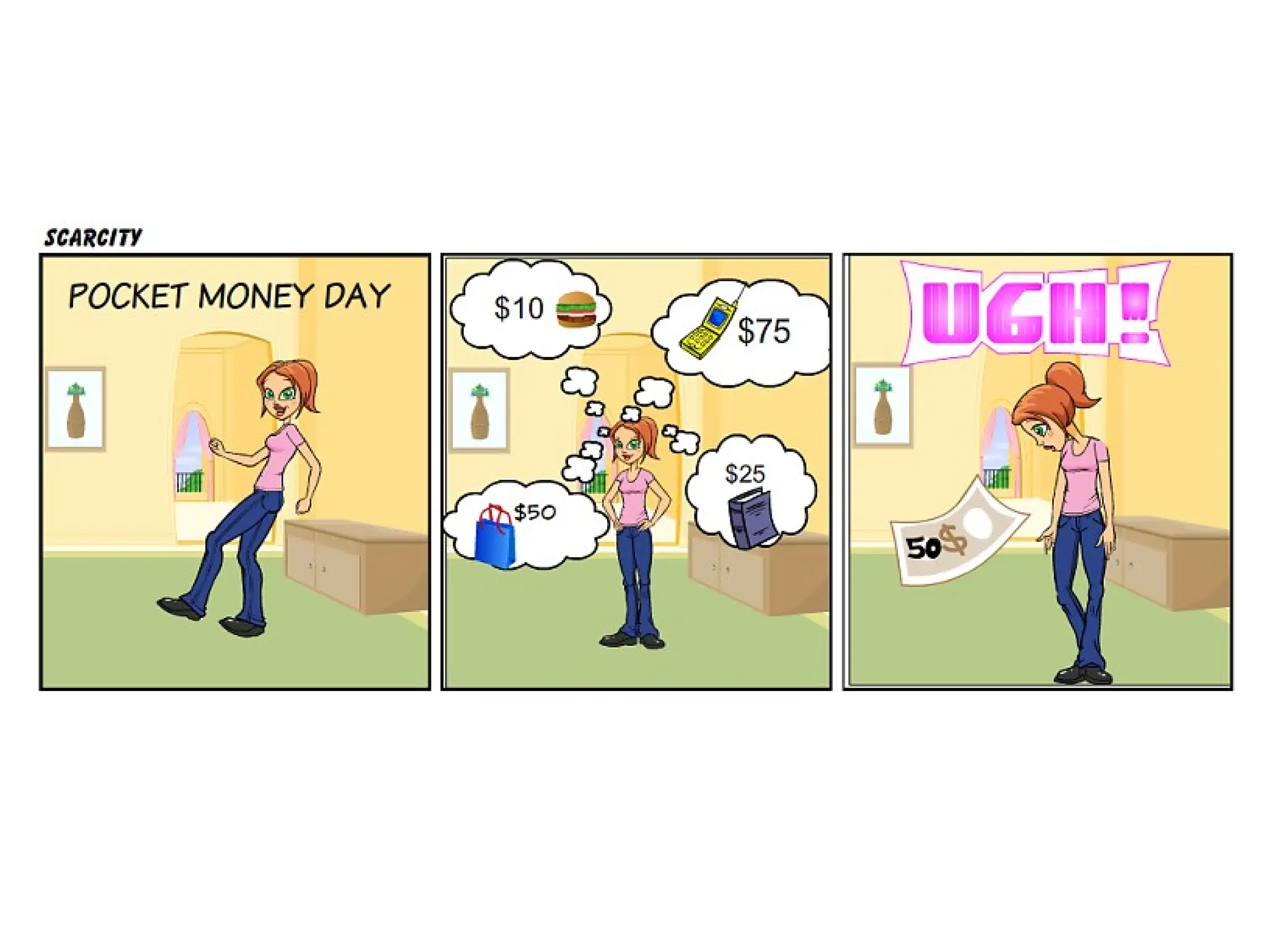

What is Economics?

•Is there a limitation on how much money you

can spend each month?

3.

What is Economics?

•Your limited budget is one example of limited

resources (scarce resources).

• Scarcity: A situation in which unlimited wants

exceed the limited resources available to fulfill

those wants

5.

What is Economics?

•When you decide how to spend your budget, you

are a decision maker (economic agent).

Economic agents: decision makers.

• In economics, agents are

– self interest

– rational

• using all available information to achieve your goals.

• Rational consumers and firms weigh the benefits and costs of

each action and try to make the best decision possible.

6.

What is Economics?

•Textbook: Economics is the study of

1. how agents choose to allocate scarce resources,

and

2. how those choices affects society.

• Your understanding?

8.

What is Macroeconomics?

Economicsconcludes:

• Microeconomics is the study of

– how households and firms make choices,

– how they interact in markets, and

– how the government attempts to influence their choices

– how individuals, firms, and governments make choices.

• Macroeconomics is the study of the economy as a whole.

9.

