Download to read offline

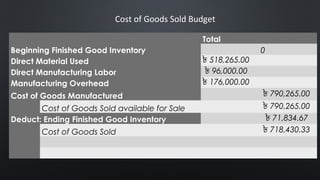

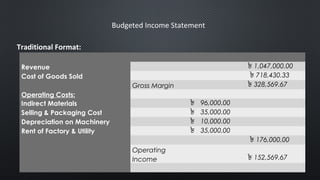

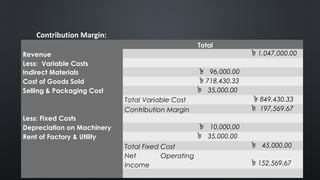

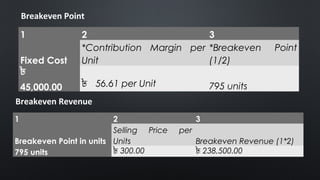

This document summarizes the costing and budgeting for sandal production. It includes analysis of direct material costs, direct labor costs, manufacturing overhead costs, and allocation of overhead. Budgets are presented for production, direct materials, direct labor, cost of goods sold, income statement, contribution margin, break-even point, margin of safety, and sensitivity analysis. The objective is to apply managerial accounting concepts to determine the full cost of each sandal and budget costs and profits.