Downloaded 215 times

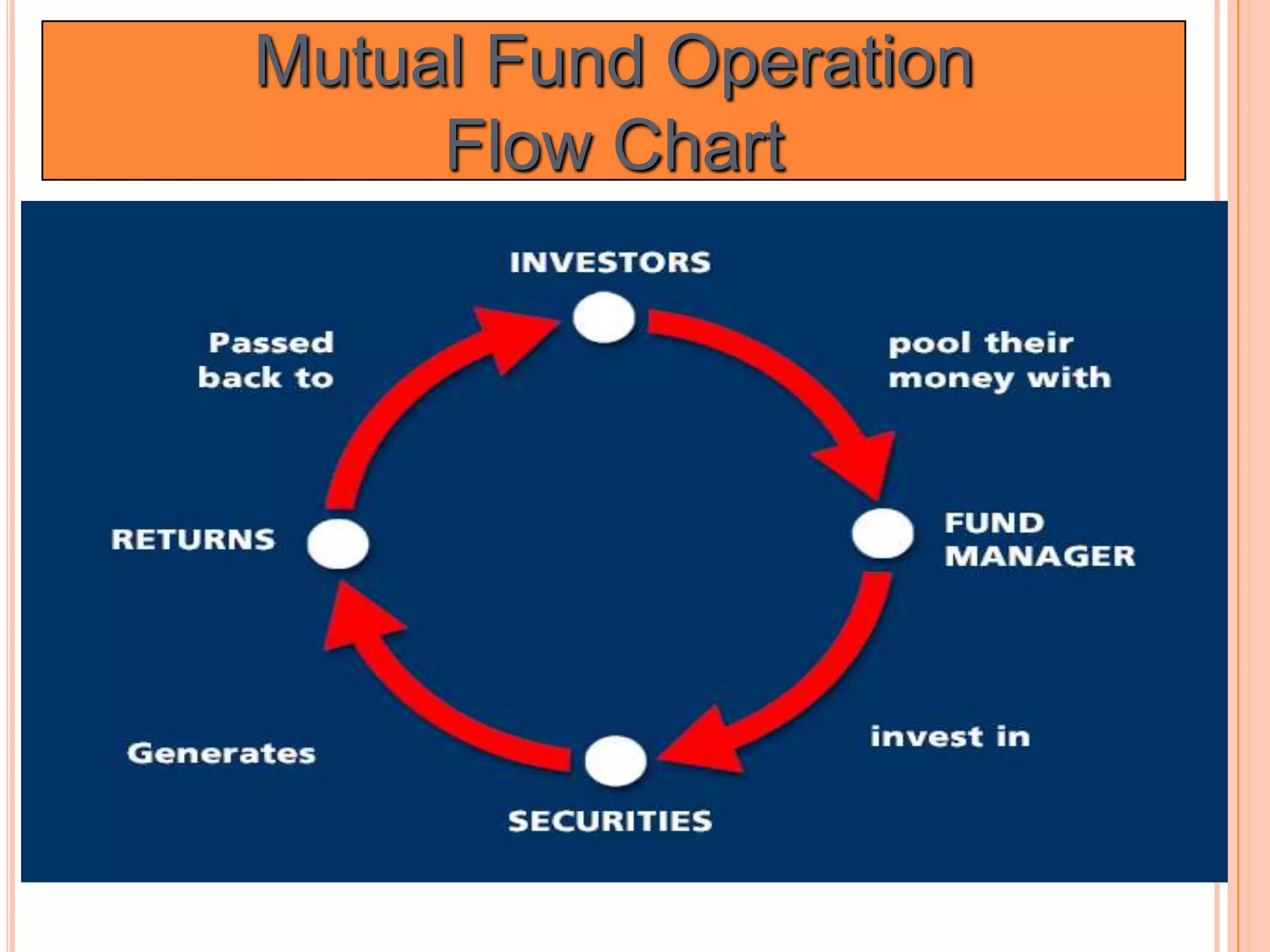

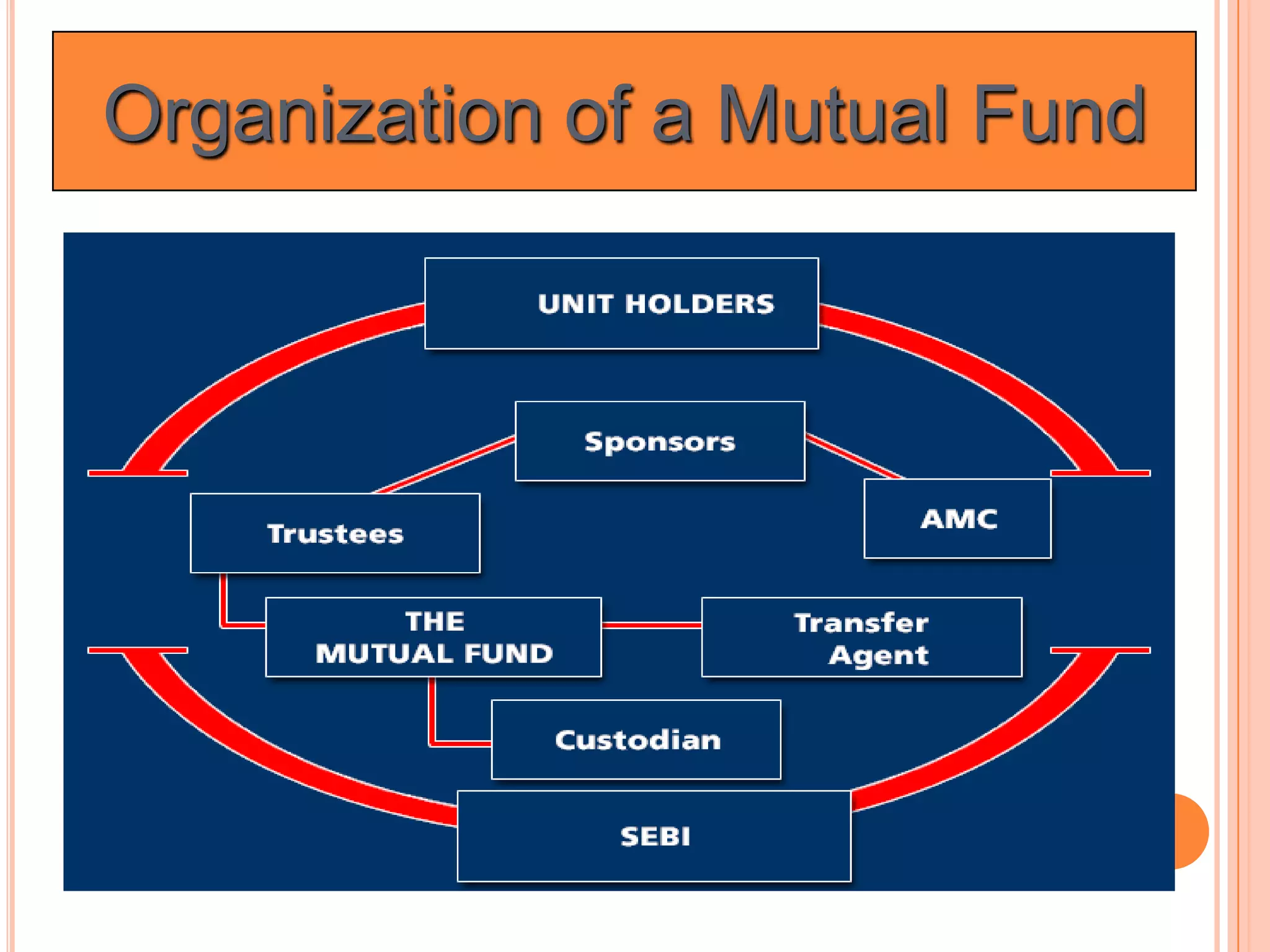

Mutual funds are professionally managed investment funds that pool money from many investors to purchase securities like stocks, bonds, and money market instruments. The fund is overseen by a fund manager who buys and sells assets according to the fund's investment objective. Investors share in the income and capital gains of the fund proportionate to their investment. Mutual funds offer diversification, affordability, and professional management for individual investors. Some disadvantages include lack of a tailored portfolio and potential underperformance. Mutual funds are regulated in India by SEBI and operate through a trust structure with sponsors, trustees, asset management companies, and third party administrators.

An introduction to the wealth management course by S G Raja Sekharan.

Definition of mutual funds, their management by fund managers, and shared income among unit holders.

Advantages include affordability, professional management, diversification, and tax benefits.

