Downloaded 118 times

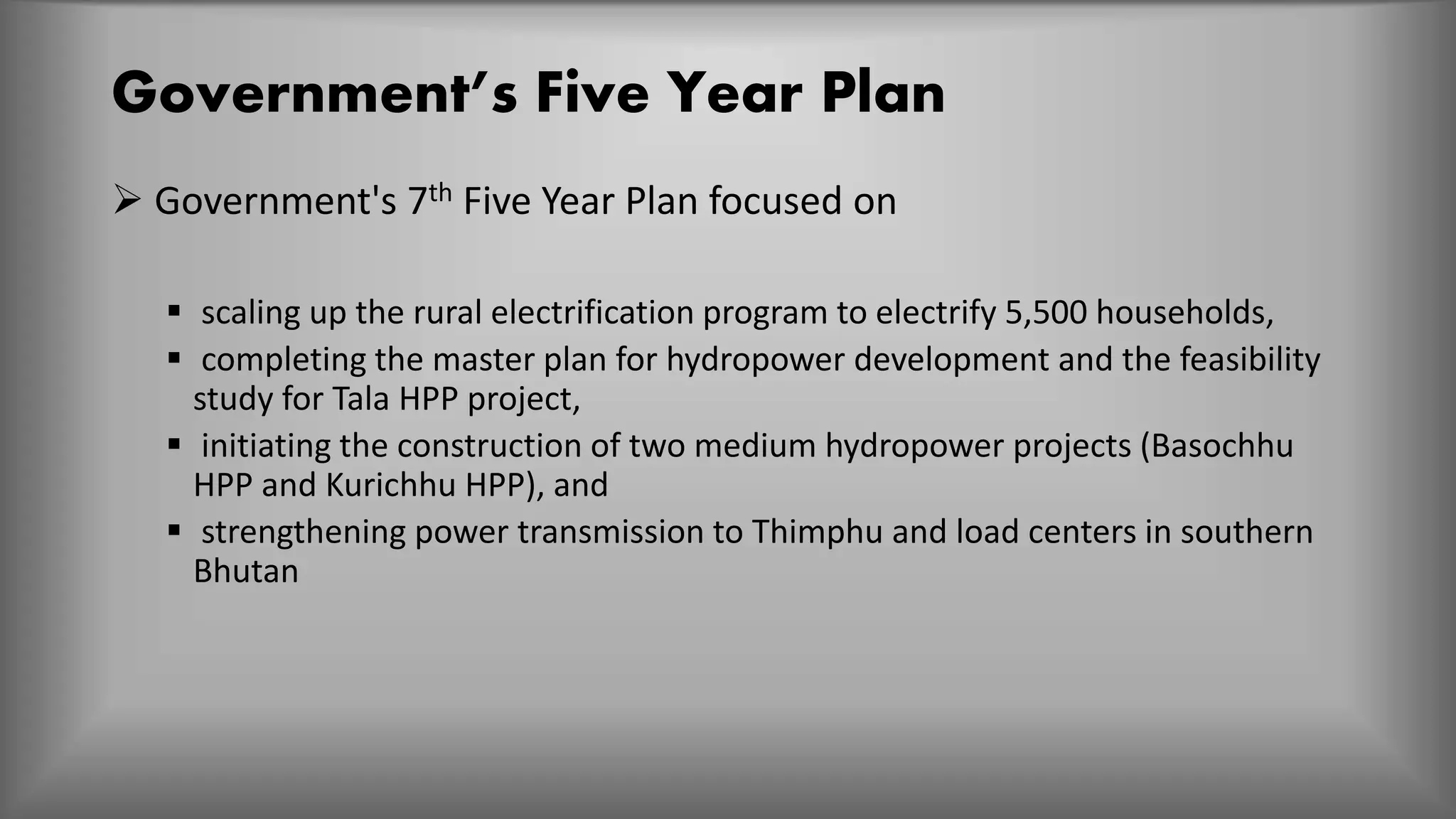

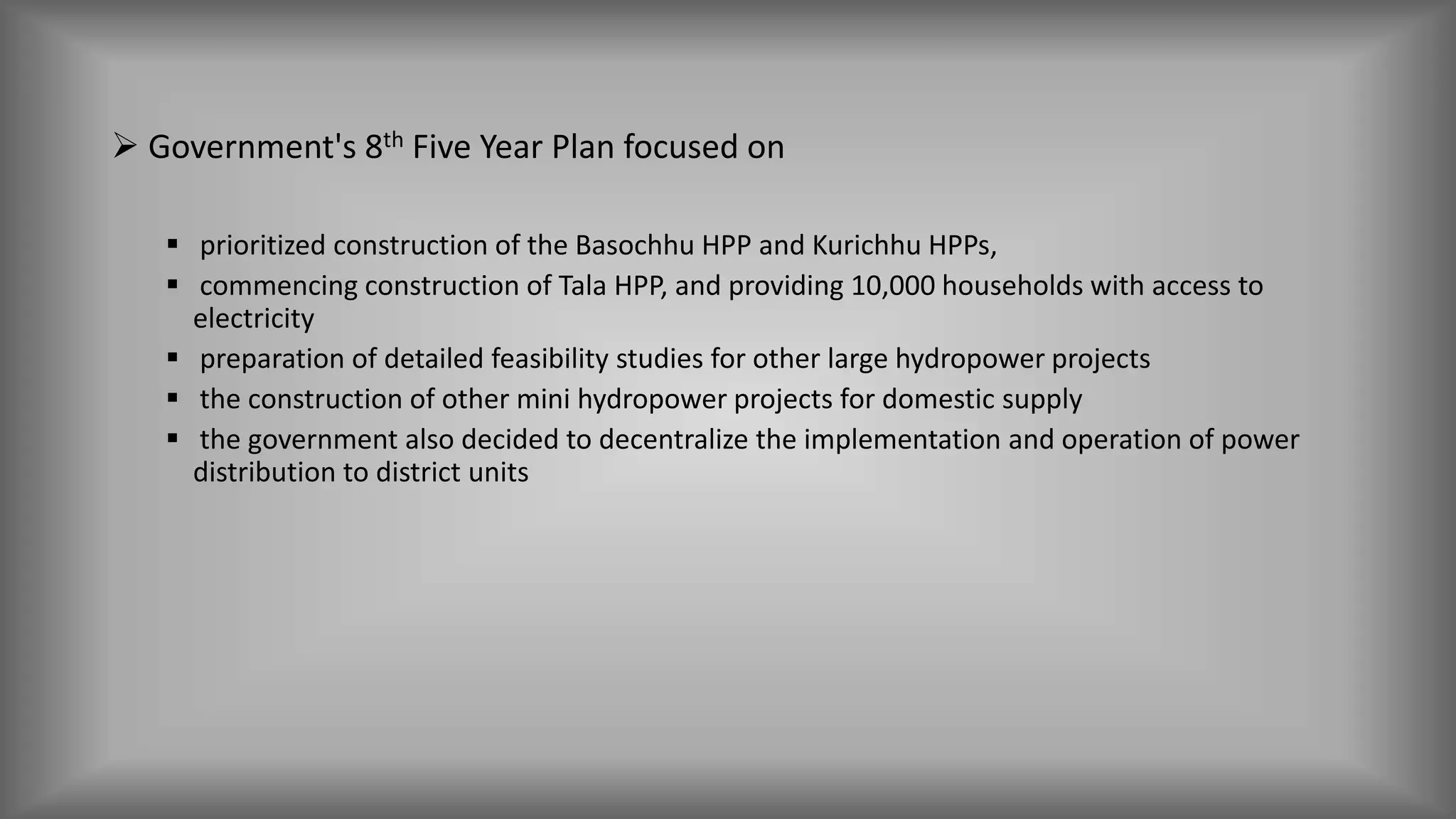

