Downloaded 37 times

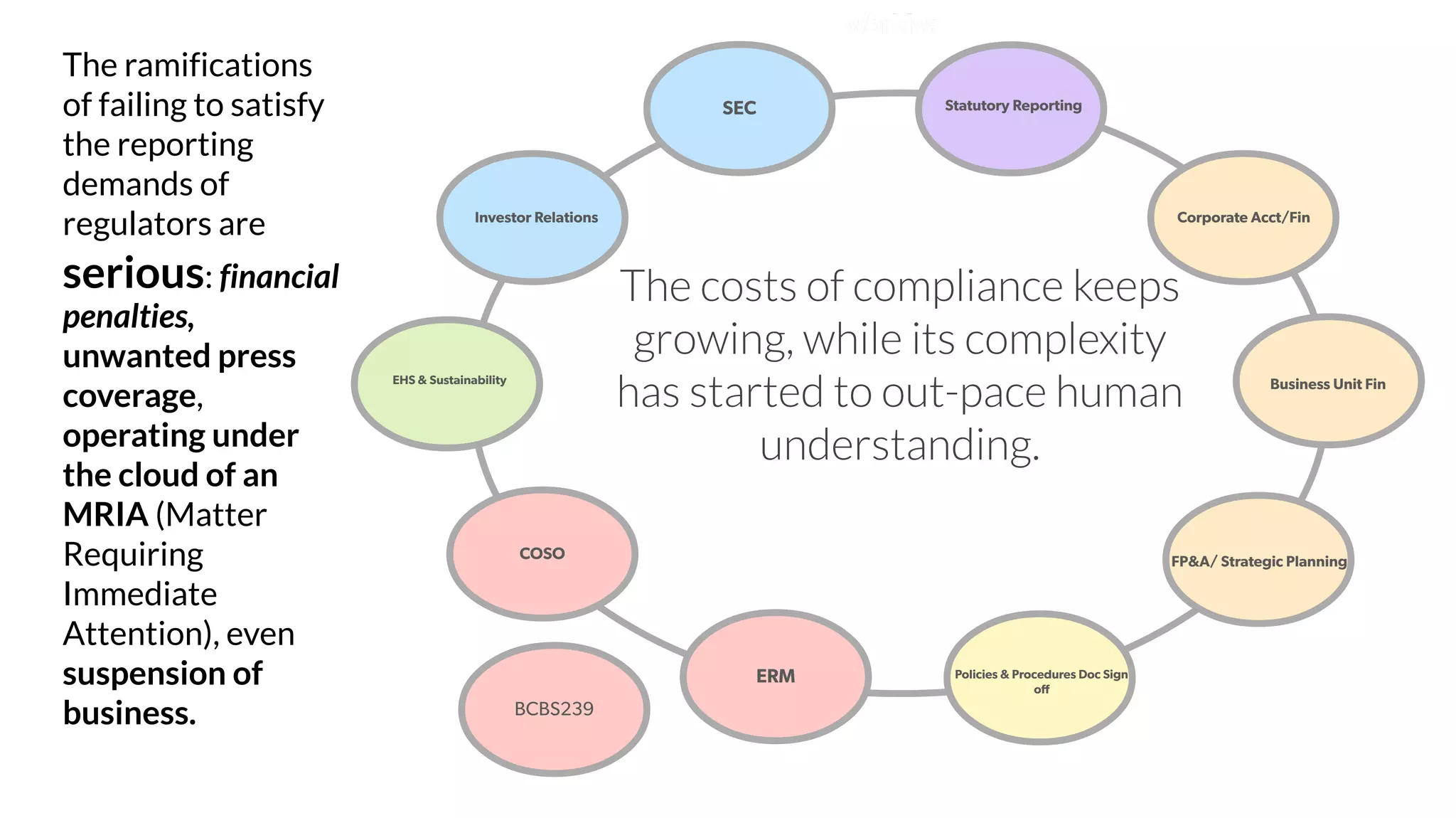

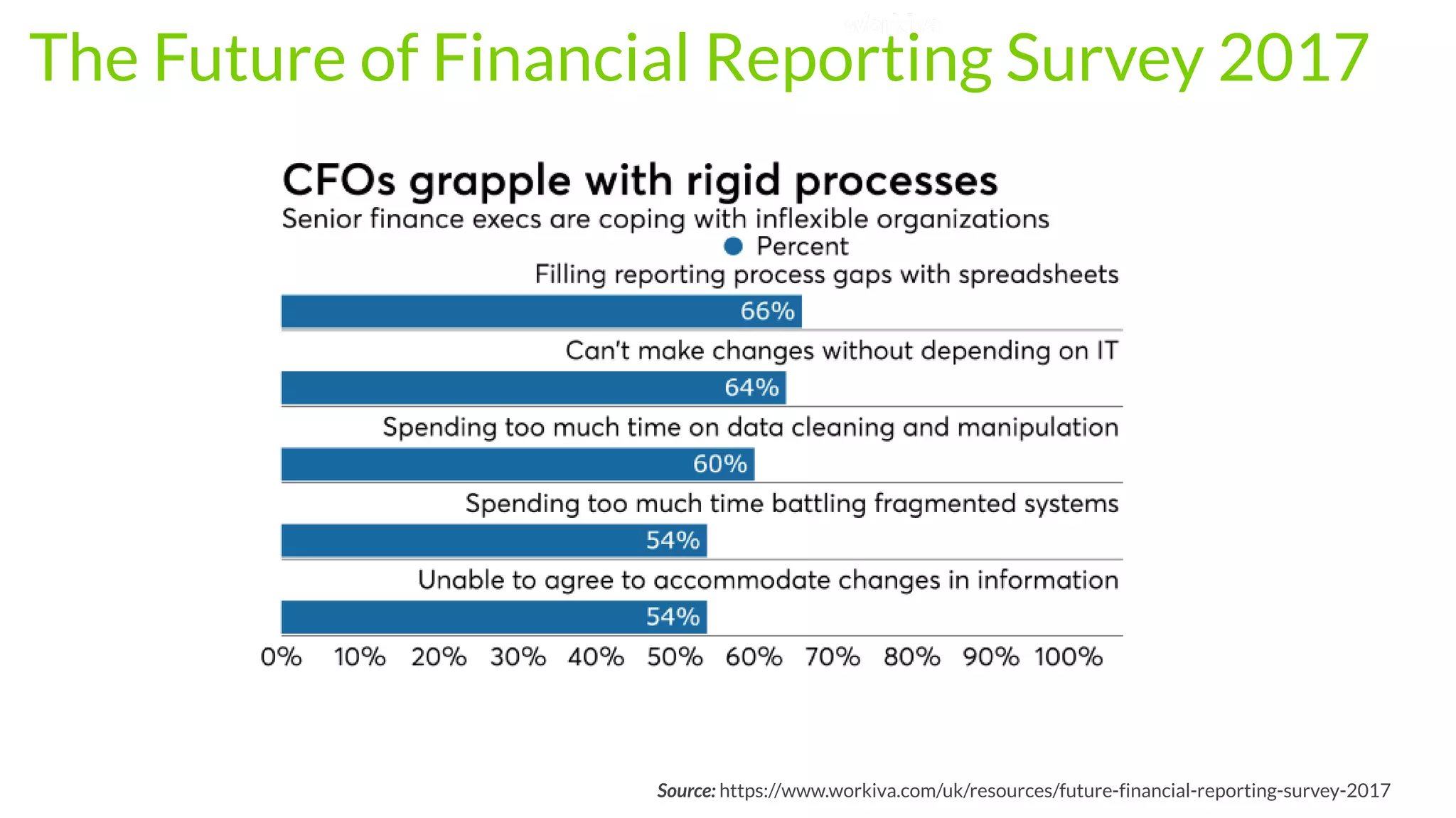

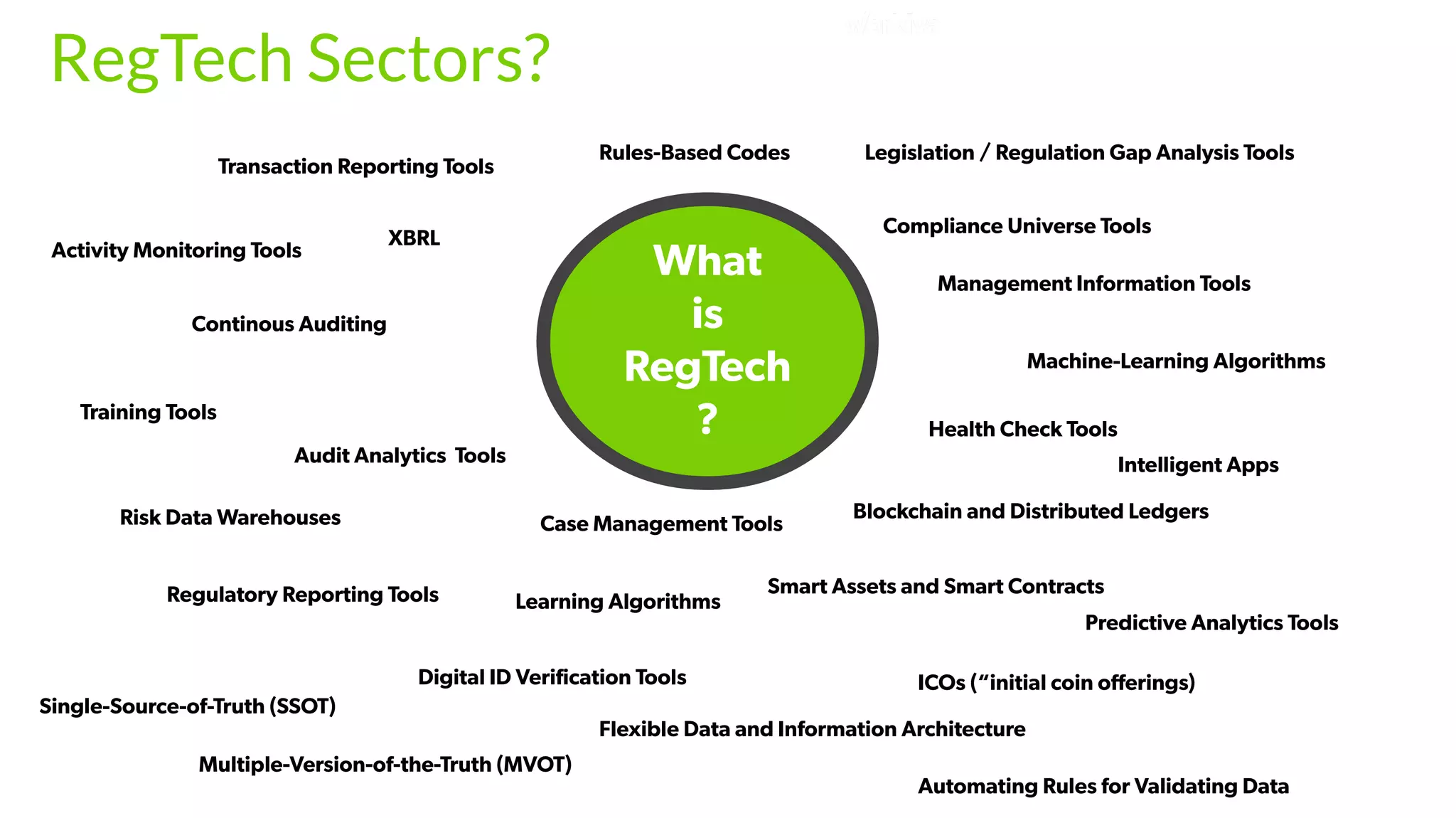