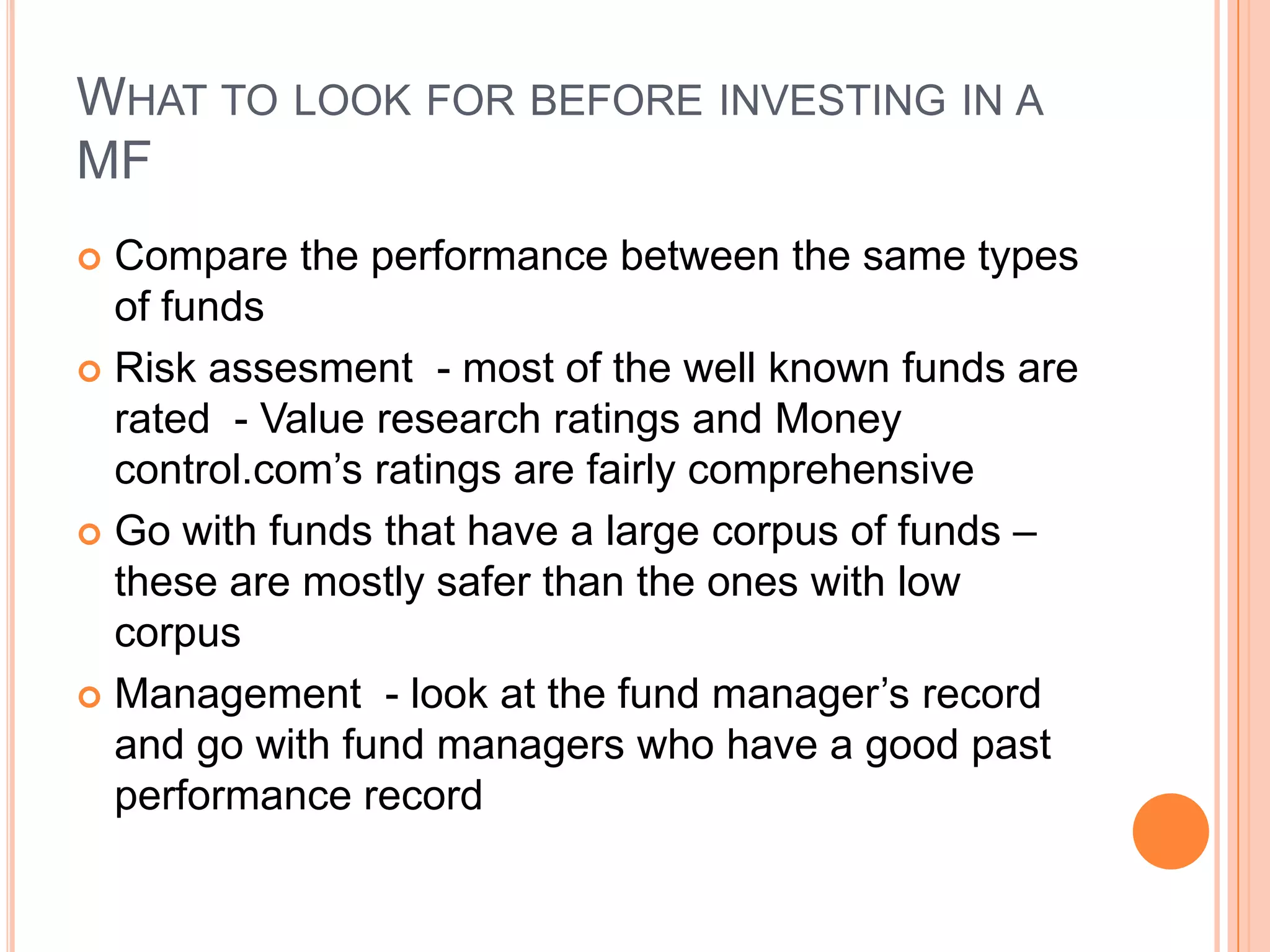

The lack of customized portfolio options in mutual fund investments.