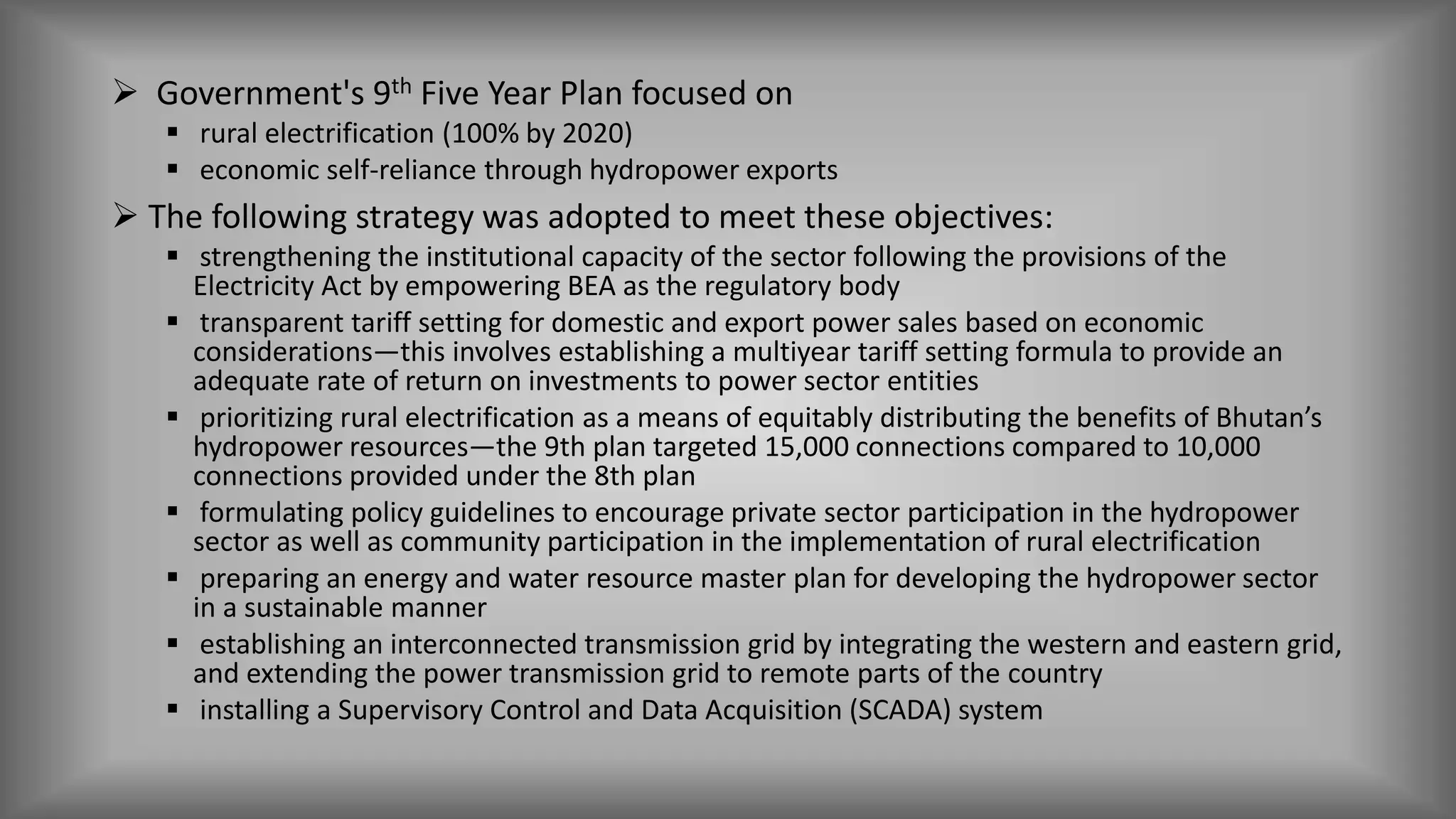

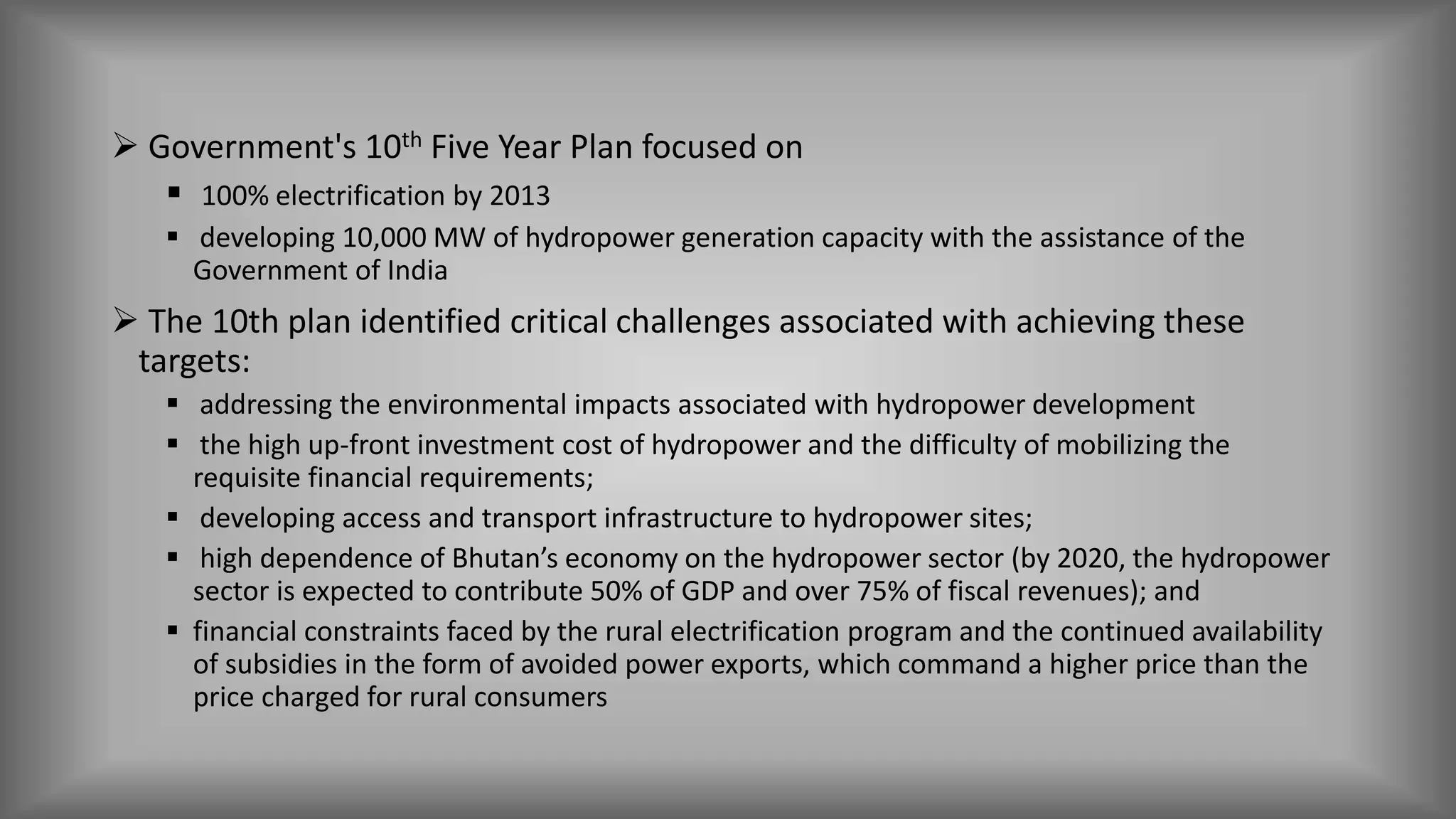

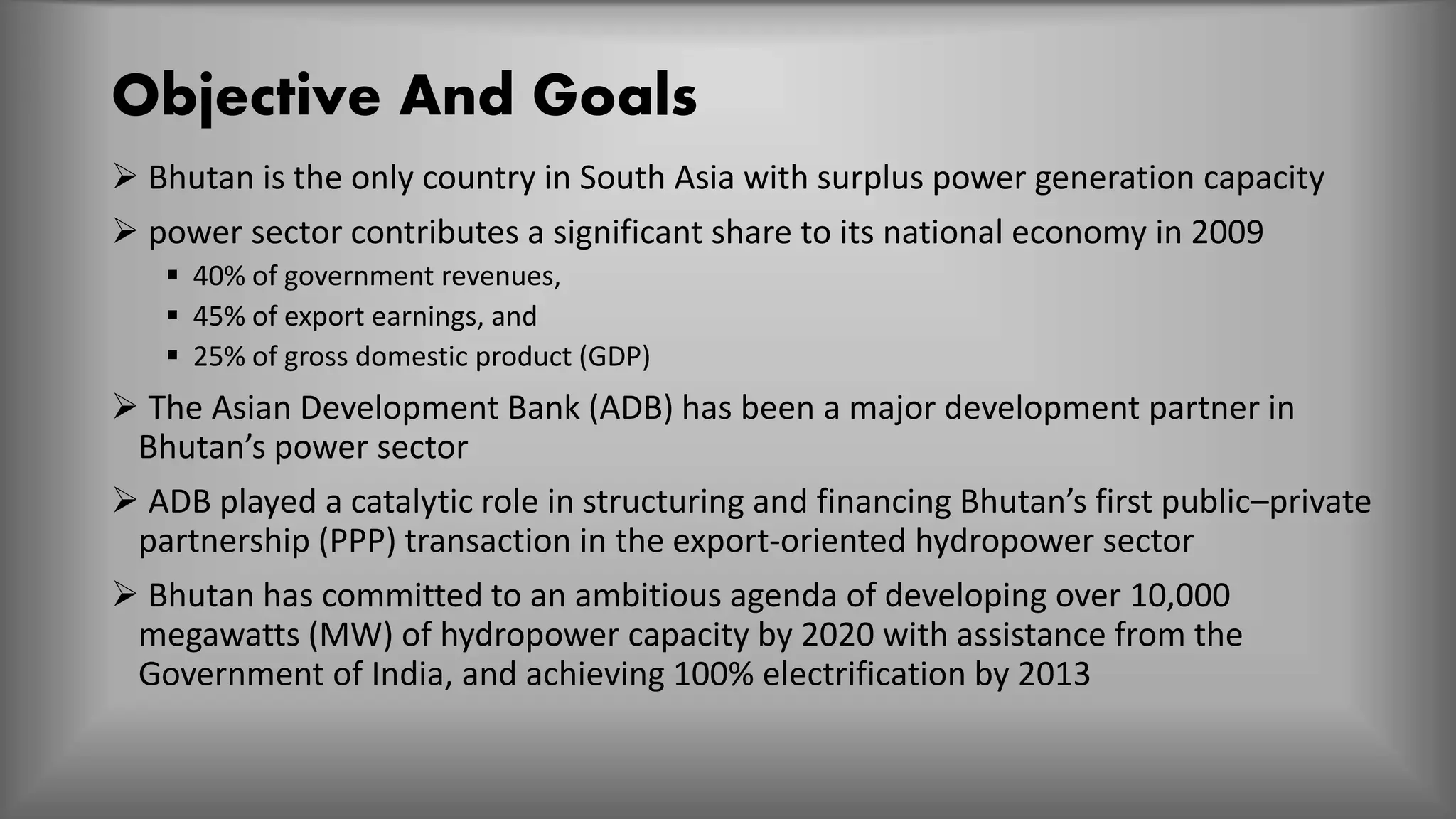

