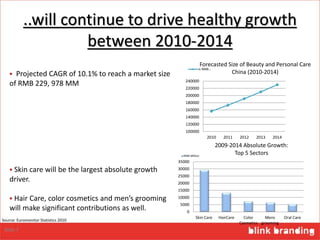

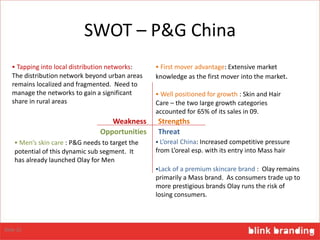

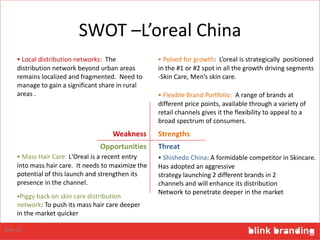

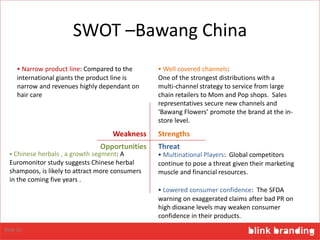

The document discusses the personal care market in China. It finds that the market will continue growing at 10% annually due to rising incomes. Skin care drives the most growth, followed by hair care and men's grooming. International brands currently dominate but have only started tapping the market's potential. L'Oreal China is well positioned across categories to capitalize on opportunities from the growing middle class. Key players like P&G, Unilever, and L'Oreal are strong but face threats from local brands and each other as competition intensifies. The market shifts towards premium and natural products, benefitting leaders able to innovate or leverage prestige brands.