Downloaded 387 times

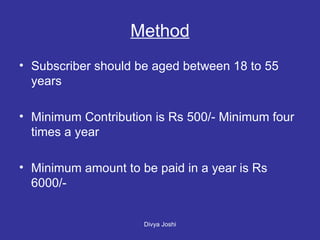

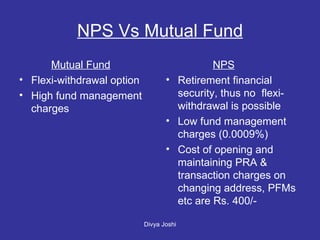

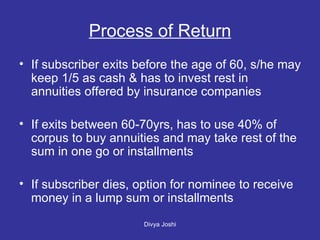

NPS is India's national pension system that allows individuals to save for retirement. Key points: 1. Individuals between 18-55 can contribute a minimum of Rs. 500 four times a year (Rs. 6,000 annually) to their PRAN (Permanent Retirement Account Number). 2. Contributions are invested by Pension Fund Managers in a mix of stocks, government bonds, and corporate bonds. The default allocation depends on the saver's age. 3. At retirement (age 60 or older), up to 60% can be withdrawn tax-free, with the remainder used to purchase an annuity from an insurance company. 4. NPS has lower fees than mutual