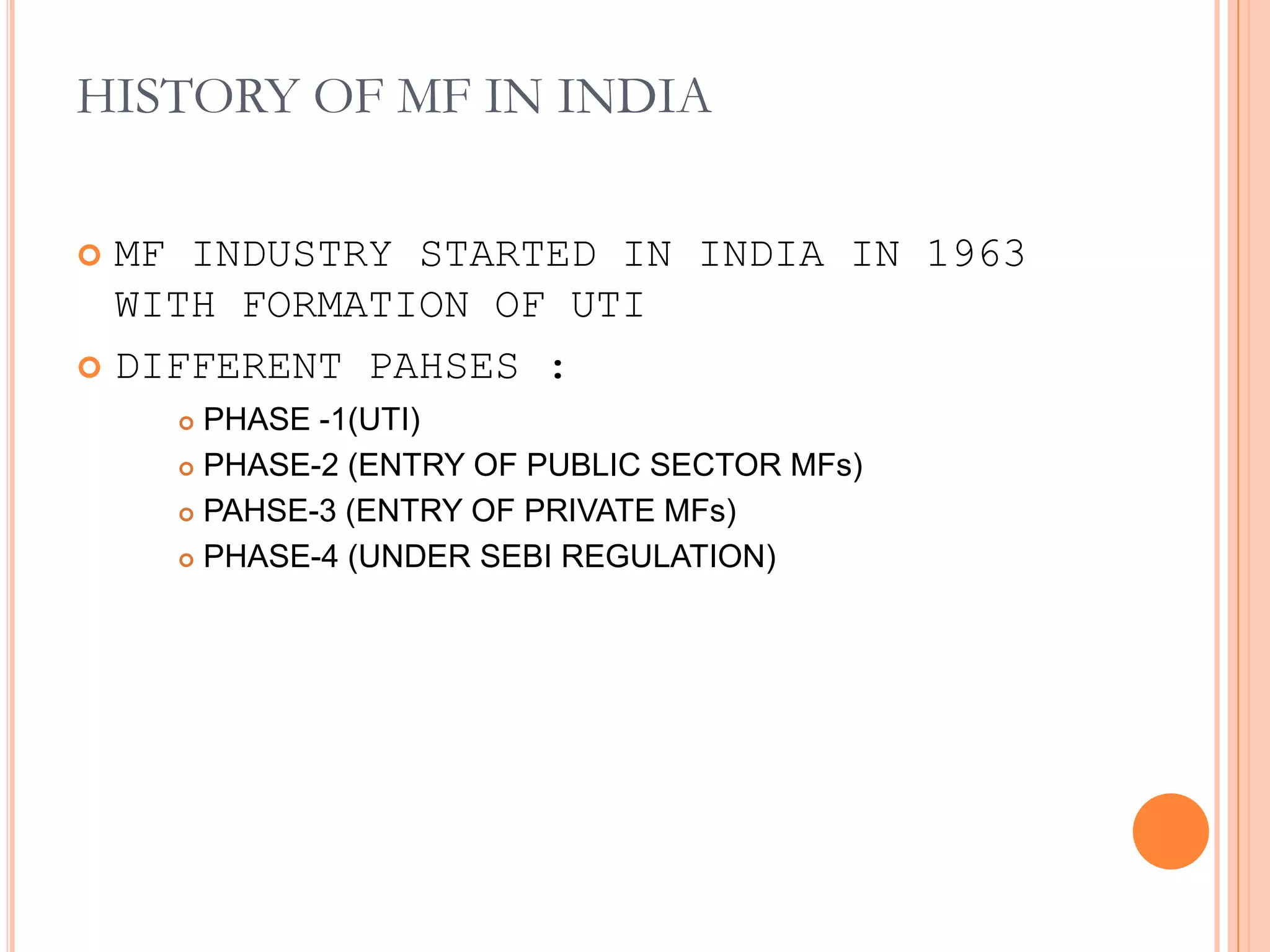

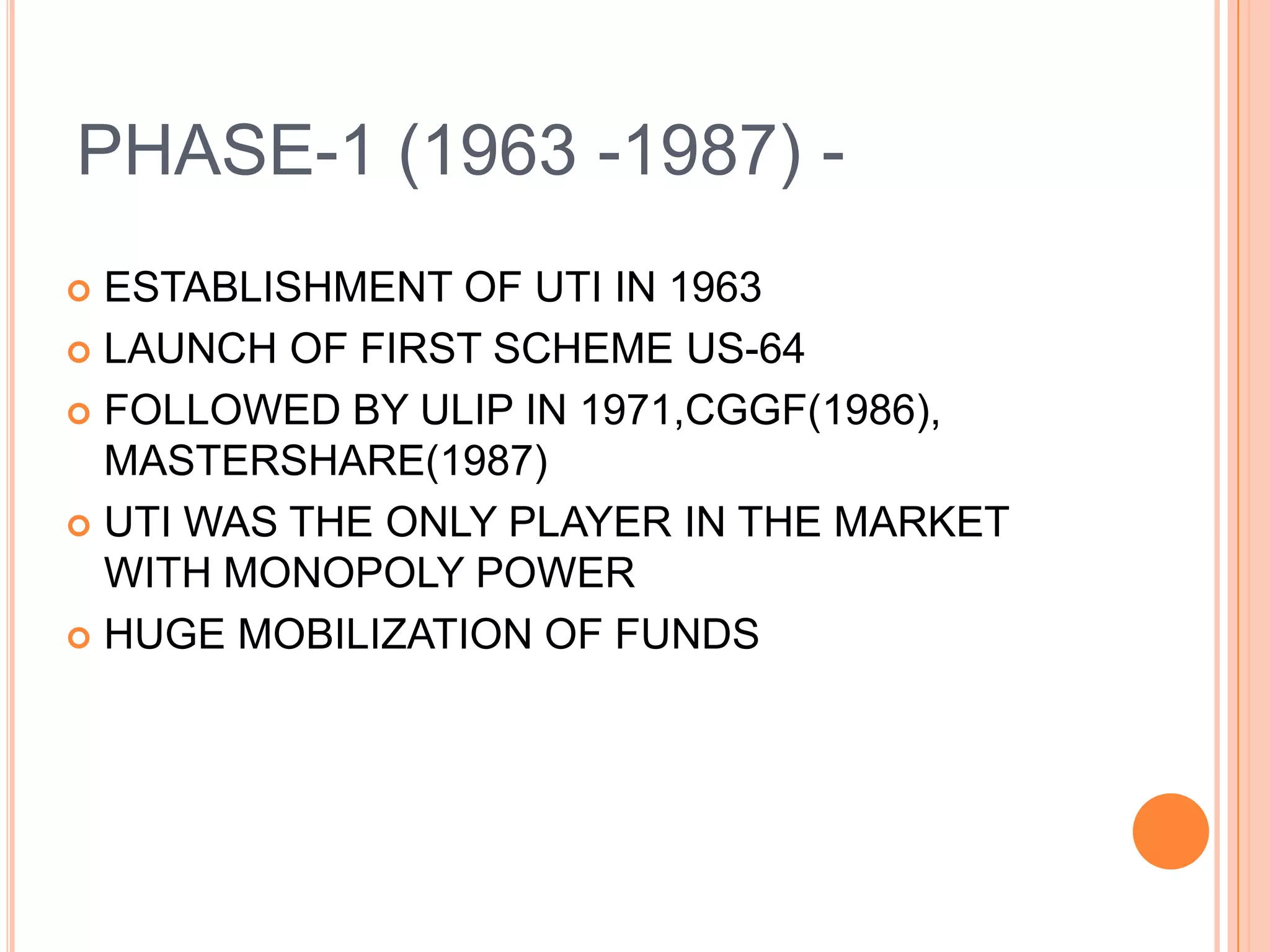