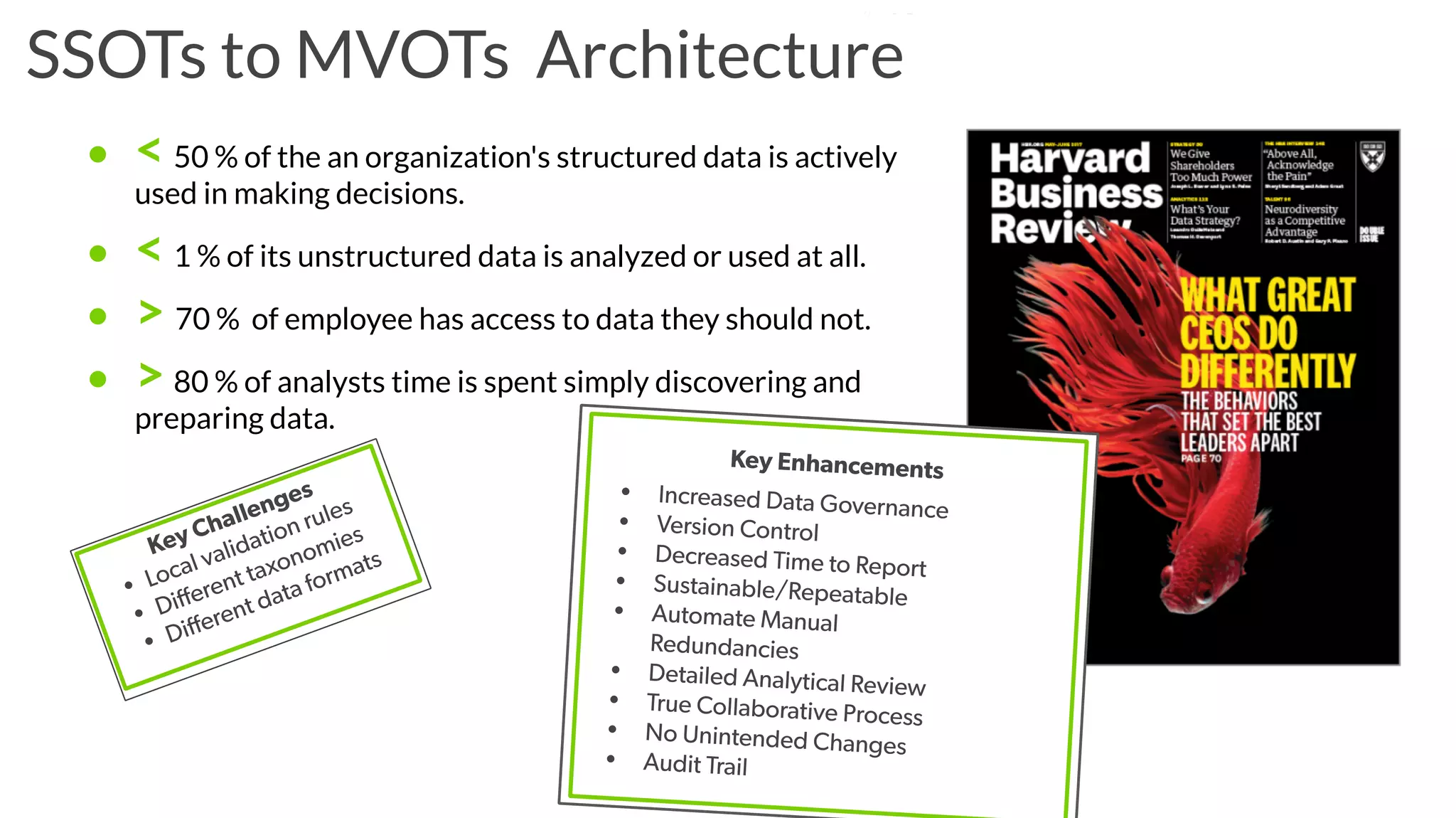

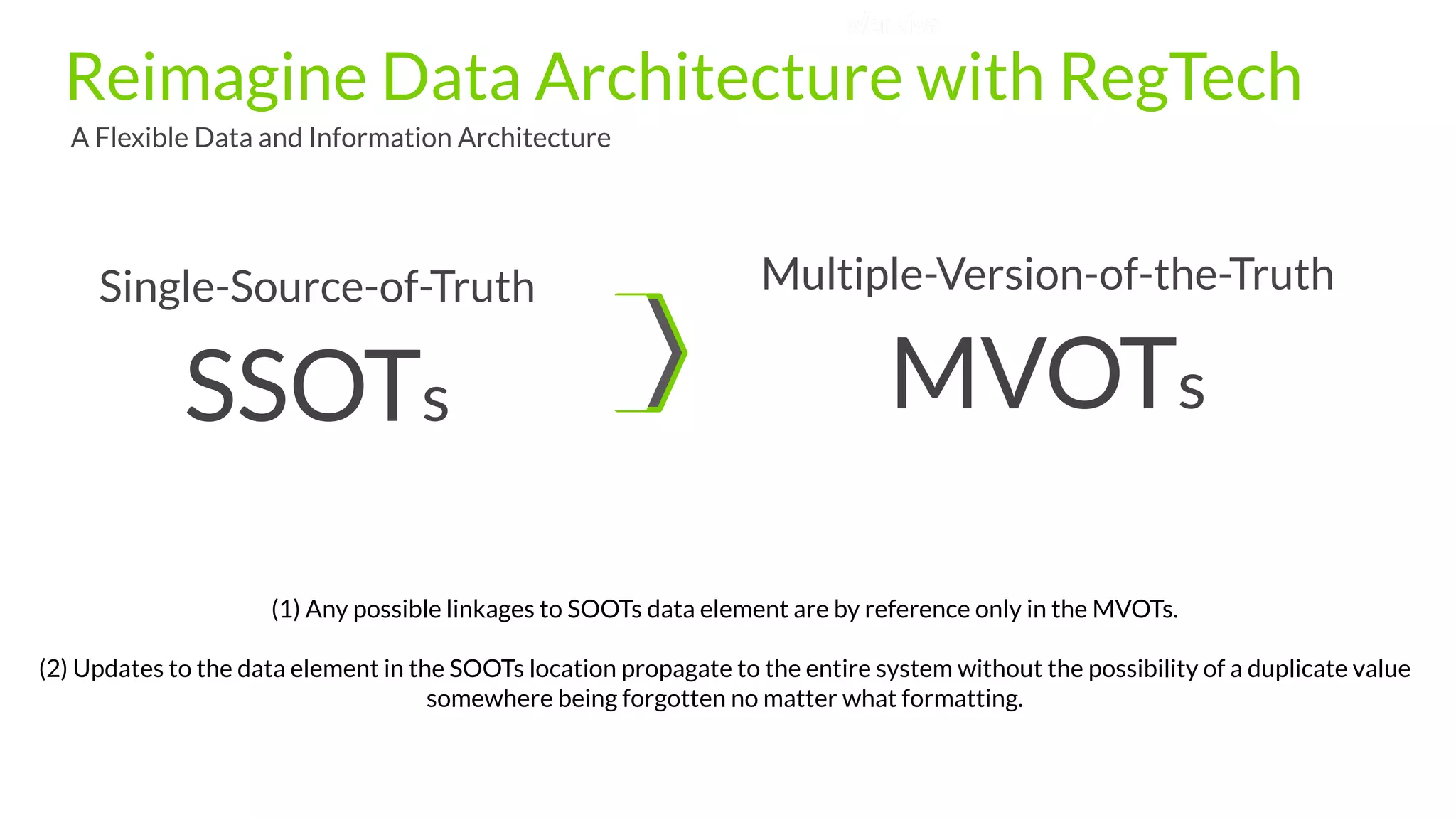

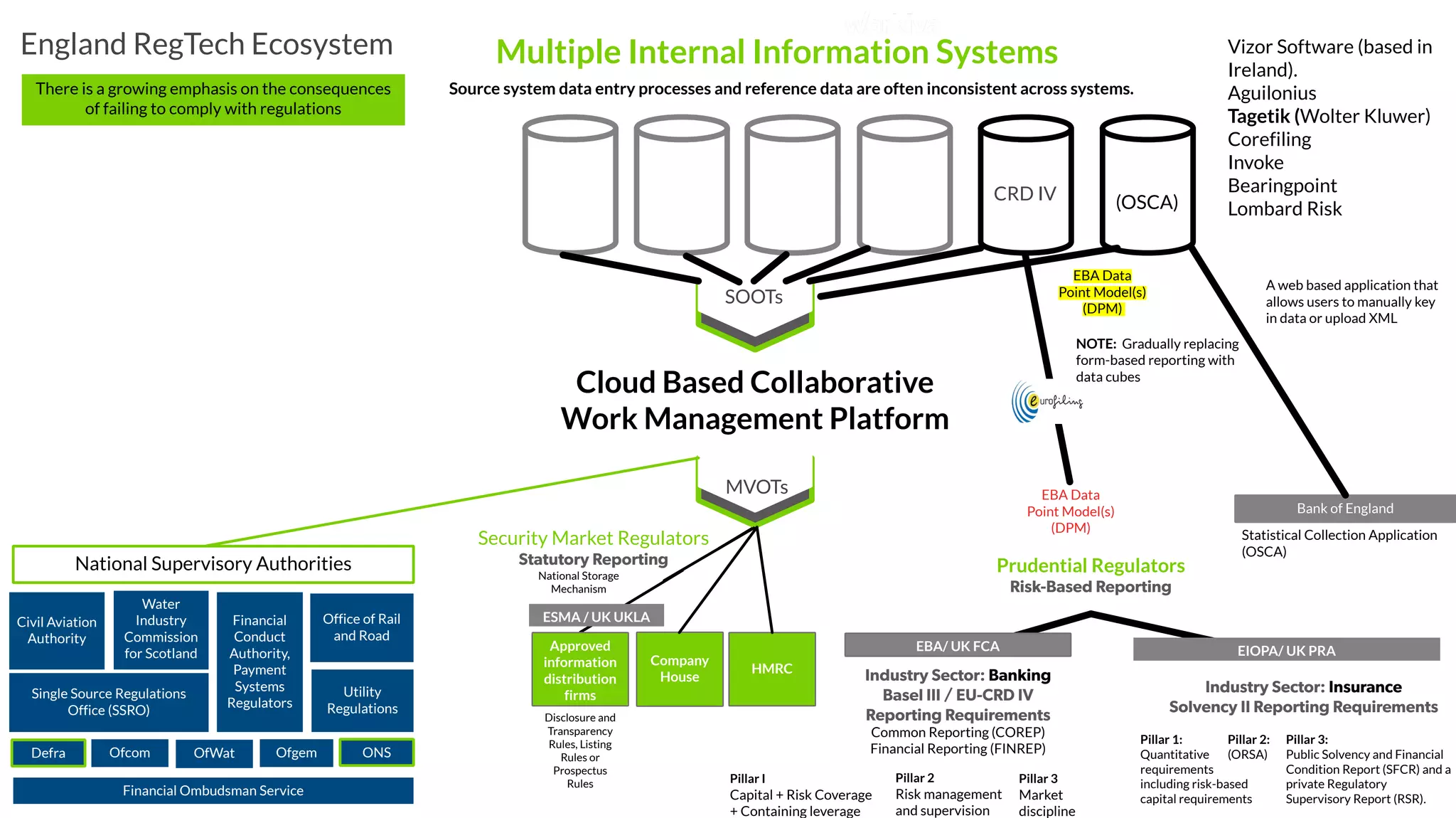

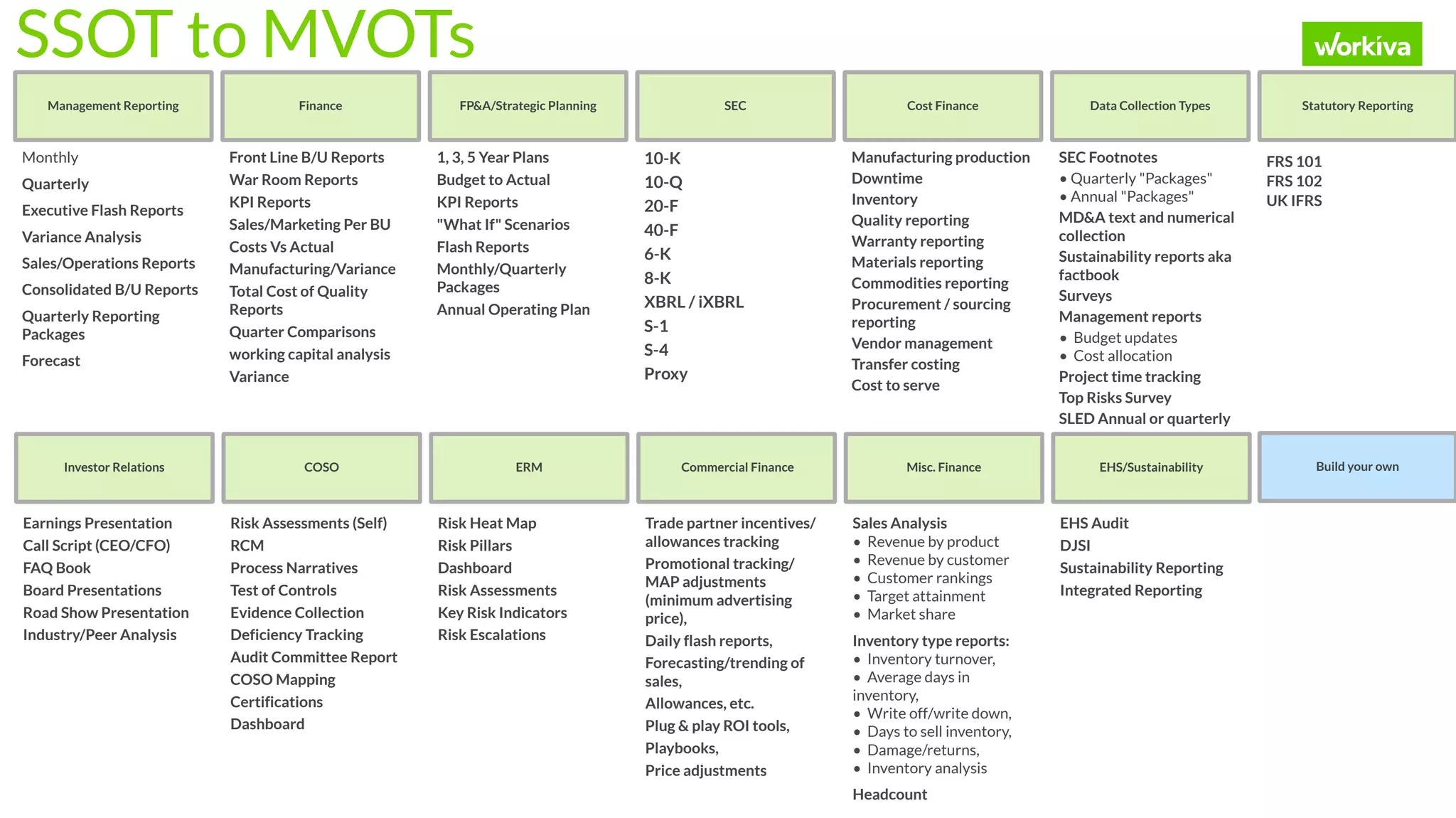

