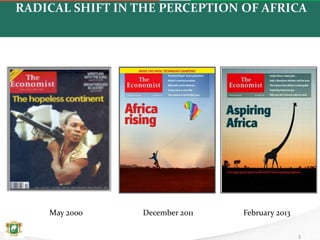

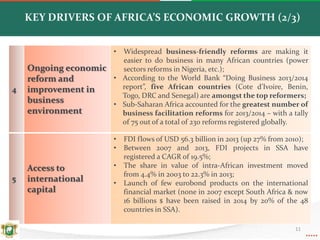

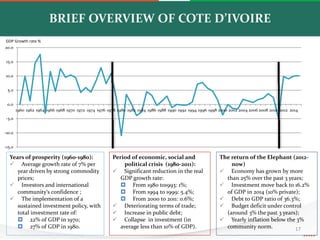

The document discusses the current economic environment and drivers of economic growth in Sub-Saharan Africa. It notes that perceptions of risk in Africa have shifted positively in recent years. Strong economic growth across the region over the past decade has been fueled by increasing political stability, strategic development planning, regional integration efforts, and infrastructure investment. Côte d'Ivoire in particular is highlighted as pursuing business-friendly reforms and allocating a large portion of its budget to investments and poverty reduction initiatives to promote continued economic and social development.