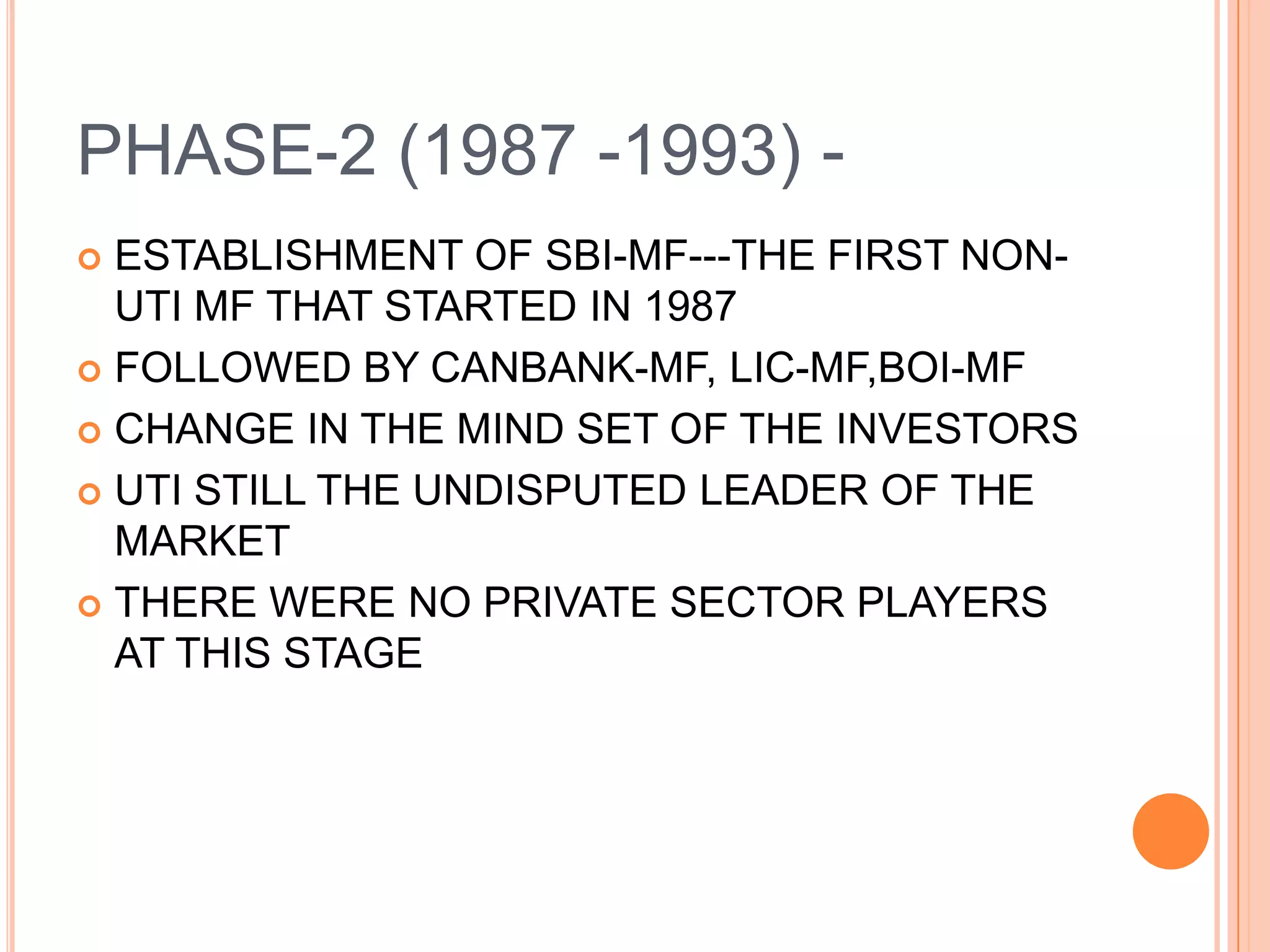

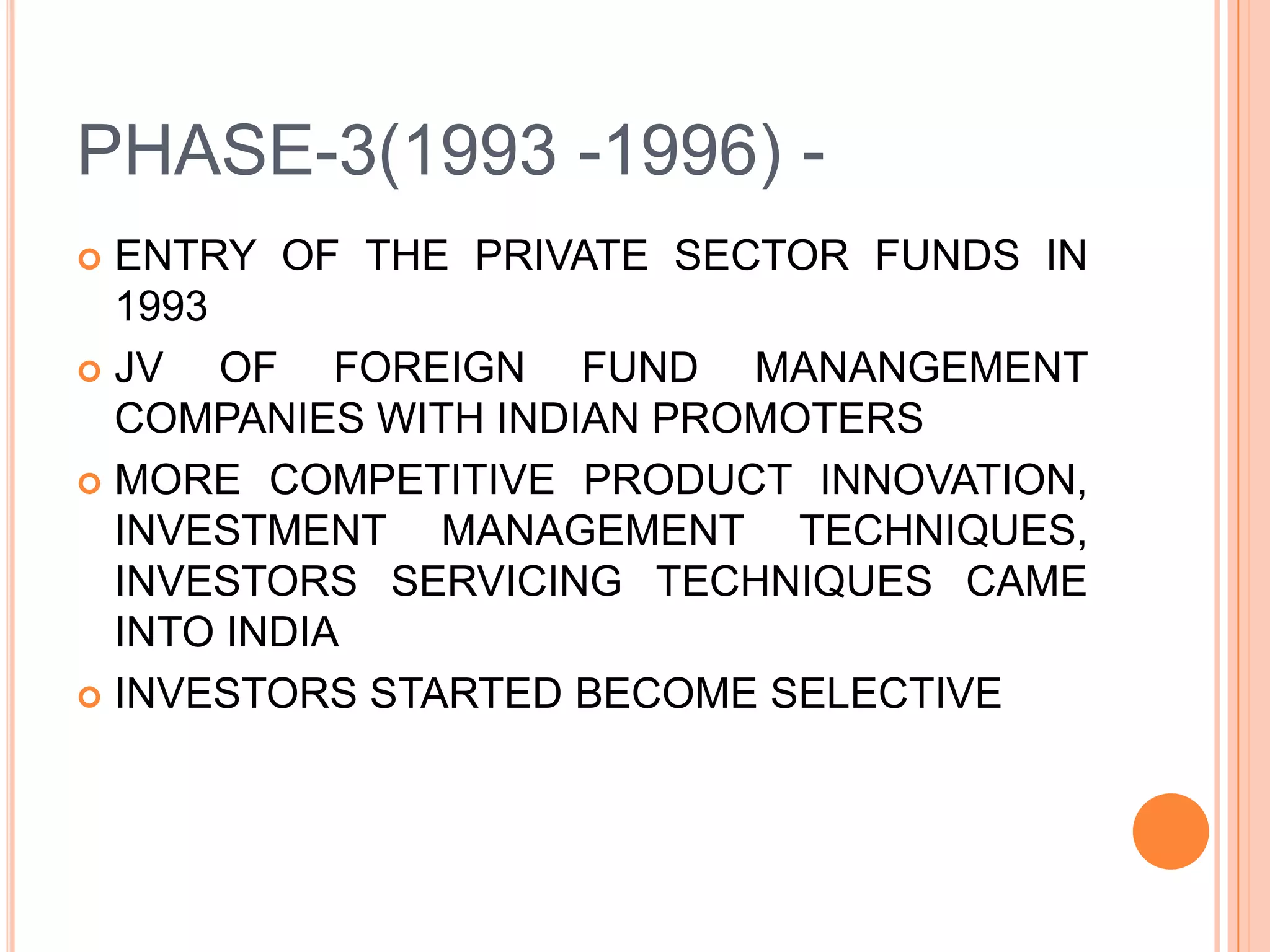