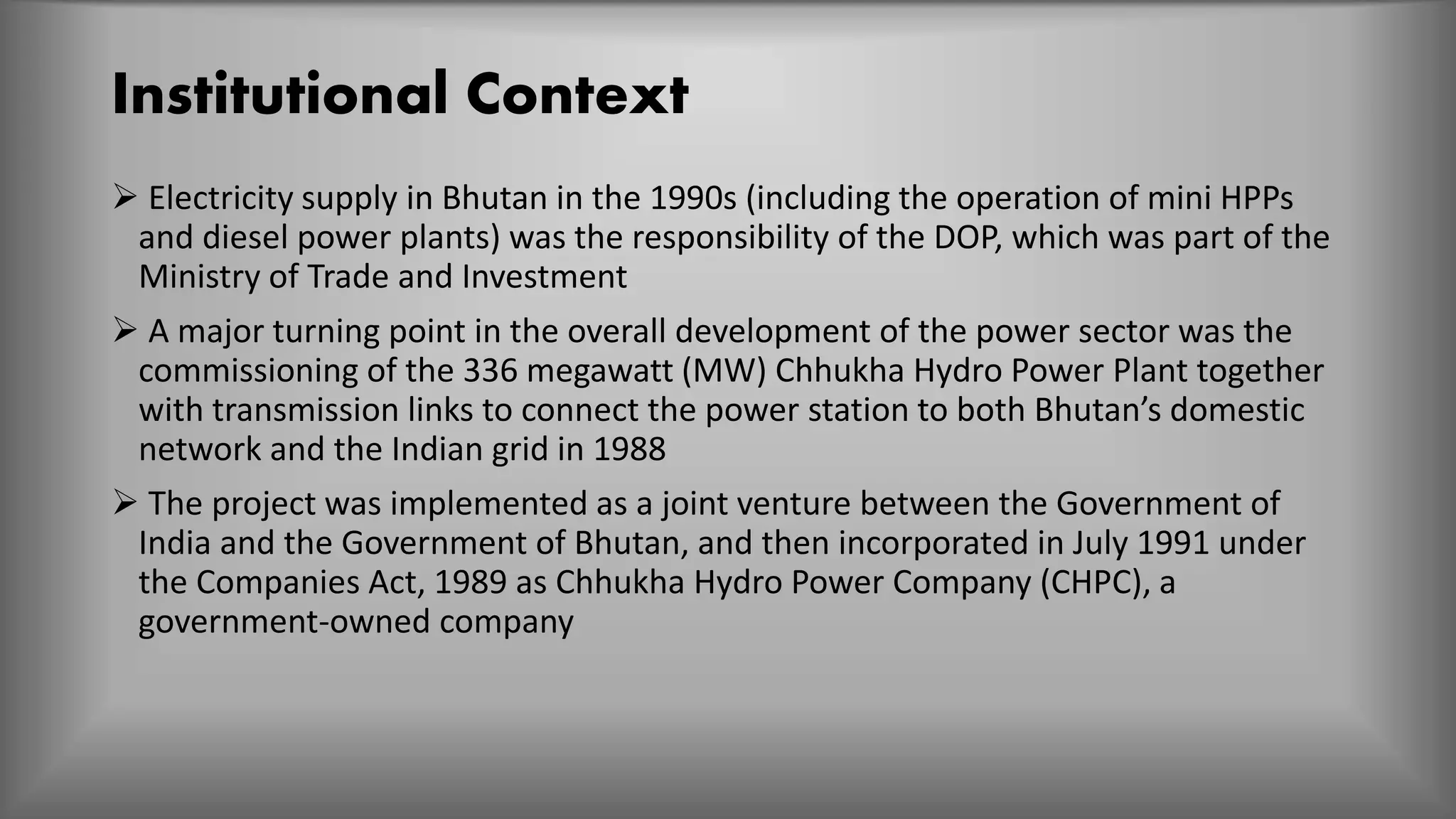

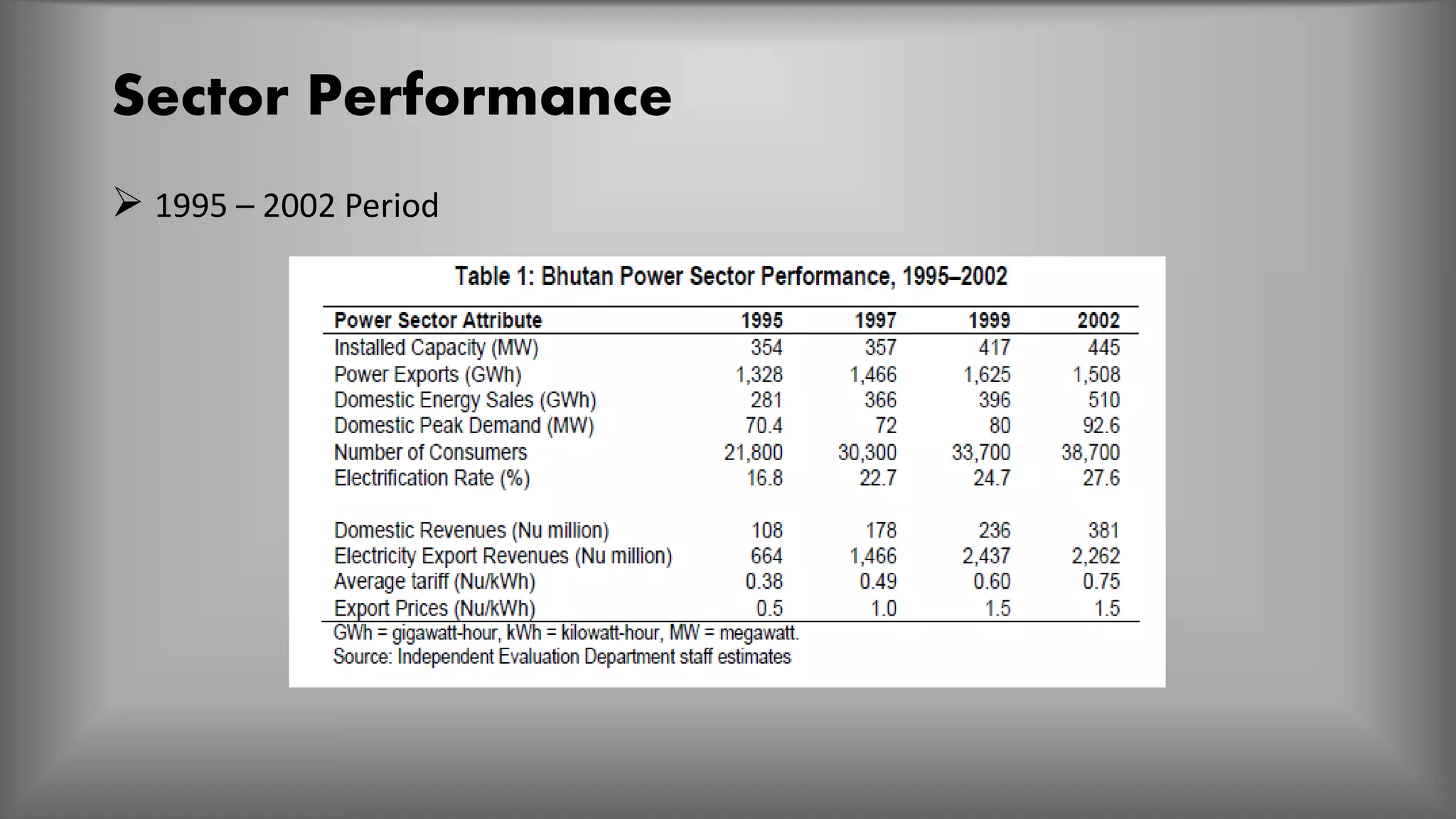

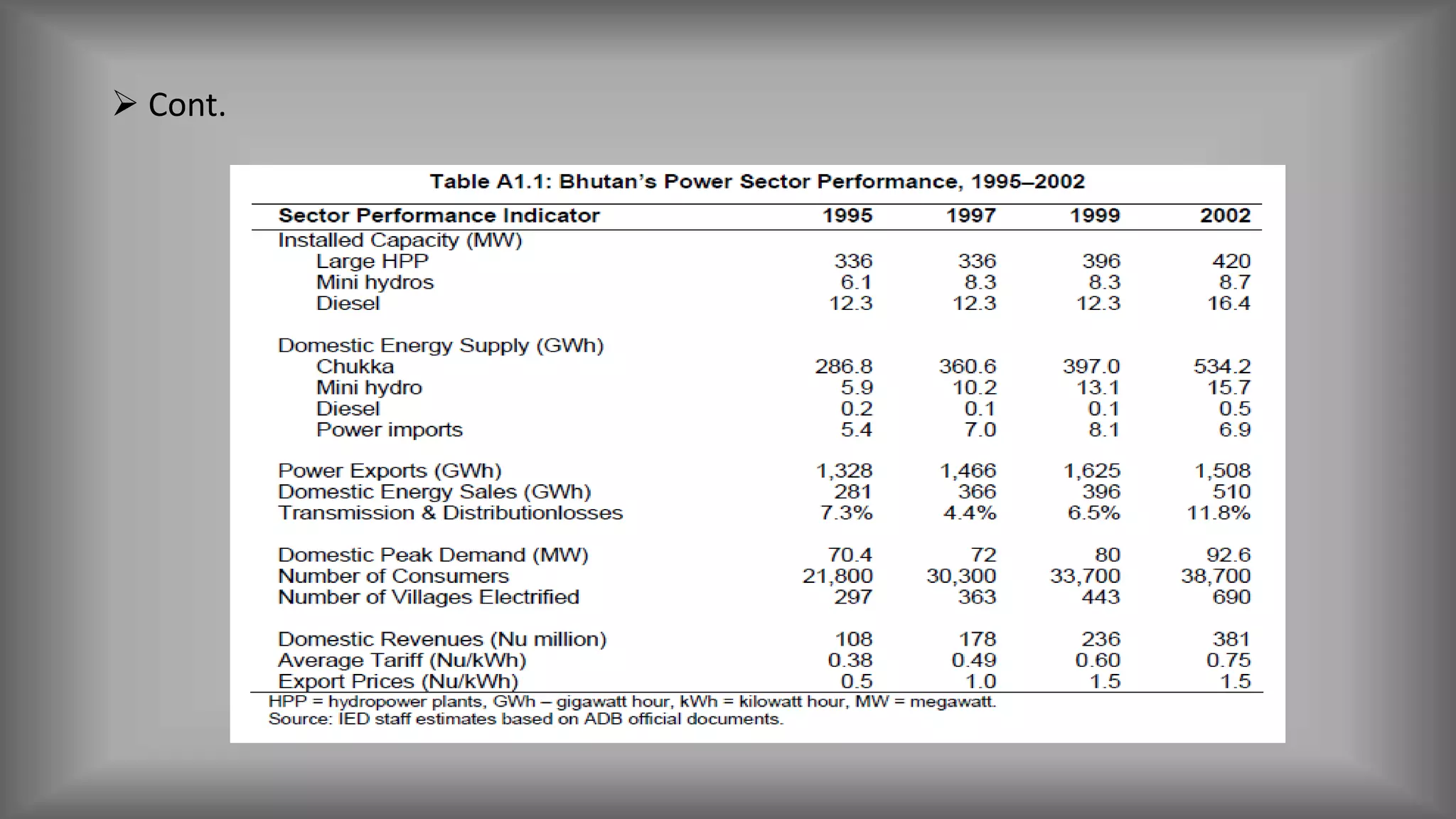

