Download as PDF, PPTX

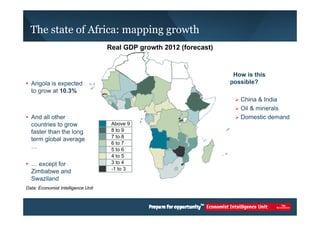

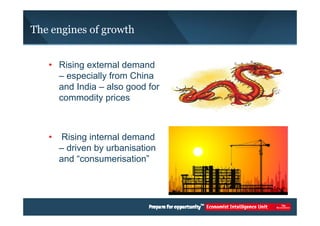

This document summarizes an Economist Intelligence Unit presentation on business opportunities and challenges in Africa. It finds that Africa is experiencing strong GDP growth, driven by rising external demand from China and India and increasing internal demand. However, the business climate remains challenging due to difficulties setting up businesses, skill shortages, complex tax systems, and weak infrastructure. While African economies are growing, regional integration efforts have faced issues and the continent still ranks poorly on measures of business environment.