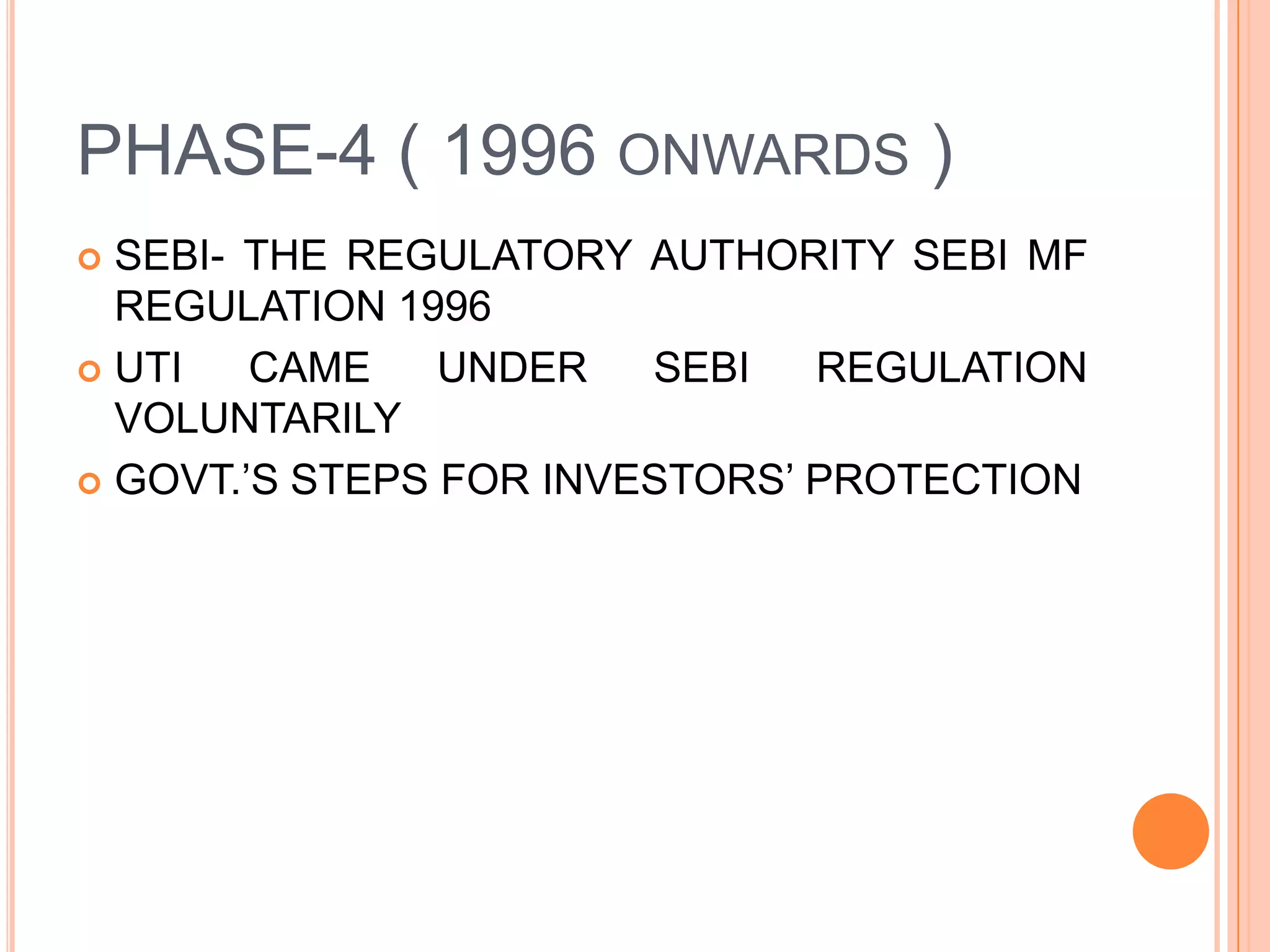

The timeline and phases of mutual fund development in India since 1963 under UTI and SEBI.