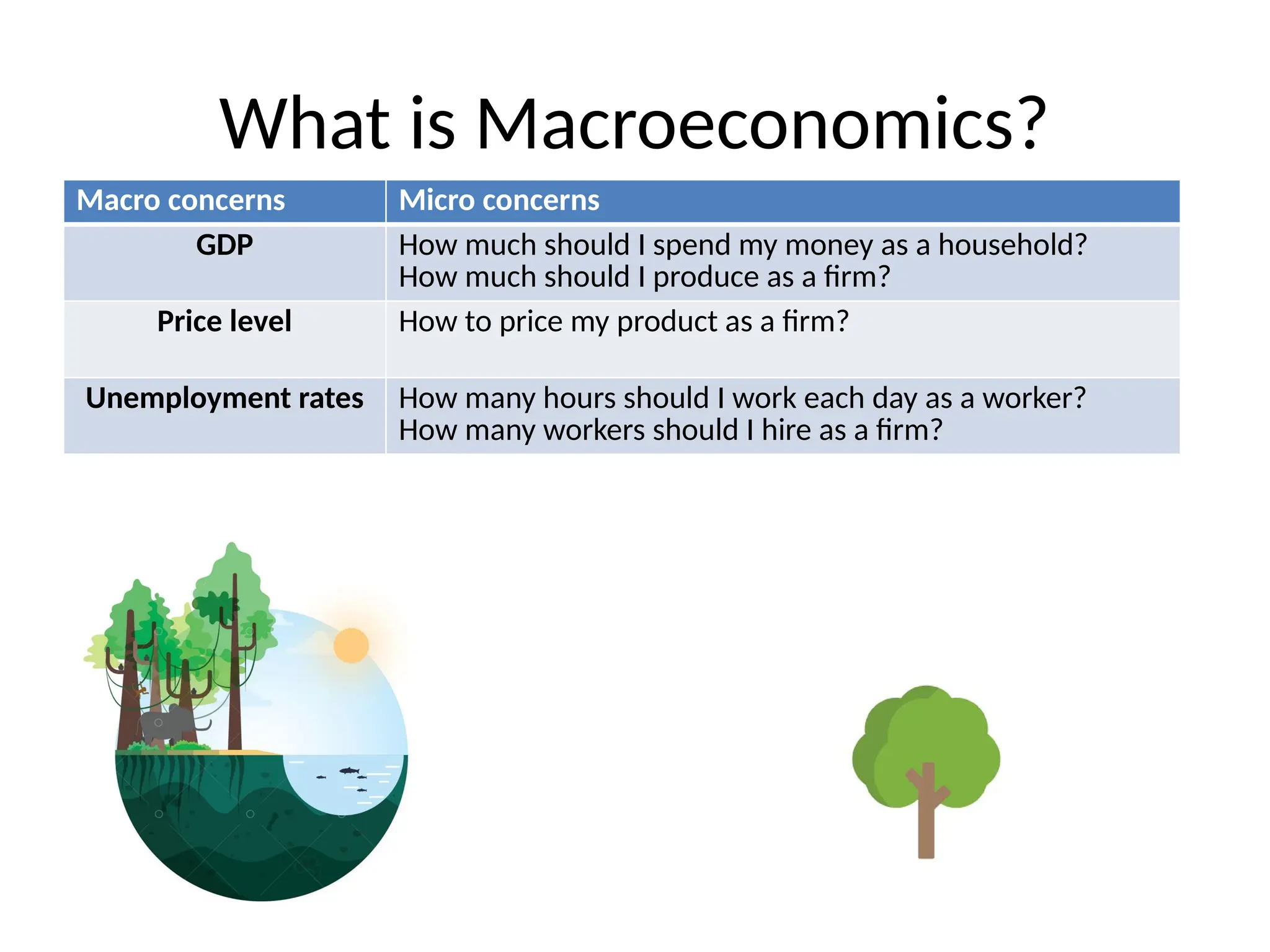

What is Macroeconomics?

Macroconcerns Micro concerns

GDP How much should I spend my money as a household?

How much should I produce as a firm?

Price level How to price my product as a firm?

Unemployment rates How many hours should I work each day as a worker?

How many workers should I hire as a firm?

10.

The Economic Wayof Thinking

• Optimization: choosing the best feasible

option with given constraints (information,

knowledge, budget, experience, training, etc).

• Equilibrium: a situation in which everyone is

simultaneously optimizing, so nobody would

benefit personally by changing his or her own

behavior, given the choices of others.

– Next: one example of equilibrium

11.

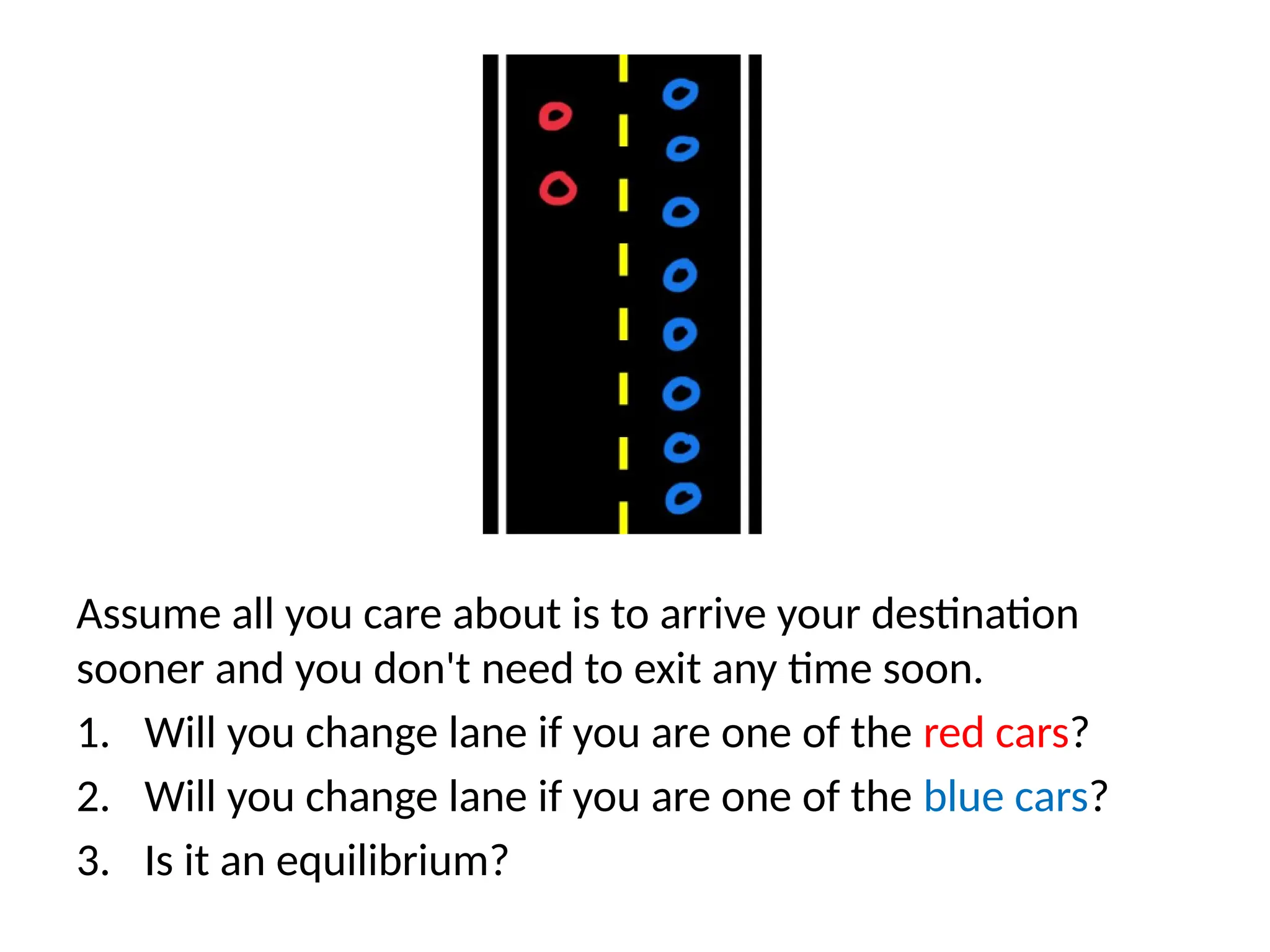

Assume all youcare about is to arrive your destination

sooner and you don't need to exit any time soon.

