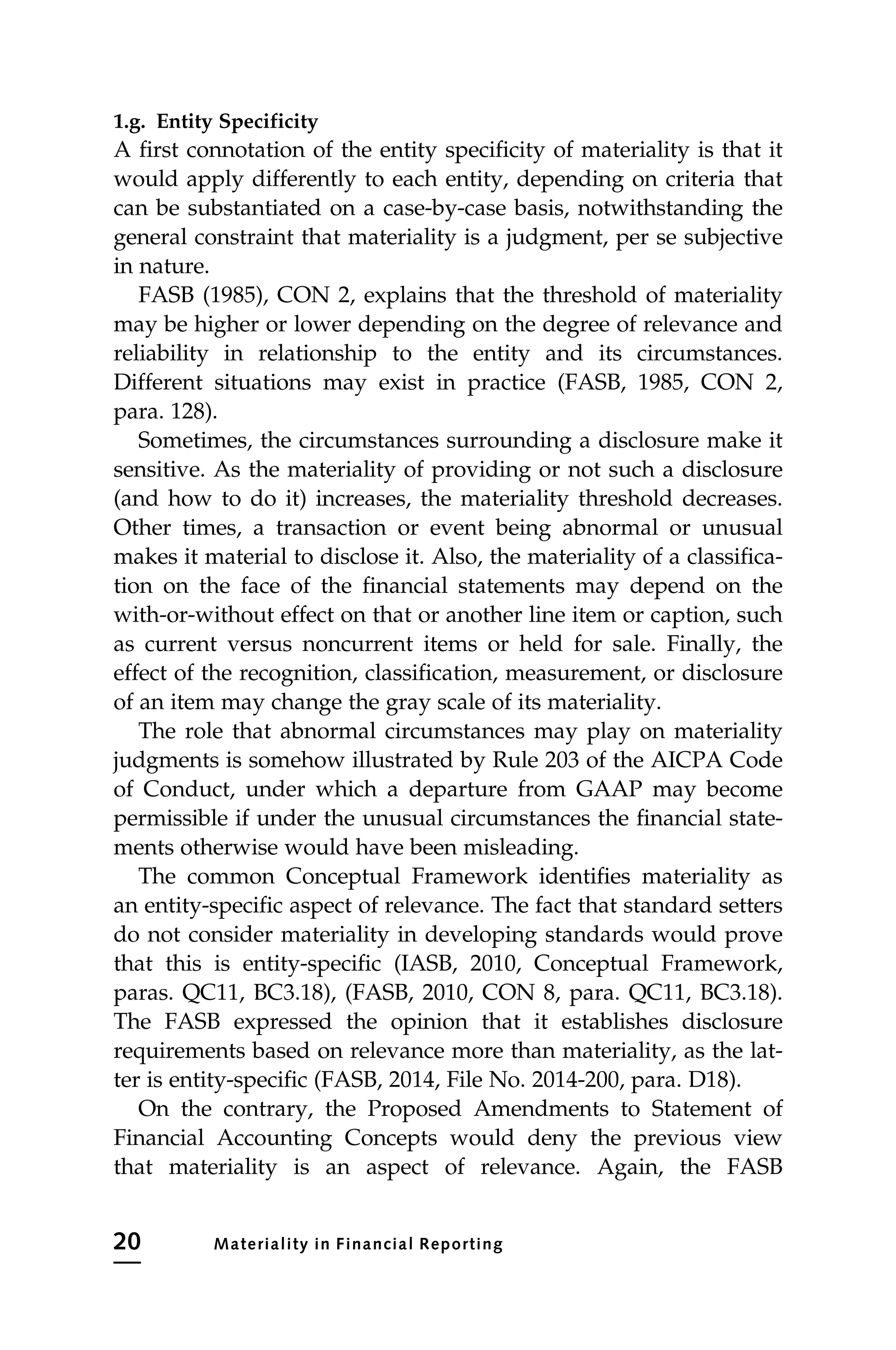

1.g. Entity Specificity

Afirst connotation of the entity specificity of materiality is that it

would apply differently to each entity, depending on criteria that

can be substantiated on a case-by-case basis, notwithstanding the

general constraint that materiality is a judgment, per se subjective

in nature.

FASB (1985), CON 2, explains that the threshold of materiality

may be higher or lower depending on the degree of relevance and

reliability in relationship to the entity and its circumstances.

