Downloaded 17 times

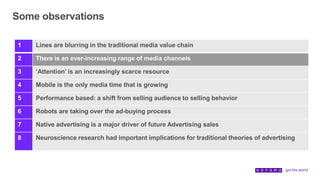

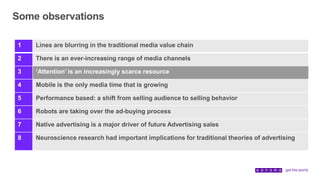

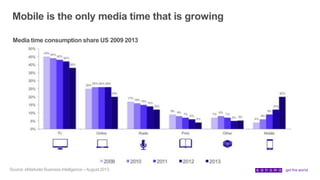

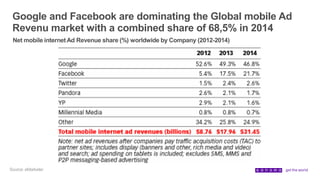

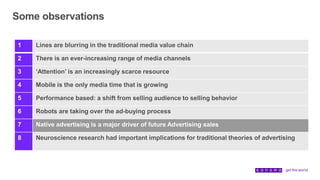

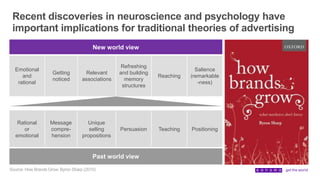

The document discusses next generation advertising solutions. It notes that traditional media value chains are blurring as publishers become agencies, agencies become content creators, and brands create content. It also notes the proliferation of new media channels, the increasing scarcity of attention, mobile as the only growing media time, the shift to performance-based advertising, the rise of programmatic buying and native ads, and implications of neuroscience research for advertising theory. The author works at Sanoma Media Netherlands and discusses how their large portfolio of media assets can help clients succeed across different target audiences and parts of the customer journey.