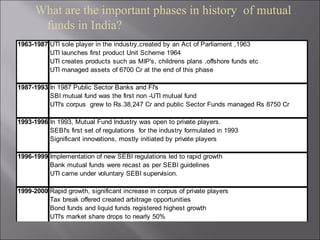

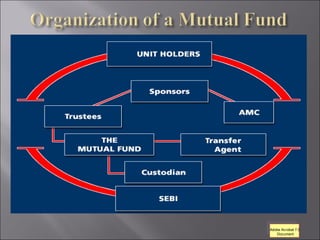

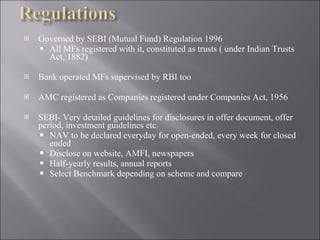

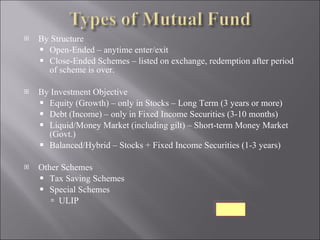

The document discusses mutual funds in India. It provides an overview of what mutual funds are, how they help with financial planning objectives, the important phases in the history of mutual funds in India, different types of mutual funds based on structure and investment objectives, factors to consider when investing in mutual funds, benefits of investing in mutual funds, potential disadvantages, and industry growth projections.

![Mutual funds[1]](https://cdn.slidesharecdn.com/ss_thumbnails/mutualfunds1-140128115104-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)