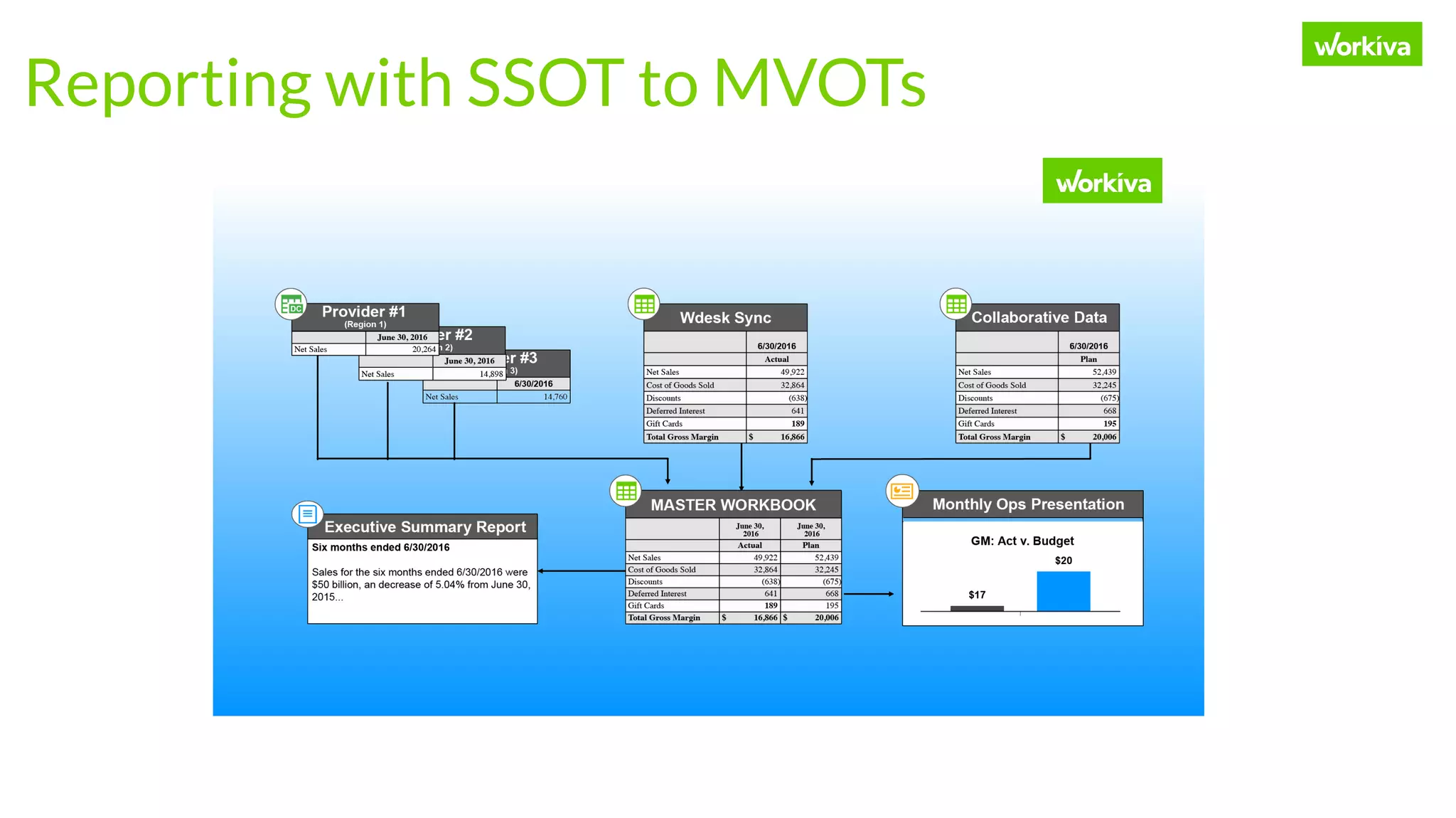

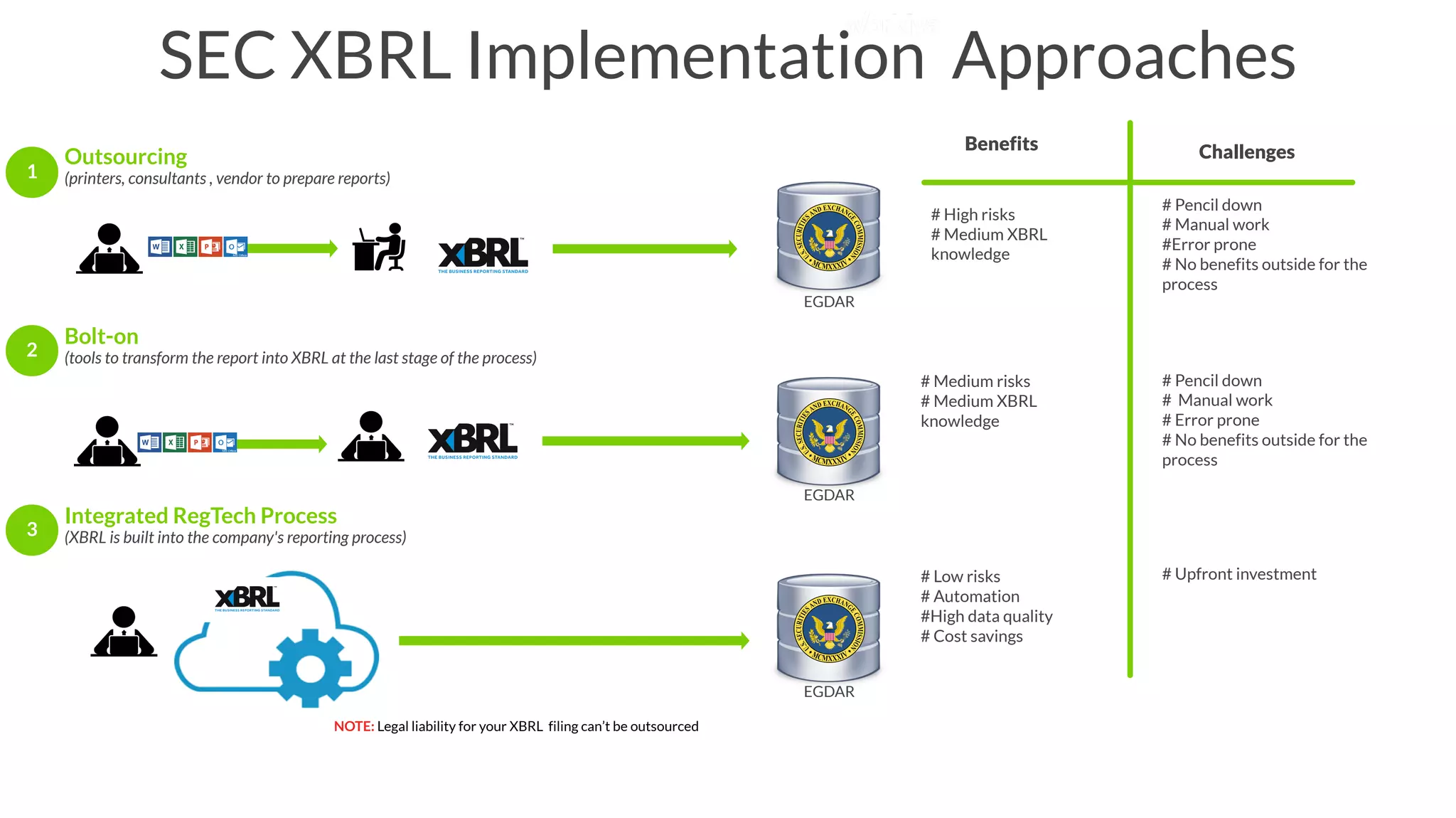

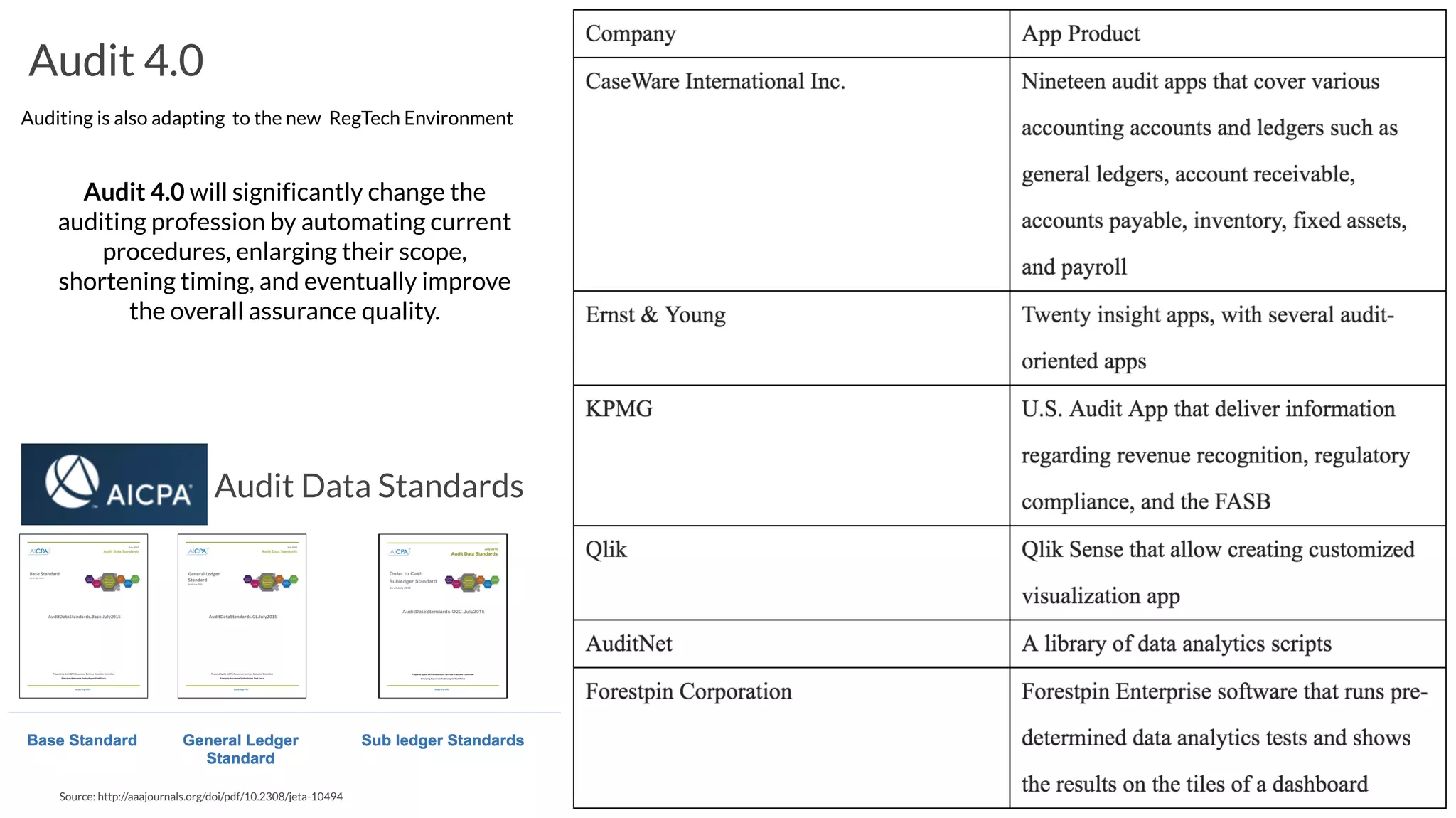

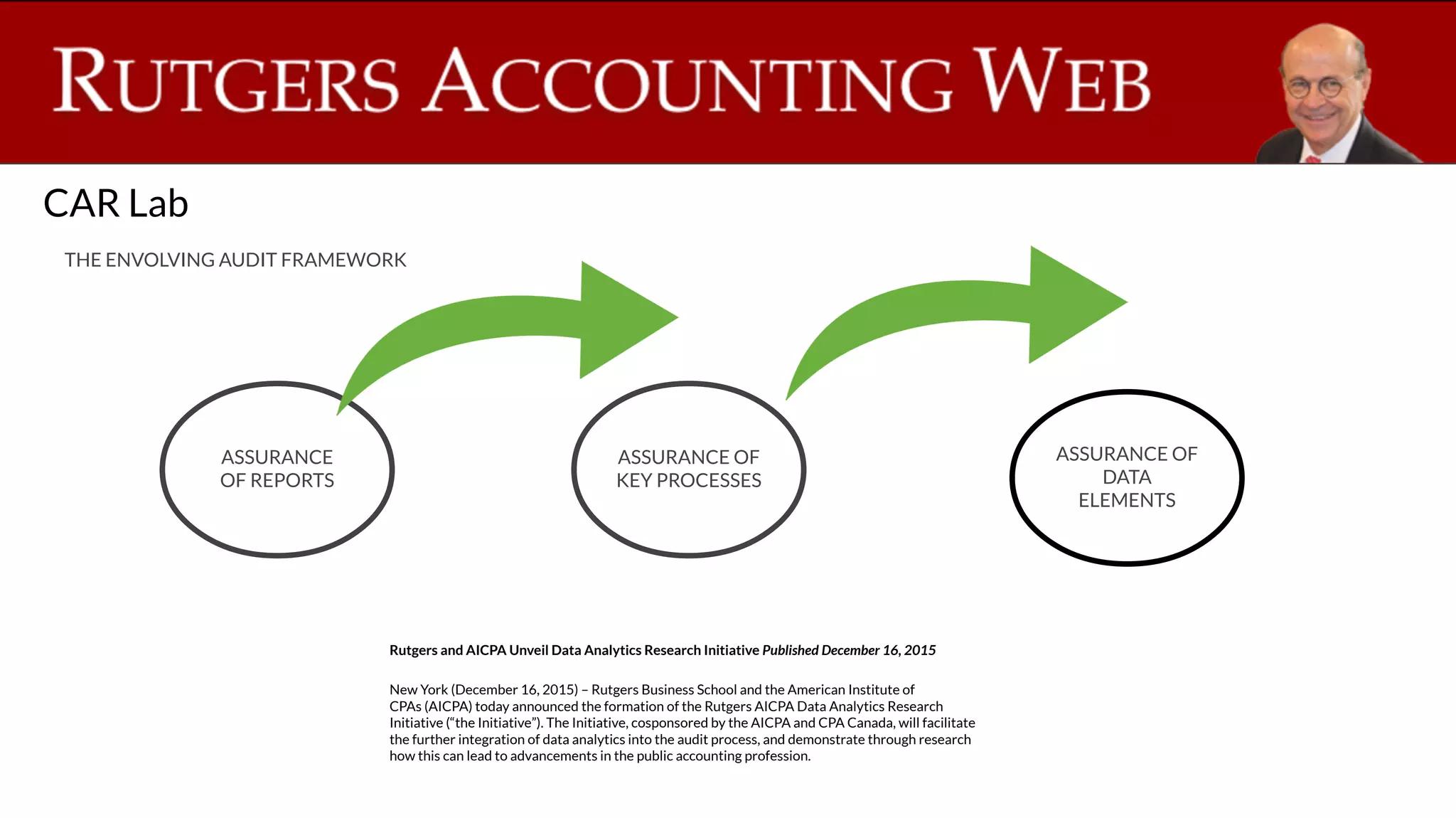