1. Will you change lane if you are one of the red cars?

2. Will you change lane if you are one of the blue cars?

3. Is it an equilibrium?

12.

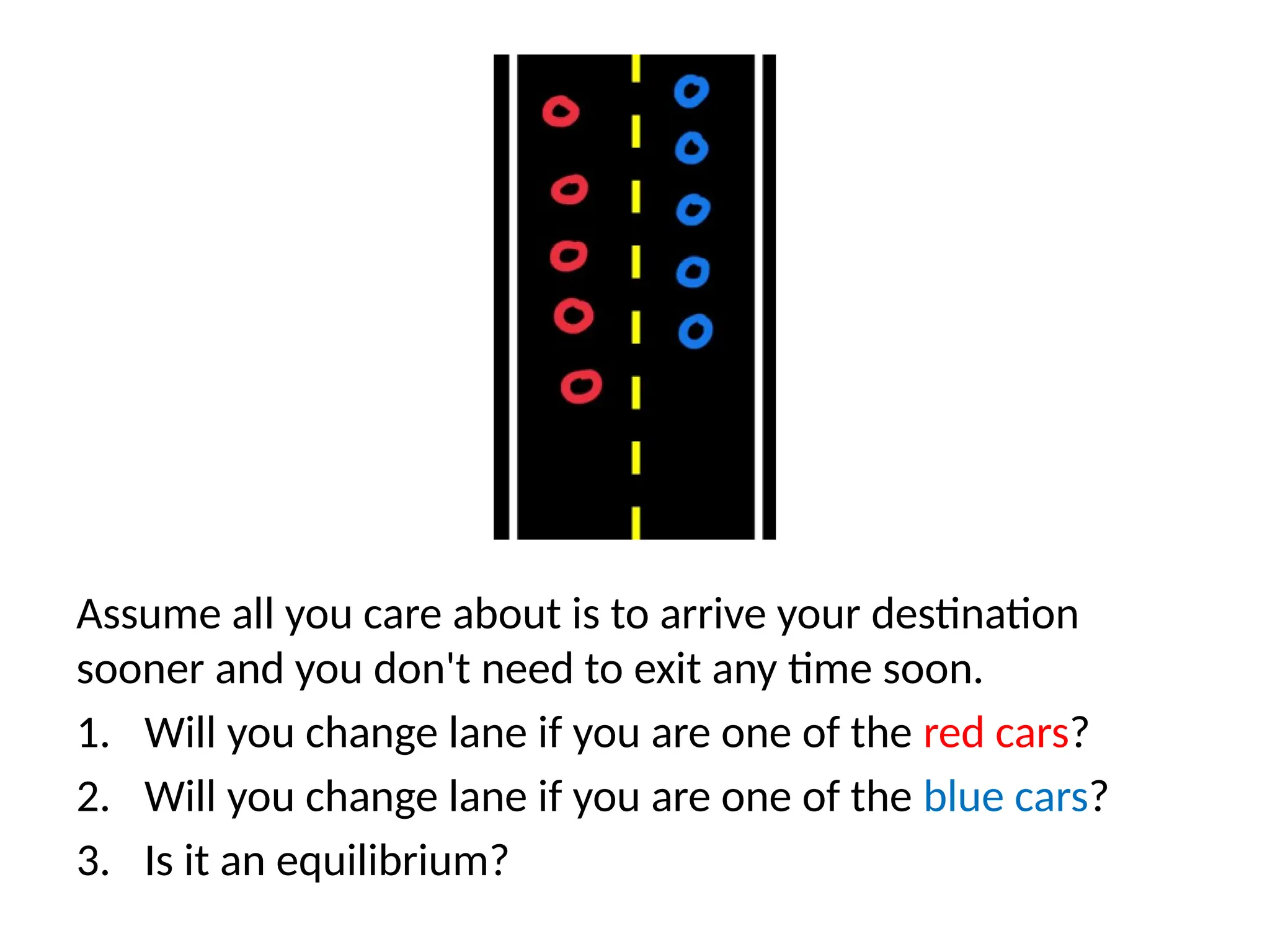

Assume all youcare about is to arrive your destination

sooner and you don't need to exit any time soon.

1. Will you change lane if you are one of the red cars?

2. Will you change lane if you are one of the blue cars?

3. Is it an equilibrium?

13.

The Economic Wayof Thinking

• Optimization: choosing the best feasible option with given

constraints (information, knowledge, budget, experience,

training, etc).

• Equilibrium: a situation in which everyone is

simultaneously optimizing, so nobody would benefit

personally by changing his or her own behavior, given the

choices of others.

– This intro level class concentrates on the “good equilibria” only.

• Resource use is efficient if it is not possible to make

someone better off without making someone else worse

off.

14.

The Economic Wayof Thinking

Empiricism is analysis that uses data, evidence-

based analysis.

• Economists use data to develop theories, to

test theories, to evaluate the success of

different government policies, and to

determine what is causing things to happen in

the world.