Different situations may exist in practice (FASB, 1985, CON 2,

para. 128).

Sometimes, the circumstances surrounding a disclosure make it

sensitive. As the materiality of providing or not such a disclosure

(and how to do it) increases, the materiality threshold decreases.

Other times, a transaction or event being abnormal or unusual

makes it material to disclose it. Also, the materiality of a classifica-

tion on the face of the financial statements may depend on the

with-or-without effect on that or another line item or caption, such

as current versus noncurrent items or held for sale. Finally, the

effect of the recognition, classification, measurement, or disclosure

of an item may change the gray scale of its materiality.

The role that abnormal circumstances may play on materiality

judgments is somehow illustrated by Rule 203 of the AICPA Code

of Conduct, under which a departure from GAAP may become

permissible if under the unusual circumstances the financial state-

ments otherwise would have been misleading.

The common Conceptual Framework identifies materiality as

an entity-specific aspect of relevance. The fact that standard setters

do not consider materiality in developing standards would prove

that this is entity-specific (IASB, 2010, Conceptual Framework,

paras. QC11, BC3.18), (FASB, 2010, CON 8, para. QC11, BC3.18).

The FASB expressed the opinion that it establishes disclosure

requirements based on relevance more than materiality, as the lat-

ter is entity-specific (FASB, 2014, File No. 2014-200, para. D18).

On the contrary, the Proposed Amendments to Statement of

Financial Accounting Concepts would deny the previous view

that materiality is an aspect of relevance. Again, the FASB

20 Materiality in Financial Reporting

50.

considers relevance insetting standards for all entities, not materi-

ality (FASB, 2015, File no. 2015-300, para. BC3.18).

Specificity may concern several aspects, including the entity, its

financial report, and the circumstances of its use (IASB, 2014,

Agenda Paper AP3), (IASB, 2014, Agenda Ref 4D).

The FASB reports comments about its 2013 field study that com-

pared materiality to entity-specific relevance. It notes that the lat-

ter is an interpretation of the former. Although the application of

both criteria in the field study leaded to similar conclusions, mate-

riality was more clearly understood and well established (FASB,

2015, File no. 2015-310, para. BC10).

The Fixing America’s Surface Transportation Act (2015) has

required the Securities and Exchange Commission (SEC) to con-

duct a study on the modernization and simplification of disclosure

in Regulation S-K, including emphasis on a company-by-company

approach for relevant and material information (Pub. L. no. 114-94,

129 Stat. 1312, 2015). Such study (SEC, 2016, Release no. 33-10110)

proposes to omit certain disclosures that may be redundant, dupli-

cated, overlapping, outdated, or superseded, in consideration of

other SEC, US GAAP, or IFRS requirements or of changes in the

information environment. The Center for Audit Quality of the

AICPA has favorably commented.

The SEC study, as it would go in the direction of taking into

accounts disclosures that are material because specific to the entity

(Center for Audit Quality, 2016, pp. 4 5).

According to the IASB (2017), PS 2, materiality applies at entity

level (IASB, 2017, PS 2, para. IN5). The traditional position of the

IASB and the FASB is that full guidance on materiality cannot be

given, because of the impossibility to generalize specific situations.

AccountAbility [AA1000SES], 2011, recognizes that materiality

may be stakeholder-specific, as not all the stakeholders may have

the same priorities and issues (AA1000SES, 2011, p. 14). Note that

this is different from entity-specific.

Some give another reading of entity specificity, that is, each

entity should determine materiality. This is a current motive

underlying the recent trend standards (e.g., IASB, 2014, Disclosure

Initiative Amendments to IAS 1) that would favor a loose

Conceptual Bases of Materiality 21

51.

determination by eachentity of what to disclose or not, even in

relation to disclosures required by accounting standards.

1.h. Materiality versus Reliability and Faithful Representation

FASB (1985), CON 2, places materiality as a qualification of reli-

ability. Whether an amount is material firstly depends on the base

on which it is compared. So, its weight relative to the base will tell

whether a rounding or an omission makes the base unreliable,

hence whether that amount is material. This is a quantitative

concept.

Second, the more sensitive the base to the decision-maker is, the

more important that same relative weight would be, hence more

material. This may be either an indirectly quantitative or a qualita-

tive concept. It may also happen that an immaterial error does not

make information unreliable (FASB, 1985, CON 2, paras. 33, 127)

(Figure 7).