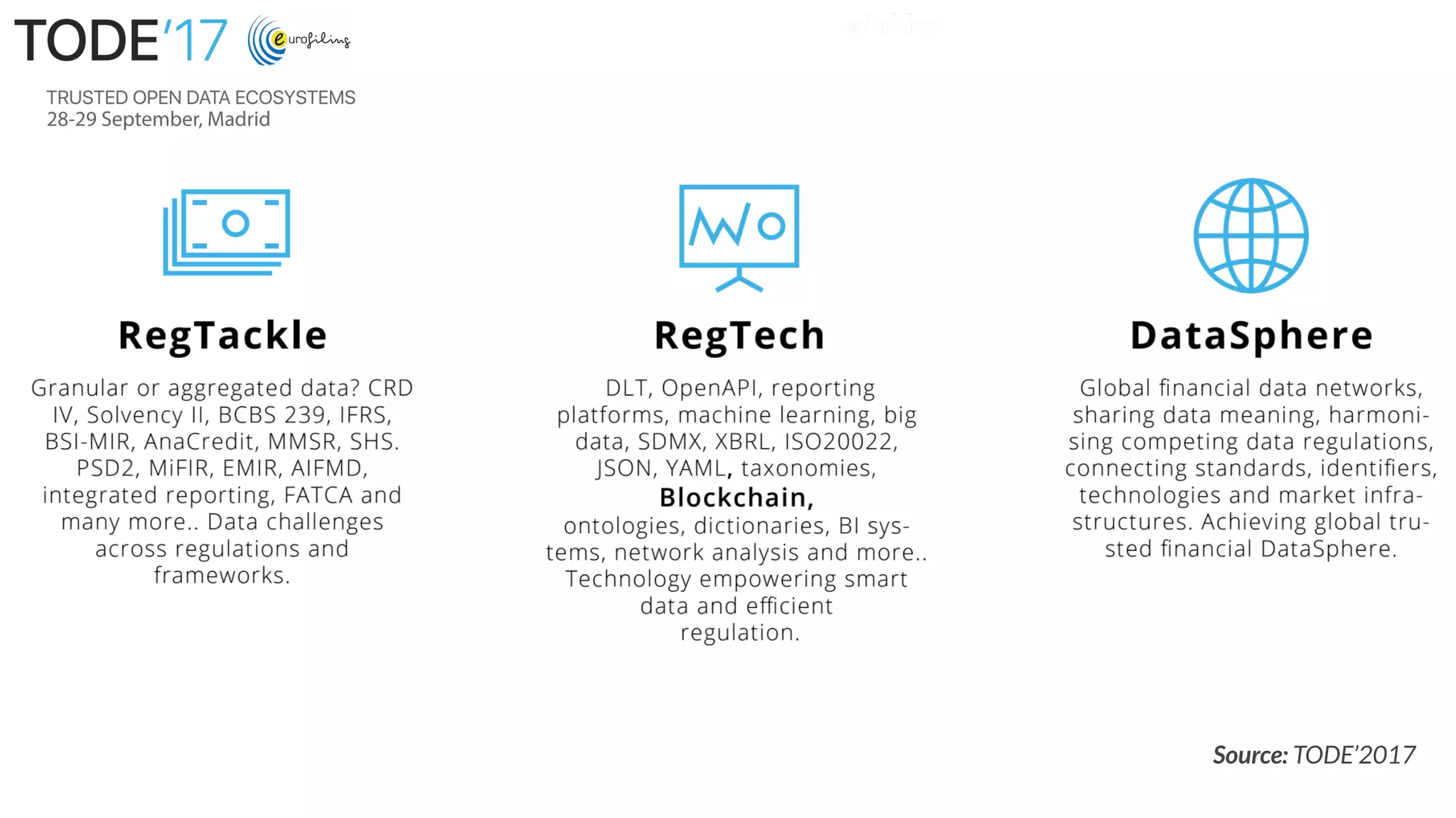

Liv Watson from Workiva presented on regulatory technology (RegTech) and how it can help organizations more efficiently and effectively meet growing regulatory reporting demands. Some key points included: - Regulatory requirements have increased in complexity and volume, outpacing human capabilities without technology. RegTech aims to address this through automation. - RegTech tools and strategies span areas like compliance management, regulatory reporting, risk management, and "smart audits". Emerging areas include blockchain, data standards like XBRL, and predictive analytics. - Adopting a flexible data architecture with single-source and multiple-version data models can help organizations better leverage RegTech across functions like finance, risk, and ESG reporting.