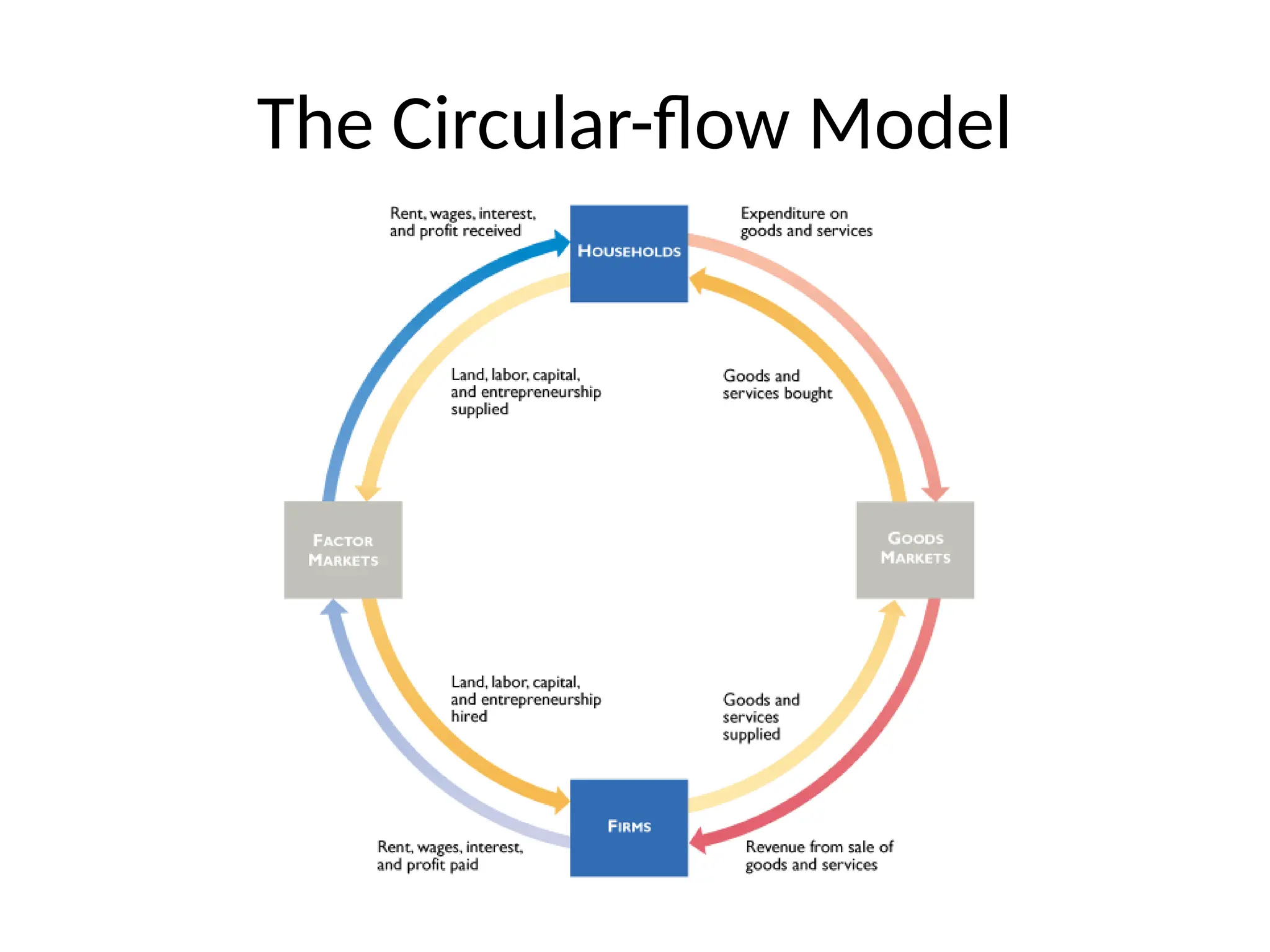

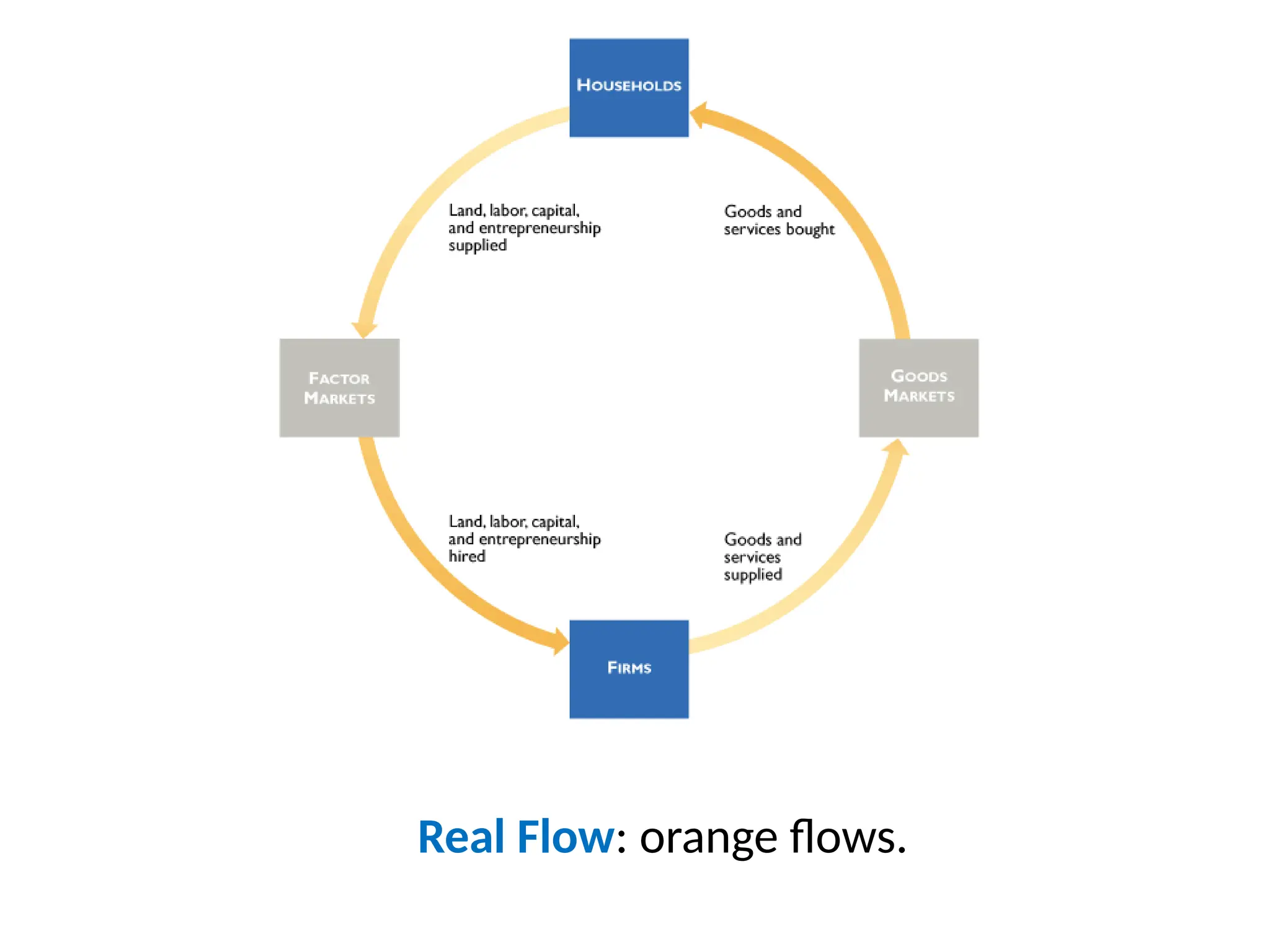

The Circular-flow Model

Market:a group of buyers and sellers of a good or service and the

institution or arrangement by which they come together to trade

• A free market is one with few government restrictions on how

a good or service can be produced or sold, or on how a factor

of production can be employed.