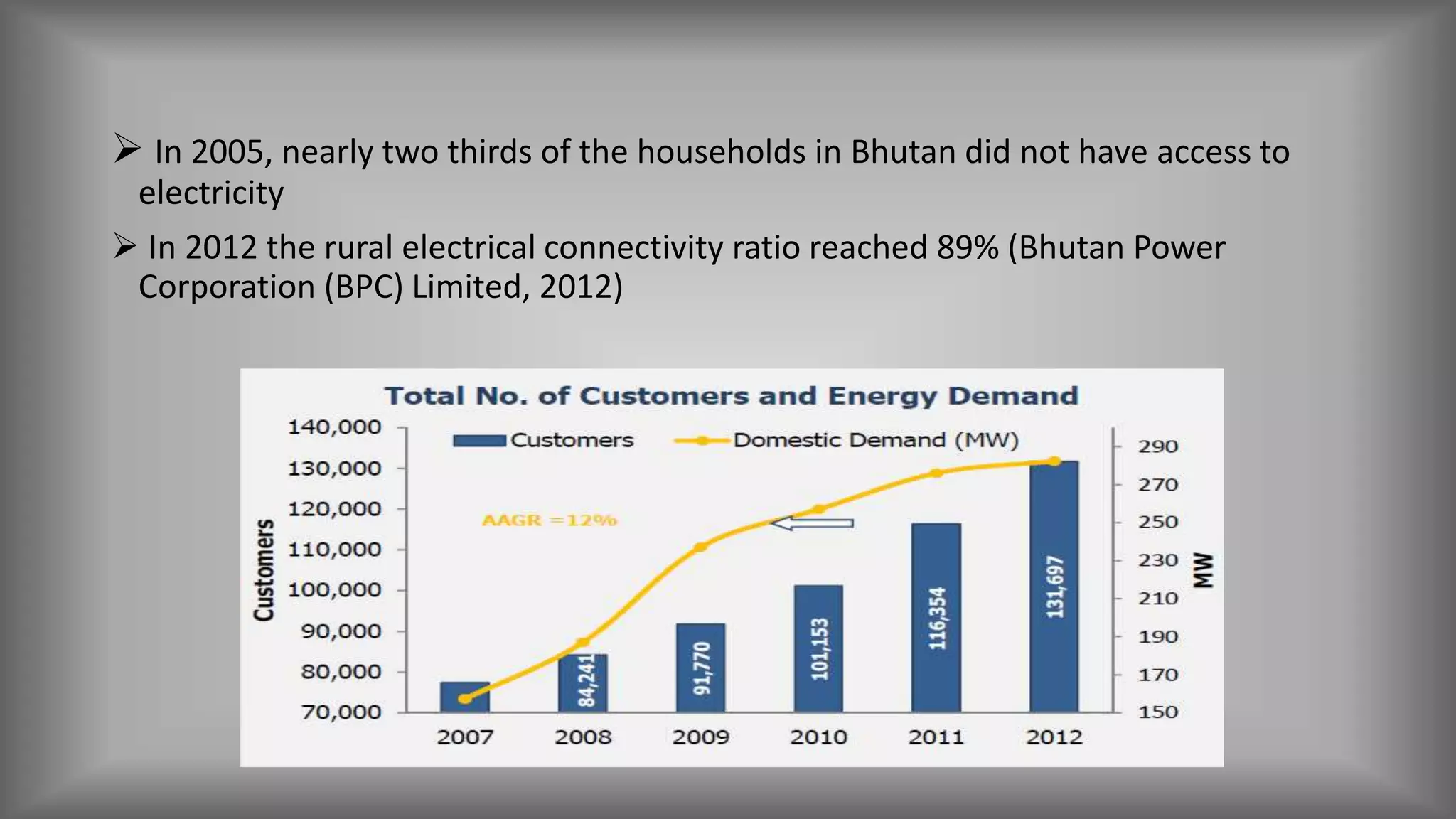

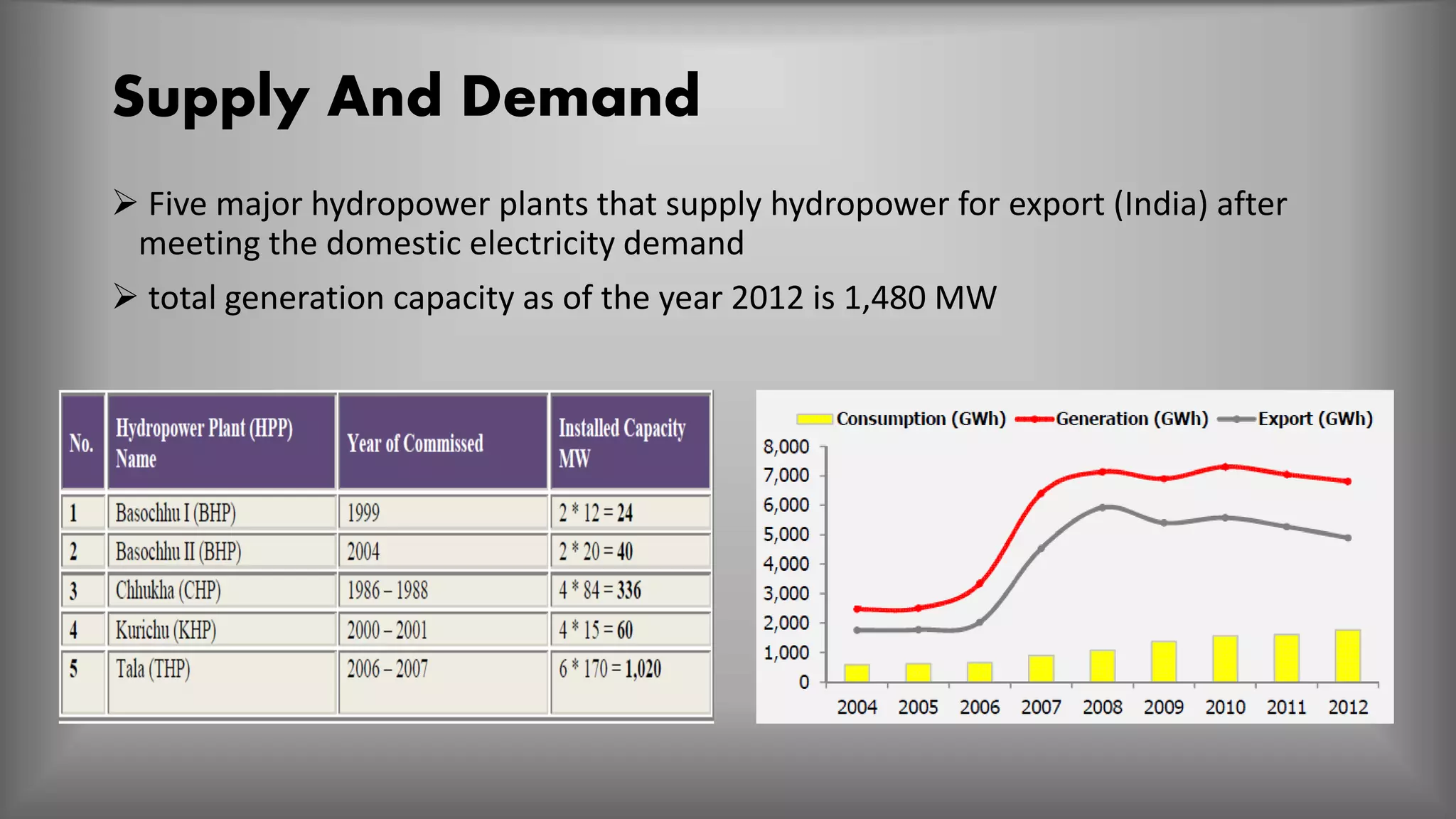

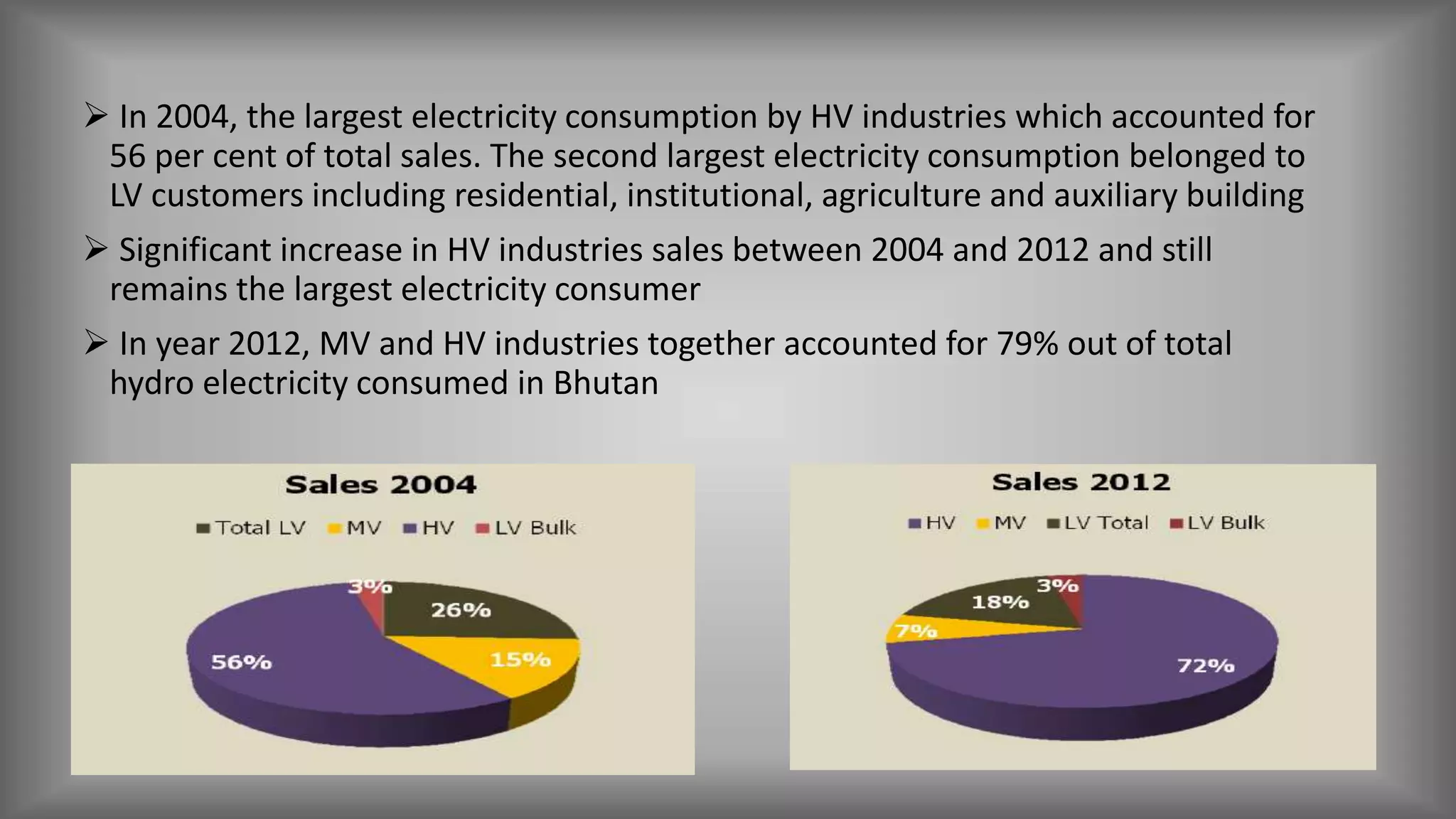

