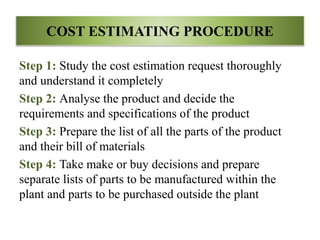

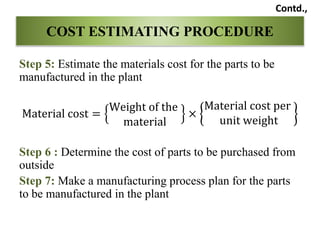

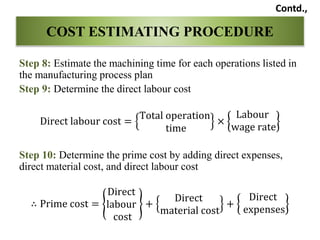

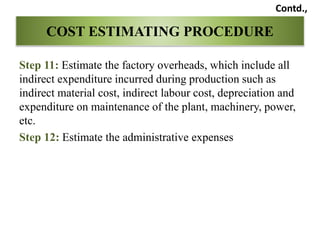

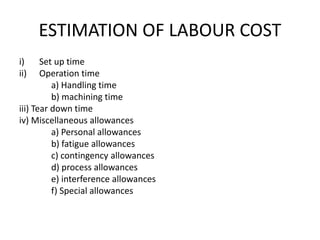

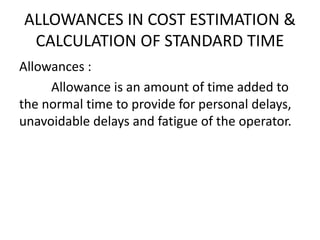

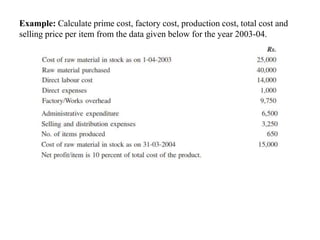

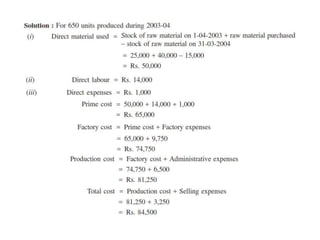

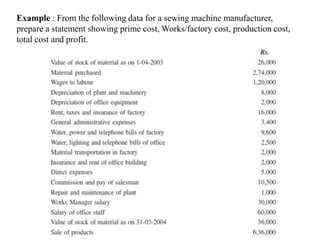

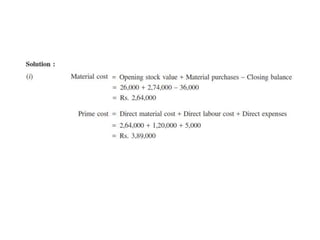

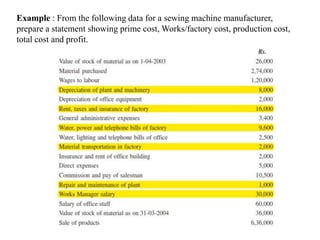

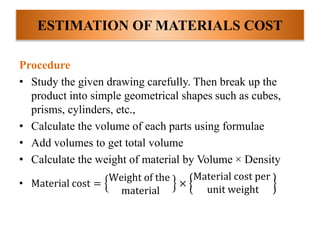

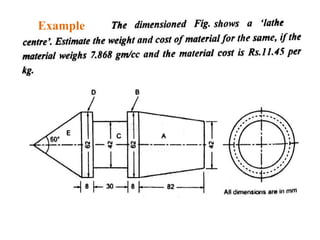

The document discusses cost estimation, which involves predicting the costs of producing a product before actual production. It covers methods of costing, types of estimates, estimating procedures, and components of a cost estimate such as material, labor, overhead costs. The objectives of estimating are to determine selling price and profitability. Detailed analysis and comparison to similar past products are common estimation methods.