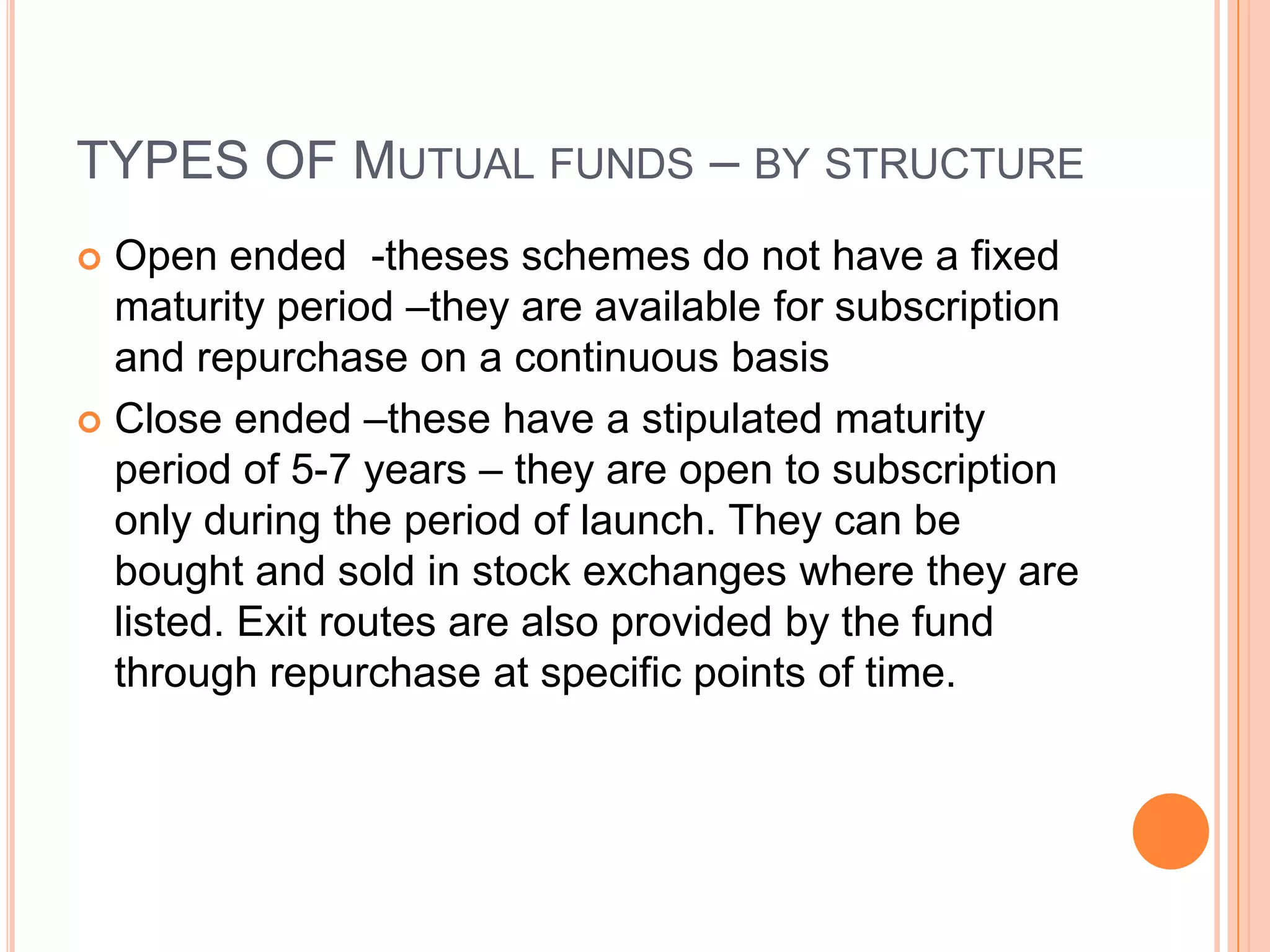

Classification based on structure: Open-ended and closed-ended mutual funds.