• Goods (and services) markets are markets in which goods and

services are bought and sold.

• Factor markets are markets in which factors of production are

bought and sold.

– https://www.stlouisfed.org/education/economic-lowdown-podcast-ser

ies/episode-2-factors-of-production

17.

The Circular-flow Model

Labor:the effort that people contribute to the production of

goods and services.

• Examples: work done by the waiter who brings your food;

artist's creation of a painting.

18.

The Circular-flow Model

Land:includes any natural resource used to produce goods and

services; anything that comes from the land.

• Some common land or natural resources are water, oil, copper, natural

gas, coal, and forests.

• Land resources are the raw materials in the production process.

• These resources can be renewable, such as forests, or nonrenewable

such as oil or natural gas.

19.

The Circular-flow Model

Capital:manufactured goods that are used to produce other goods and

services.

• The tools, instruments, machines, buildings, and other constructions that

businesses used for production.

• Examples: hammers, forklifts, computers, delivery vans, textbooks,

whiteboards, etc.

20.

The Circular-flow Model

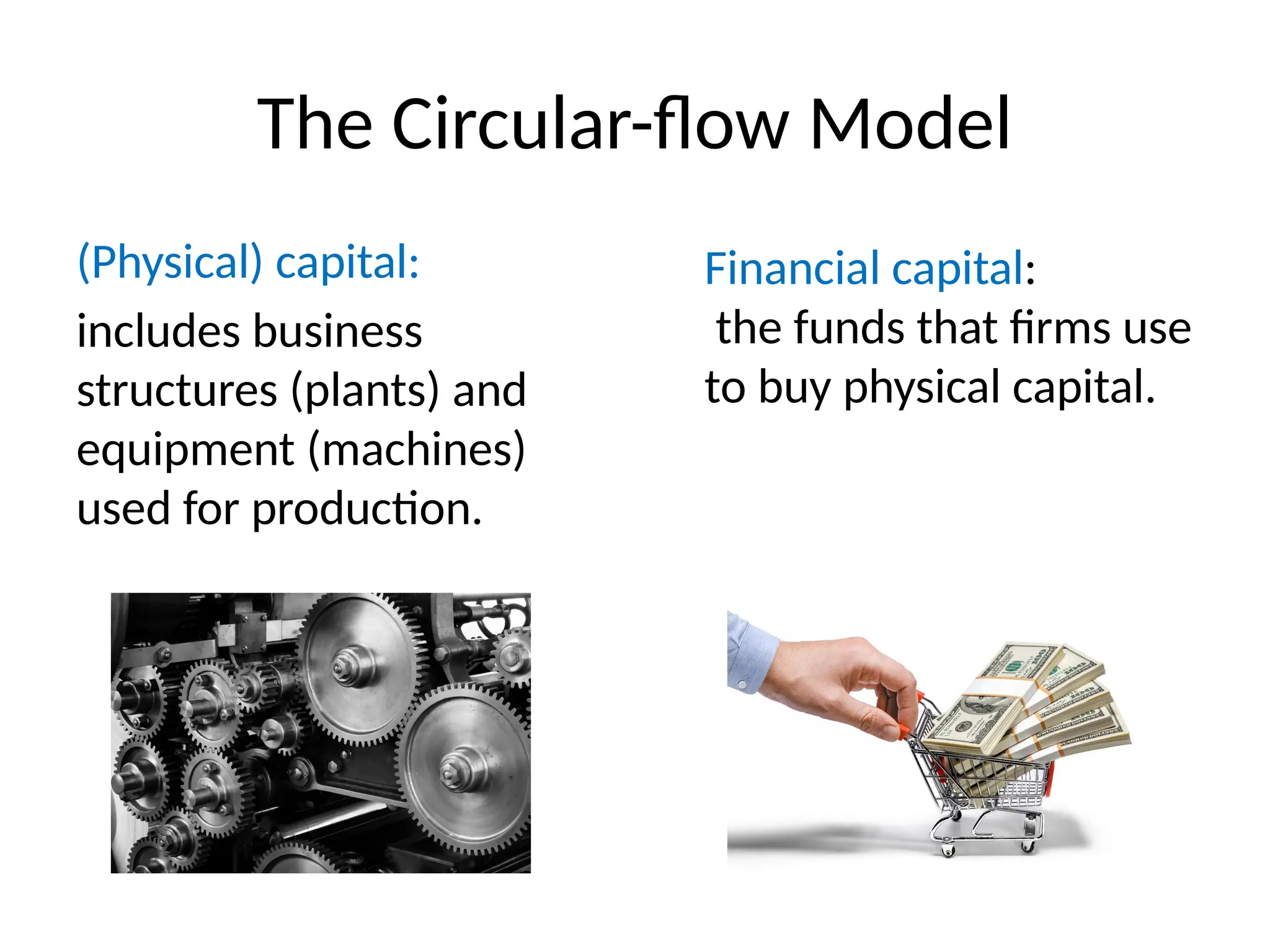

(Physical)capital:

includes business

structures (plants) and

equipment (machines)

used for production.

Financial capital:

the funds that firms use

to buy physical capital.

21.

The Circular-flow Model

Entrepreneurship:is someone who brings together the factors of production—

land, labor, and capital—to produce goods and services and earn profits.

• The most successful entrepreneurs are innovators who find new ways to

produce goods and services or who develop new goods and services to bring

to market.

• Entrepreneurs can be a vital engine of economic growth (helping to build

some of the largest firms in the world)

22.