If materiality may qualify reliability, immateriality does not

waive unreliability. Paragraph V.4.b below shows the interaction

of percentage metrics of reliability with absolute value of

materiality.

Paragraph V.6.j below treats the issue of what level of material-

ity a misstatement in estimate must have to mean that the estimate

is unreliable.

Reliability?

Materiality?

Would it make

the base

unreliable?

Yes No

The more sensitive

the base, the finer the

materiality screen

Figure 7: Reliability and Materiality in FASB (1985), CON 2.

22 Materiality in Financial Reporting

52.

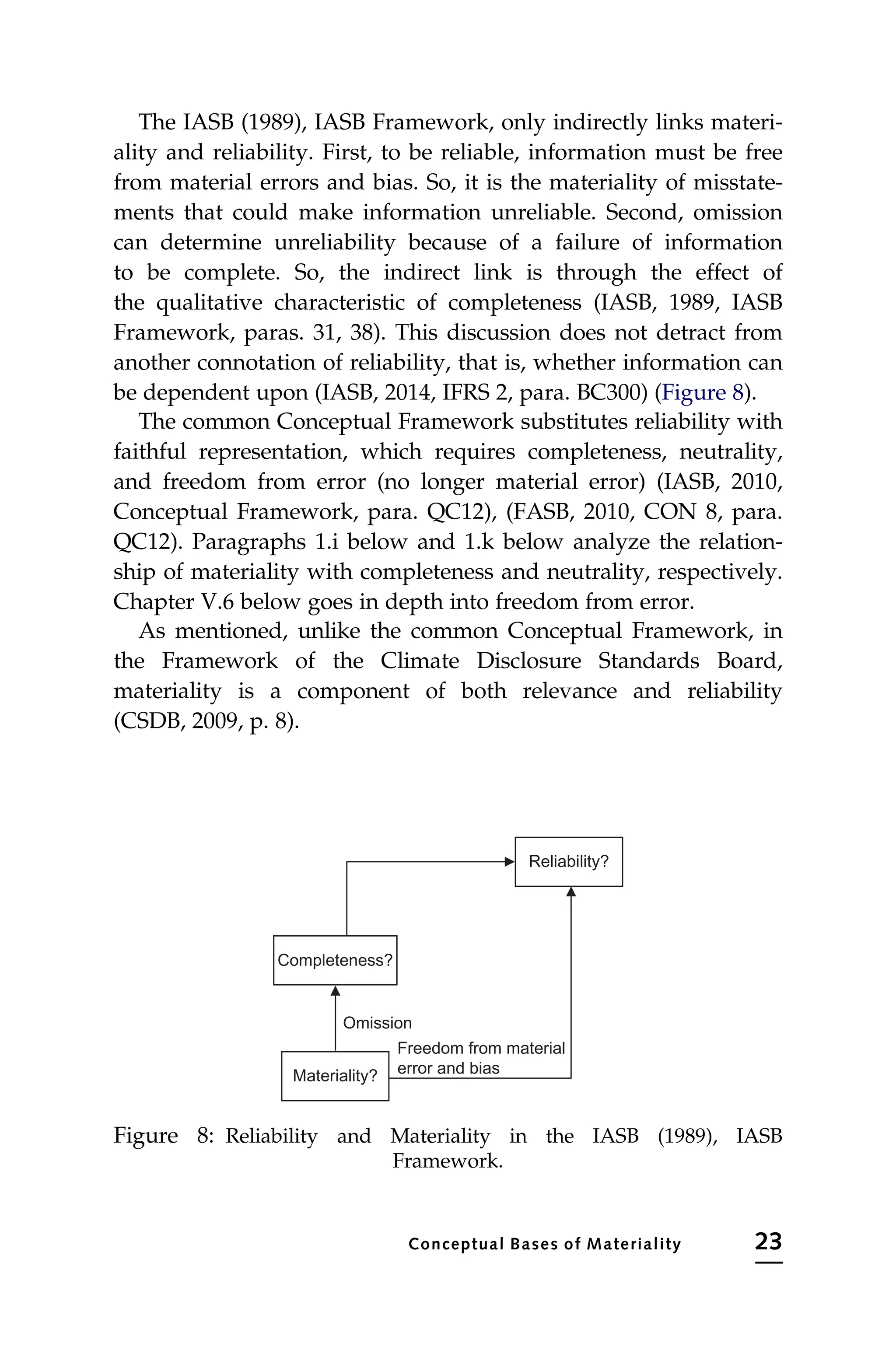

The IASB (1989),IASB Framework, only indirectly links materi-

ality and reliability. First, to be reliable, information must be free

from material errors and bias. So, it is the materiality of misstate-

ments that could make information unreliable. Second, omission

can determine unreliability because of a failure of information

to be complete. So, the indirect link is through the effect of

the qualitative characteristic of completeness (IASB, 1989, IASB

Framework, paras. 31, 38). This discussion does not detract from

another connotation of reliability, that is, whether information can

be dependent upon (IASB, 2014, IFRS 2, para. BC300) (Figure 8).

