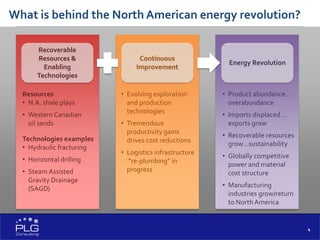

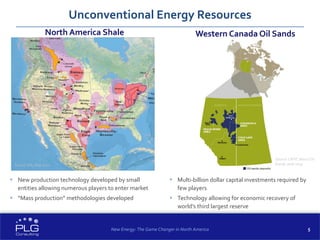

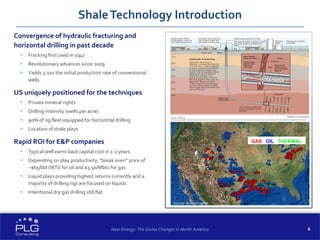

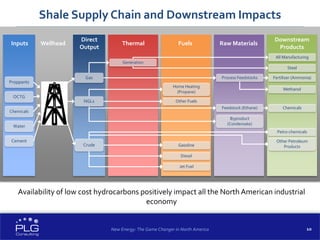

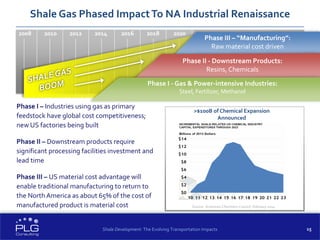

The document discusses the transformative impact of new energy resources, particularly shale oil and natural gas, on the North American supply chain and manufacturing sectors. It highlights advancements in extraction technologies, the economic benefits of domestic energy production, and the logistical changes in energy distribution across the continent. Additionally, it outlines the implications for related industries and the potential for Mexico to enhance its energy sector through liberalization and collaboration with U.S. companies.

![[PRESENTATION] PLEA 2017 | Ethane--a green(er) clean(er) transportation fuel ...](https://cdn.slidesharecdn.com/ss_thumbnails/ethaneplea2017final-170702001739-thumbnail.jpg?width=640&height=640&fit=bounds)

![Energy renaissance-outlook-2013[1]](https://cdn.slidesharecdn.com/ss_thumbnails/energy-renaissance-outlook-20131-130409141220-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)