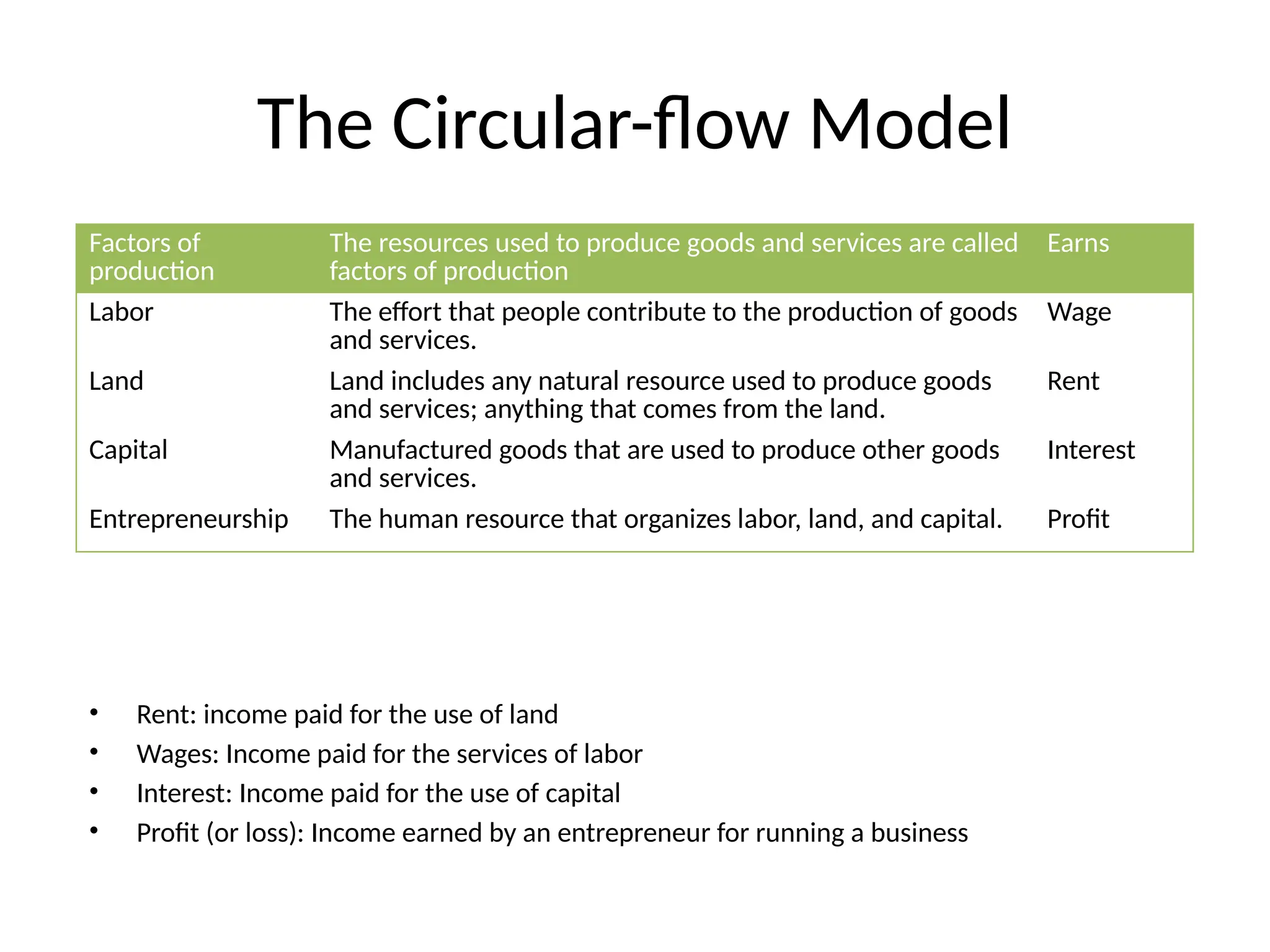

The Circular-flow Model

Factorsof

production

The resources used to produce goods and services are called

factors of production

Earns

Labor The effort that people contribute to the production of goods

and services.

Wage

Land Land includes any natural resource used to produce goods

and services; anything that comes from the land.

Rent

Capital Manufactured goods that are used to produce other goods

and services.

Interest

Entrepreneurship The human resource that organizes labor, land, and capital. Profit

• Rent: income paid for the use of land

• Wages: Income paid for the services of labor

• Interest: Income paid for the use of capital

• Profit (or loss): Income earned by an entrepreneur for running a business

23.