The common Conceptual Framework substitutes reliability with

faithful representation, which requires completeness, neutrality,

and freedom from error (no longer material error) (IASB, 2010,

Conceptual Framework, para. QC12), (FASB, 2010, CON 8, para.

QC12). Paragraphs 1.i below and 1.k below analyze the relation-

ship of materiality with completeness and neutrality, respectively.

Chapter V.6 below goes in depth into freedom from error.

As mentioned, unlike the common Conceptual Framework, in

the Framework of the Climate Disclosure Standards Board,

materiality is a component of both relevance and reliability

(CSDB, 2009, p. 8).

Reliability?

Completeness?

Freedom from material

error and bias

Materiality?

Omission

Figure 8: Reliability and Materiality in the IASB (1989), IASB

Framework.

Conceptual Bases of Materiality 23

53.

1.i. Completing thePicture: Materiality versus Completeness

Under FASB (1985), CON 2, completeness is part of representa-

tional faithfulness, an ingredient of reliability. So, there is a

double-indirect link between completeness and reliability, medi-

ated by materiality and cost feasibility, based on which omitting

an important fact (where importance may be either in size or

nature) would make the overall information unreliable. Here,

completeness does not only mean omission but also unbiased

measurement. This is a relative concept of completeness, in that

information should cover completely what is material, not neces-

sarily be fully completed. An important point is that even if infor-

mation is complete to the point not to undermine reliability,

omission might still affect relevance if that piece of information is

material (FASB, 1985, CON 2, paras. 79 80). Figure 9 illustrates

these relationships, completing the picture of Figures 4 and 7.

Under the IASB (1989), IASB Framework, lack of completeness

affects both relevance and reliability through an indirect link via

materiality. On one hand, omission means incompleteness; when

this makes information false or misleading (i.e., the omission is

material), information becomes unreliable. So, completeness affects

reliability through materiality. On the other hand, relevance

would be deficient (IASB, 1989, IASB Framework, para. 38). In

instructing the management to develop accounting policies in the

Yes

Relevance? Reliability?

No Yes

Materiality?

Would it make

a difference?

Would it make

the base

unreliable?

Yes No

No

The more important

the item, the finer the

materiality screen

The more sensitive

the base, the finer the

materiality screen

Representation

faithfulness

Completeness

Figure 9: Relationships between Materiality, Relevance, Completeness,

and Reliability in FASB (1985), CON 2.

24 Materiality in Financial Reporting

54.

absence of aspecific IFRS dealing with a transaction, IASB, 2014,

IAS 8 requires, inter alia, completeness of information in all mate-

rial respects (IASB, 2014, IAS 8, para. 10). Figure 10 illustrates

these relationships, completing the picture as shown in Figures 5

and 8.

The Integrated Reporting Framework requires the inclusion of

all material information and the consideration of the level of speci-

ficity or preciseness of information (The International Integrated

Reporting Council, 2013, paras. 3.47 3.48).

The Global Reporting Initiative (GRI) has a Principle of

Completeness, intended to make sure that a sustainability report

covers material “Aspects” and their “Boundaries” under the dimen-

sions of scope (the range of Aspects covered), boundary (within or

outside the organization), and time (for the reporting period of

occurrence for their short-term impact as well as the long-term

unavoidable or irreversible consequences). Completeness here

serves the coverage and prioritization of all material Aspects, mak-

ing sure that material information is not omitted (Global Reporting

Initiative, 2013b, pp. 12 13).

1.j. Materiality versus Understandability

Although the common Conceptual Framework does not make a

direct link between these two concepts, at least three connections

can be drawn.

Relevance? Reliability?

Completeness?

-Size

-Circumstances

Nature

Freedom from material

error and bias

Materiality?

Omission

Figure 10: Relationships between Materiality, Relevance, Completeness,