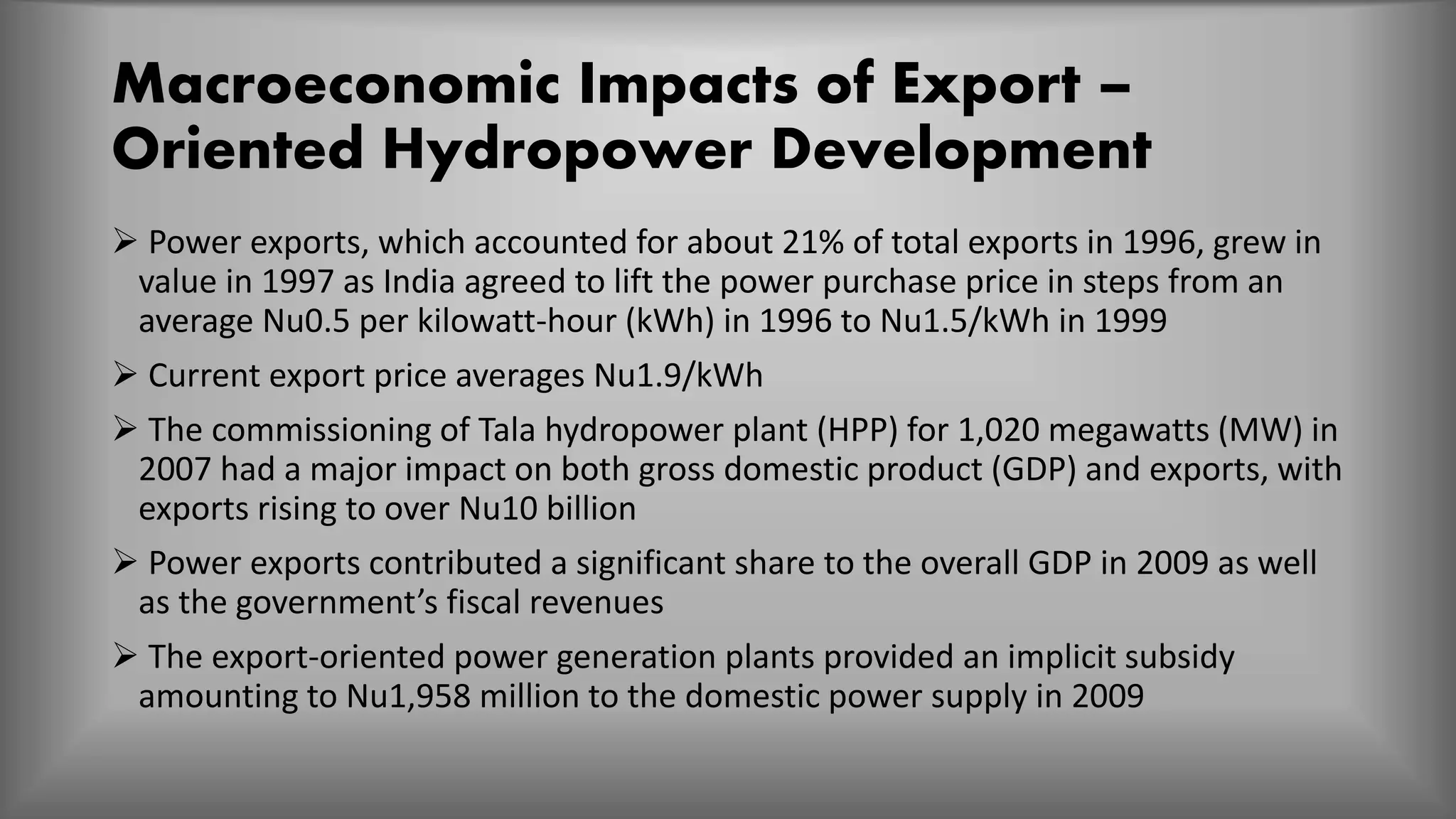

The document provides an overview of Bhutan's power sector, highlighting its reliance on hydroelectricity for economic development and electricity exports, primarily to India. Key challenges include institutional capacity, maintaining rural electrification, and adapting to climate change impacts on hydropower generation. The government has undertaken various five-year plans to achieve 100% electrification and expand hydropower capacity significantly by 2020.