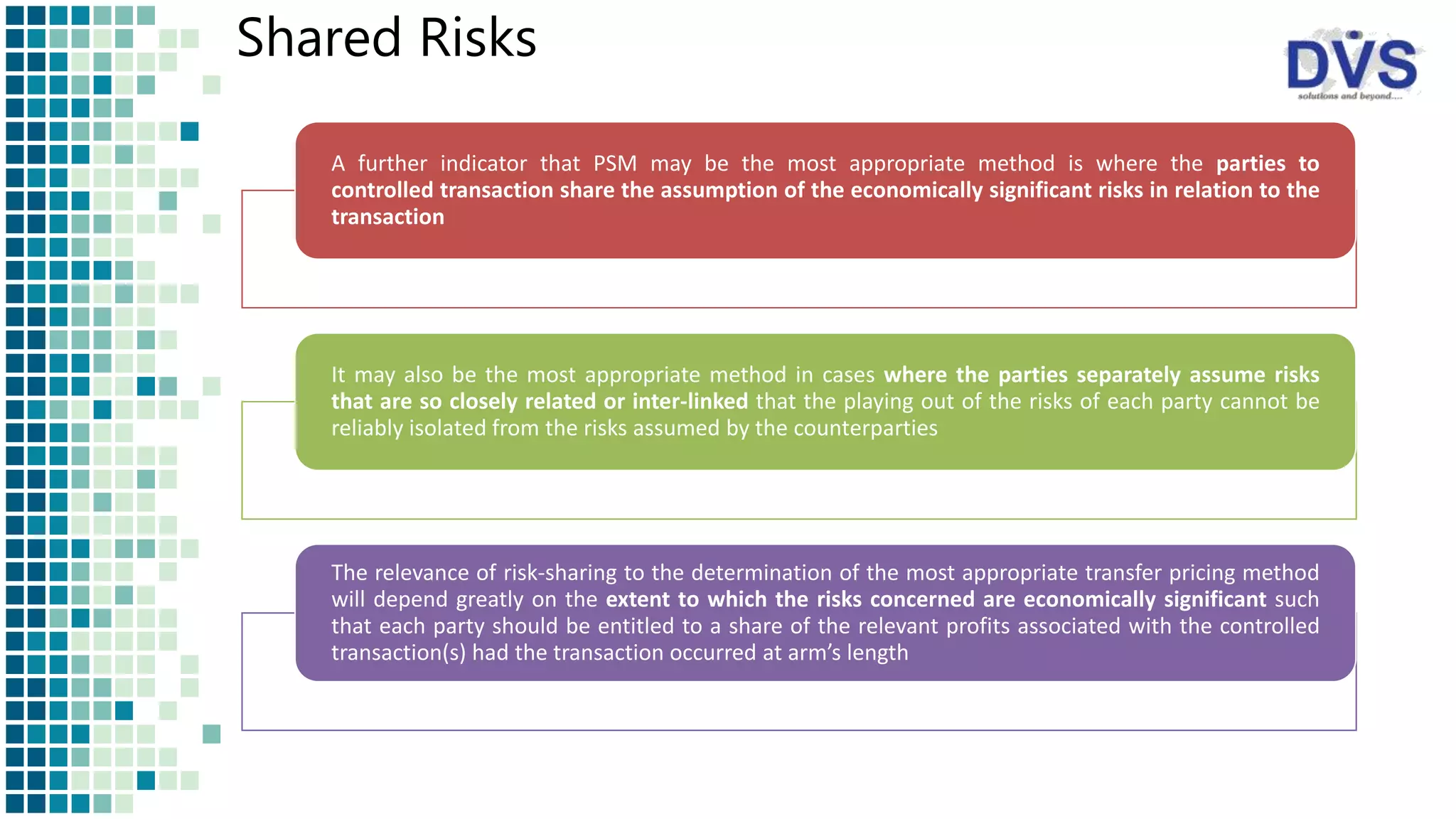

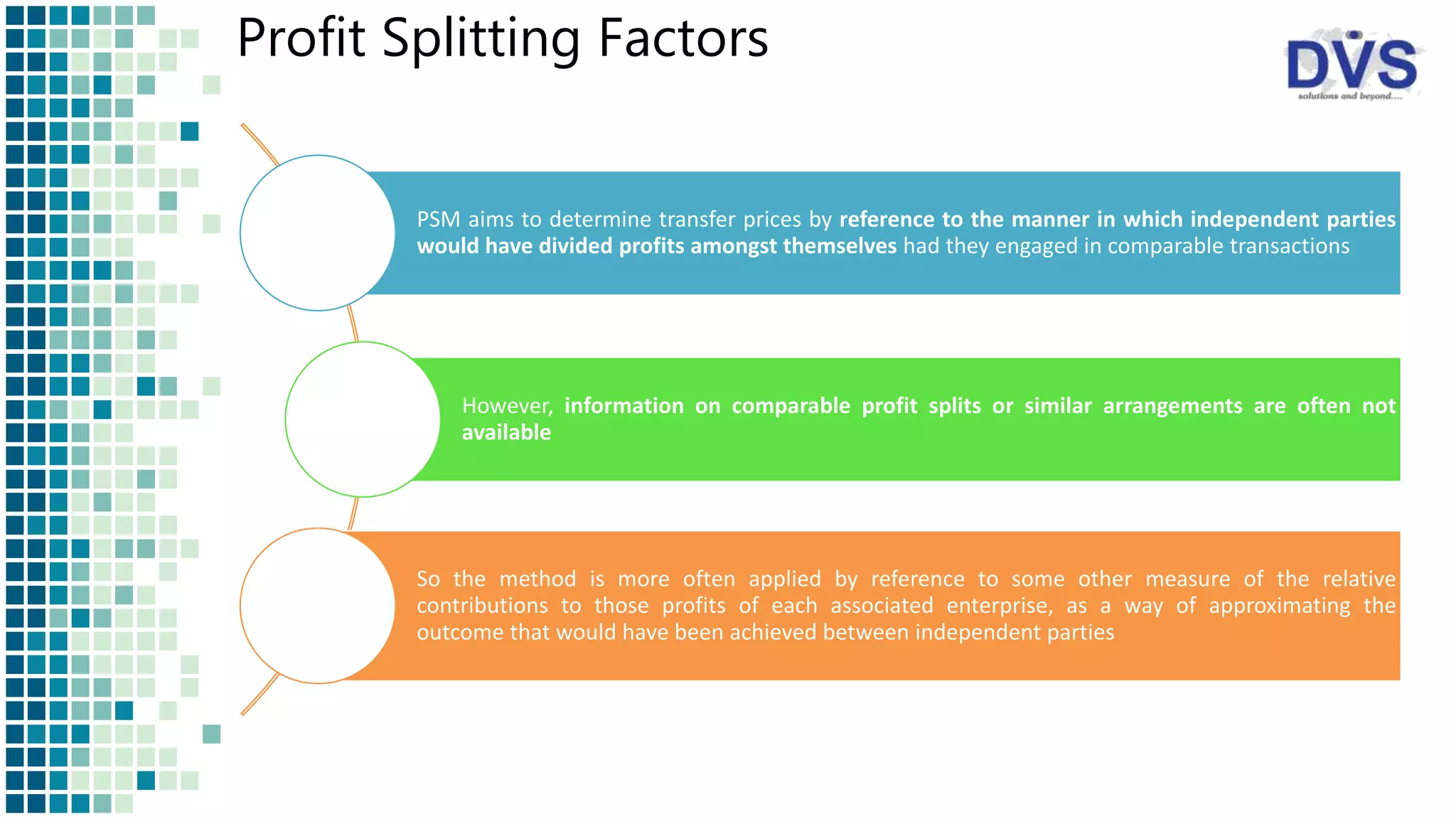

The Profit Split Method (PSM) is a complex transfer pricing approach that divides combined profits of related parties based on their contributions, applicable in transactions involving unique contributions or high integration of operations. While PSM offers a comprehensive evaluation aiming for arm's length pricing outcomes, its complexity arises from difficulties in measuring relevant profits and the need for detailed data. PSM is particularly useful in industries with significant intangible assets, like high technology and pharmaceuticals, where alternative pricing methods may not suffice.

![AUTOMATIC VACATION OF STAY GRANTED BY TRIBUNALDCIT v. PEPSI FOODS LTD. [2021]...](https://cdn.slidesharecdn.com/ss_thumbnails/depcitvpepsifoodsco-210717130643-thumbnail.jpg?width=640&height=640&fit=bounds)