Downloaded 28 times

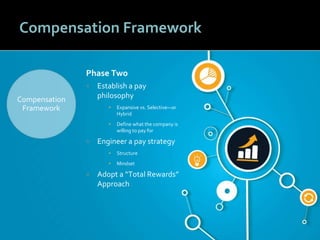

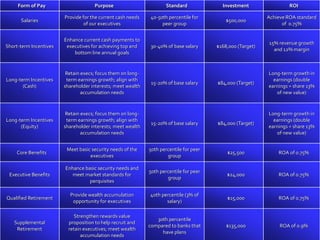

The document outlines strategic pay approaches aimed at enhancing shareholder value through improved employee engagement, performance, and talent attraction. It emphasizes the importance of creating a stewardship mindset and adopting a performance culture, supported by compensation frameworks that reward innovation and align employee contributions with business success. The six key criteria for effective pay strategies are identified as supporting performance frameworks, attracting top talent, fostering stewardship, contributing to performance culture, generating measurable returns, and reflecting a wealth multiplier philosophy.