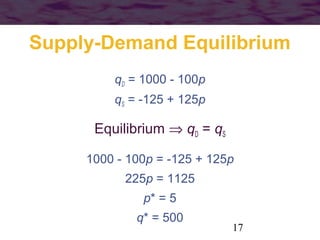

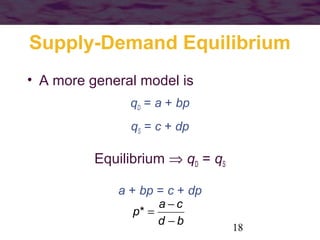

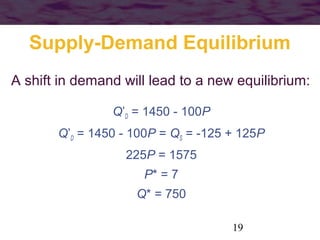

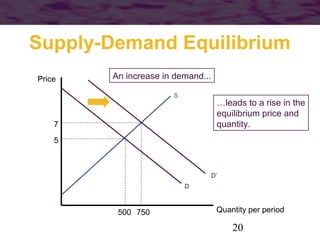

This document provides an overview of microeconomic theory and modeling. It discusses how economists use simple models to understand resource allocation, highlighting the supply-demand model. It also explains general equilibrium models look at multiple markets simultaneously and how models are tested through direct evaluation of assumptions and indirect assessment of predictive power. The document outlines key concepts like optimization, ceteris paribus, and the distinction between positive and normative analysis.