Downloaded 35 times

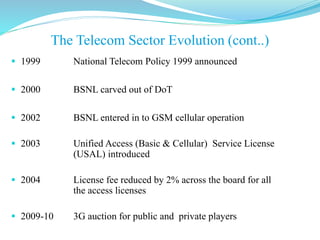

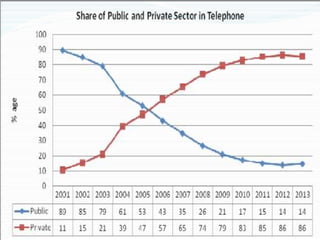

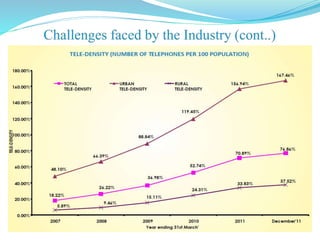

The Indian telecom sector has undergone significant changes since the 1970s. It started as a state-run monopoly but has since transitioned to a competitive private sector dominated market. Major reforms included allowing foreign investment, introducing private operators, and establishing an independent regulator. As a result, tele-density increased dramatically from 5% in 1999 to over 75% currently. However, intense price competition has led to declining revenues per user, posing financial challenges for operators in the saturated market. The oligopolistic industry is projected to consolidate further with only a few large players dominating in the coming years.

![Exercicios complementares -_matematica_-7o ano_3a_[1]](https://cdn.slidesharecdn.com/ss_thumbnails/exercicioscomplementares-matematica-7oano3a1-161107190245-thumbnail.jpg?width=640&height=640&fit=bounds)