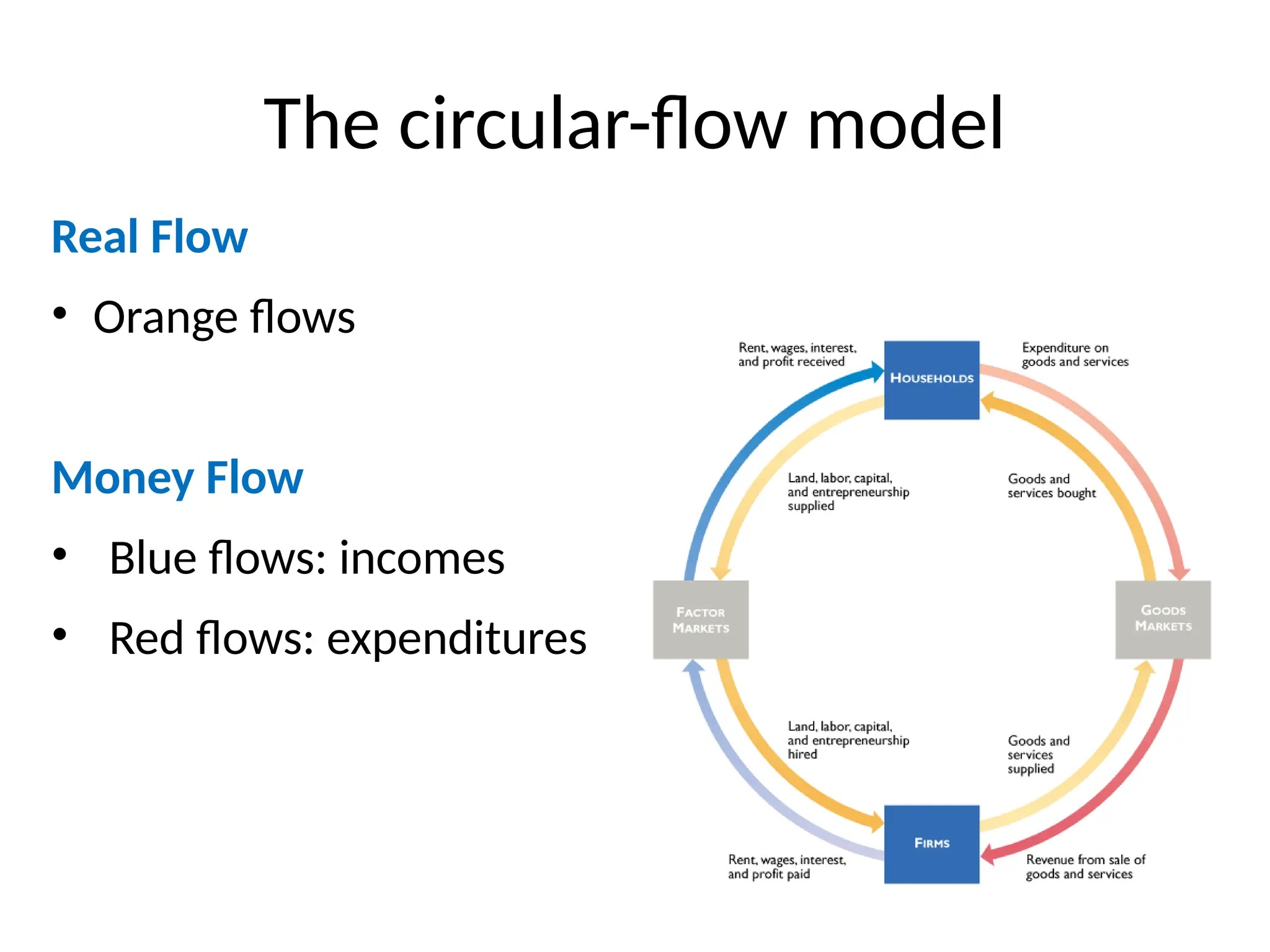

The Circular-flow Model

Realflow:

• In goods markets

o Who offers goods and

services?

o Who receives goods and

services?

• In factor markets (say labor

market)

o Who offers production

factors?

o Who receives production

factors?

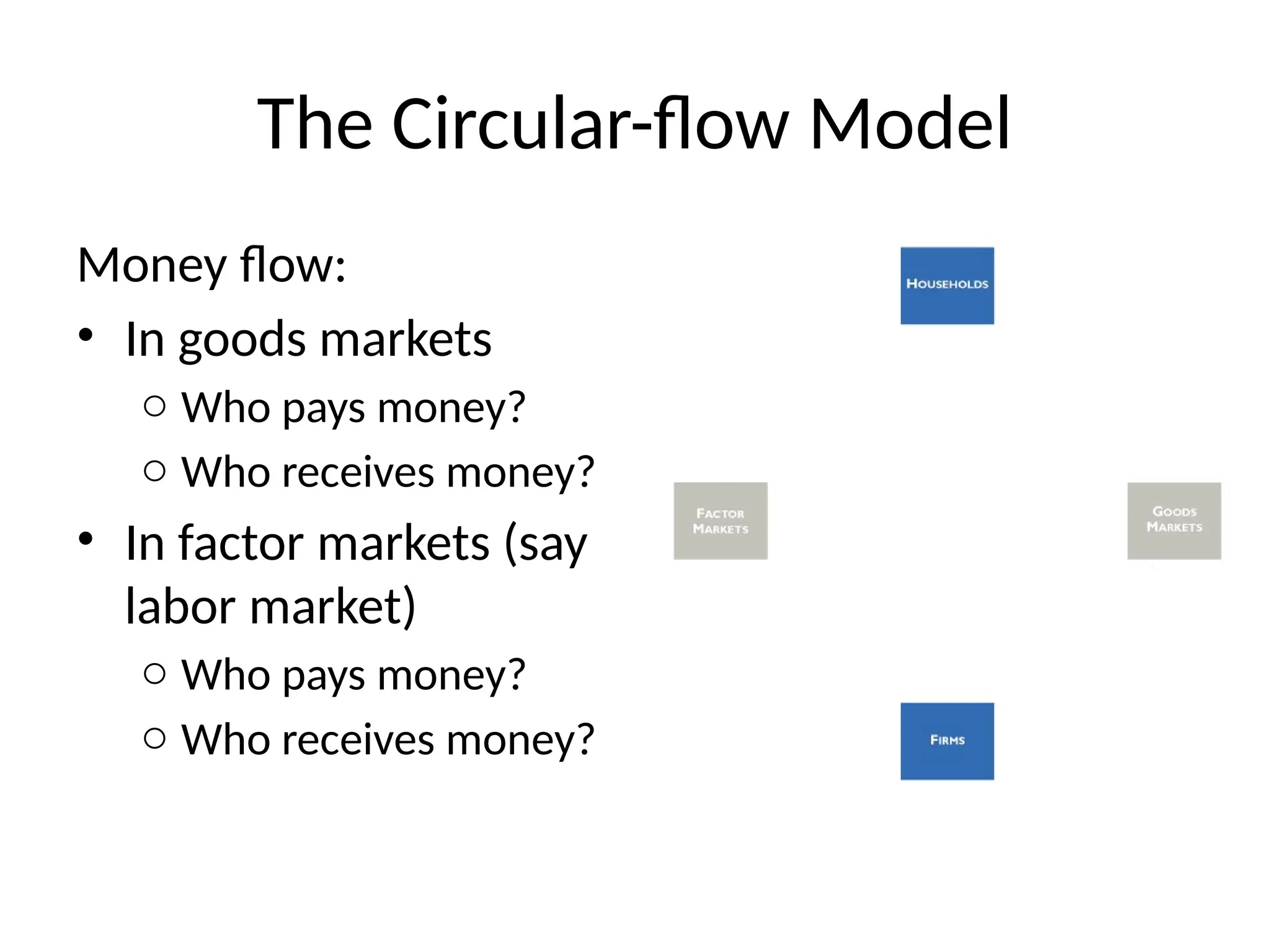

The Circular-flow Model

Moneyflow:

• In goods markets

o Who pays money?

o Who receives money?

• In factor markets (say

labor market)

o Who pays money?

o Who receives money?

