Download as PDF, PPTX

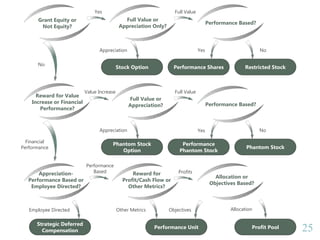

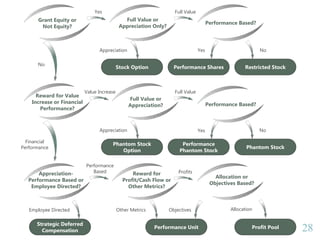

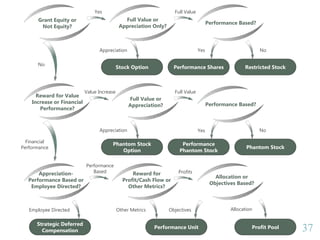

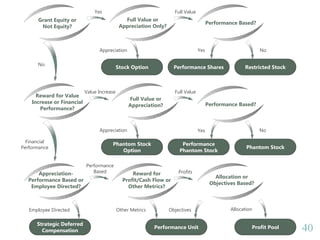

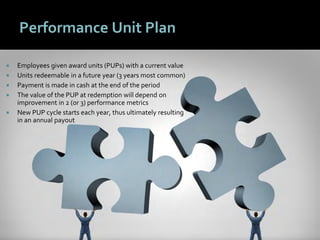

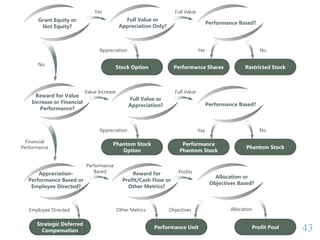

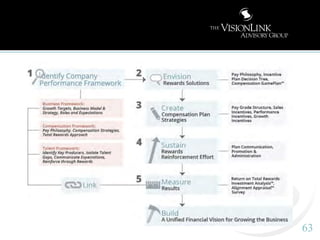

This document discusses alternatives to sharing stock for long-term incentive plans (LTIPs) in private companies. It begins with an introduction to VisionLink Advisors and their focus on helping businesses build high-performance cultures through pay strategies. The bulk of the document then reviews 9 different non-stock alternatives to traditional equity compensation, including phantom stock, profit pools, and performance units. For each option, it outlines the key characteristics and how it could work. The document concludes by providing steps to implement the alternatives once a plan type is selected.