The Circular-flow Model

Questions:

1.Are there any elements you want to add to

this 4-sector circular flow model?

2. Households do not always spend all their

income. Are savings a leakage from circular

flow?

28.

Economic Model

Economic model:simplified versions of reality

used to analyze real-world economic situations

• It is a description of some aspect of the

economic world that includes only those

features that are needed for the purpose at

hand.

29.

Economic Model

Economists developeconomic models to analyze real-world issues.

• Building an economic model often follows these steps:

1. Decide on the assumptions to use in developing the model.

2. Formulate a testable hypothesis.

3. Use economic data to test the hypothesis.

4. Revise the model if it fails to explain the economic data well.

5. Retain the revised model to help answer similar economic questions in the

future.

• Assumptions and simplifications: every model needs them in order to be

useful.

• Testability: good models generate testable predictions, which can be verified

or disproven using data.

• Economic variables: something measurable that can have different values,

such as the incomes of doctors.

30.

The Scientific Natureof Economics

• Economists try to mimic natural scientists by using the

scientific method. But economics is a social science;

studying the behavior of people is often tricky.

• When analyzing human behavior, we can perform:

– Positive analysis: the study of “what is?”; and/or

– Normative analysis: the study of “what ought to be?”

• Economists generally perform positive analysis.

31.

Types of Economies

•Centrally planned economies result when governments decide

what to produce, how to produce it, and who received the goods

and services.

• Market economies result when the decisions of households and

firms determine what is produced, how it is produced, and who

receives the goods and services.

• Mixed economies have features of both of the above. Most

economic decisions result from the interaction of buyers and

sellers, but governments play a significant role in the allocation of

resources.

32.

Efficiency of Economies

Marketeconomies tend to be more efficient than centrally-planned

economies.

Market economies promote:

• Productive efficiency, where goods or services are produced at the

lowest possible cost; and

• Allocative efficiency, where production is consistent with consumer

preferences: the marginal benefit of production is equal to its marginal

cost

• These efficiencies come about because all transactions result from

voluntary exchange: transactions that make both the buyer and seller

better off.

33.

Efficiency of Economies

Marketsmay not result in fully efficient outcomes. For example:

• People might not immediately do things in the most efficient

way

• Governments might interfere with market outcomes

• Market outcomes might ignore the desires of people who are

not involved in transactions – ex: pollution

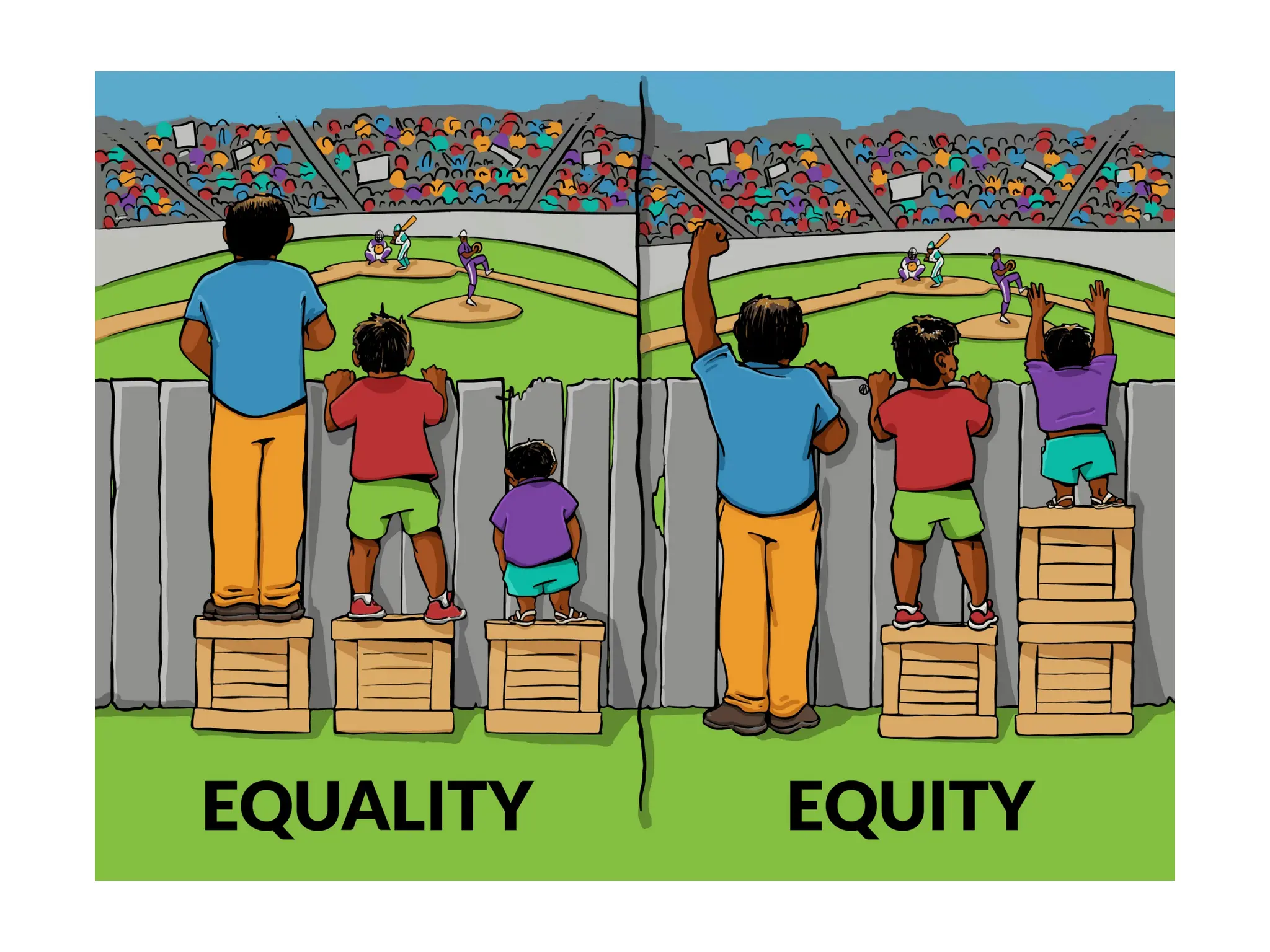

Economically efficient outcomes may not be the most desirable.

Markets result in high inequality; some people prefer more

equity, i.e. fairer distribution of economic benefits.