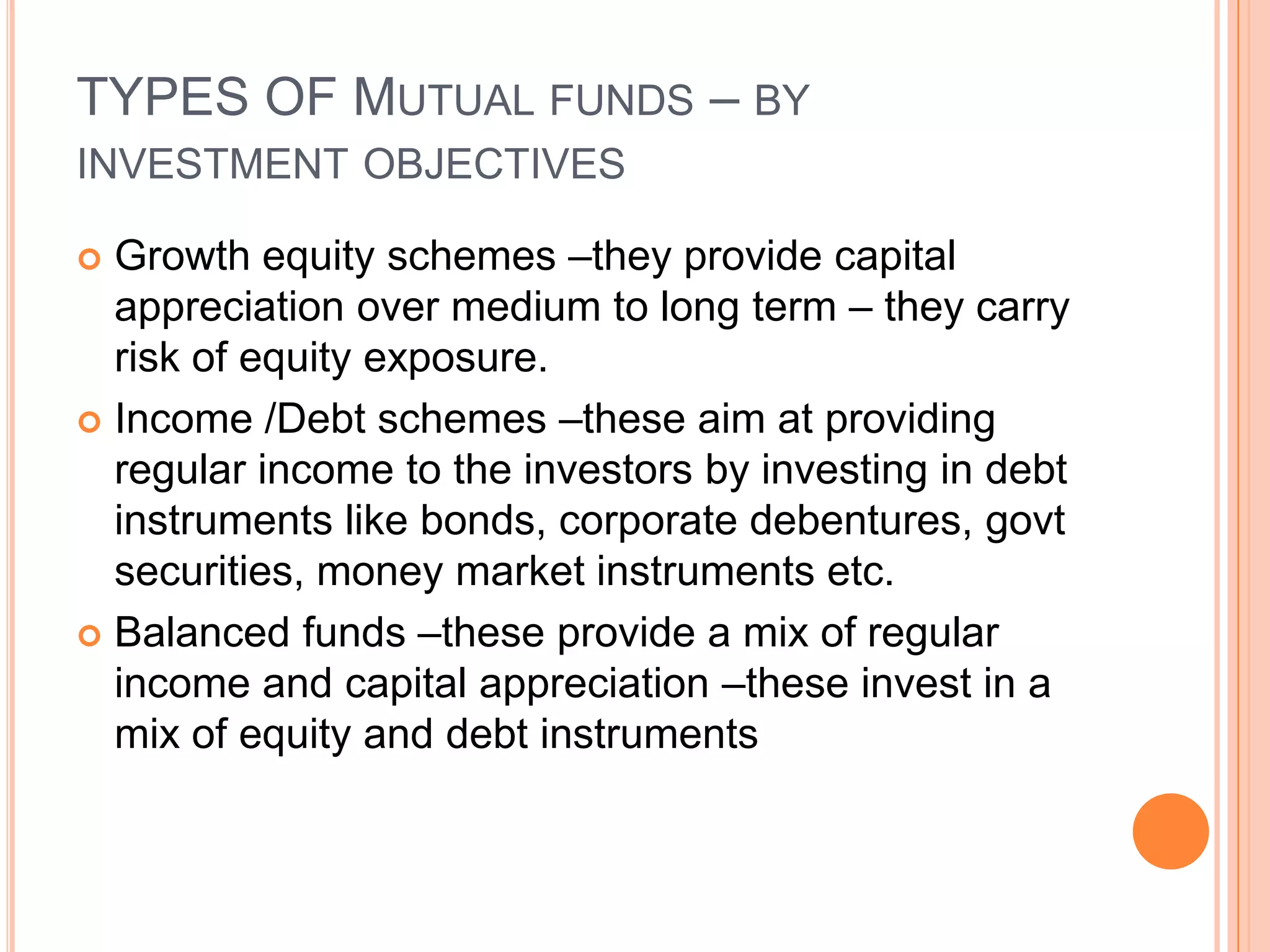

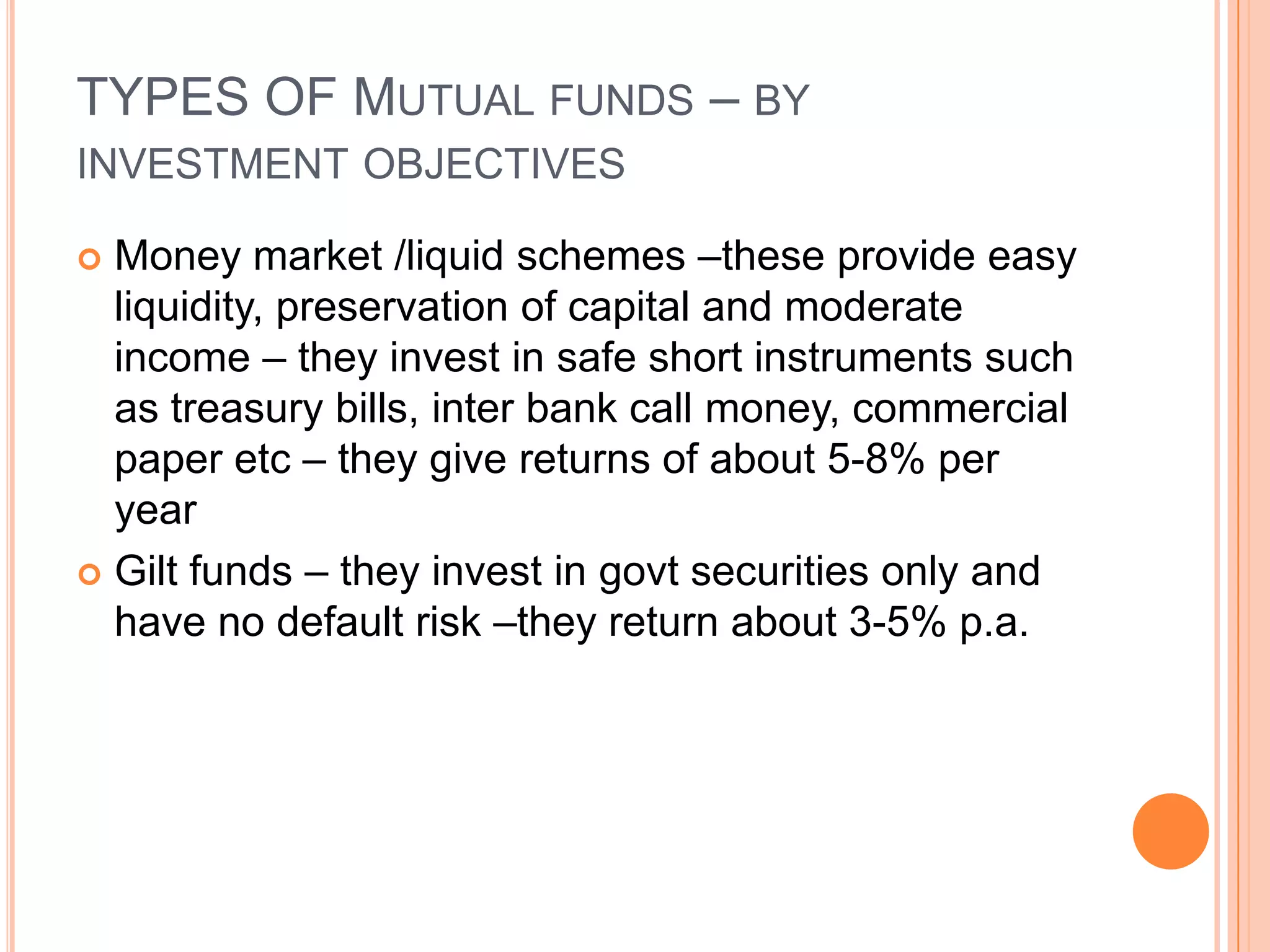

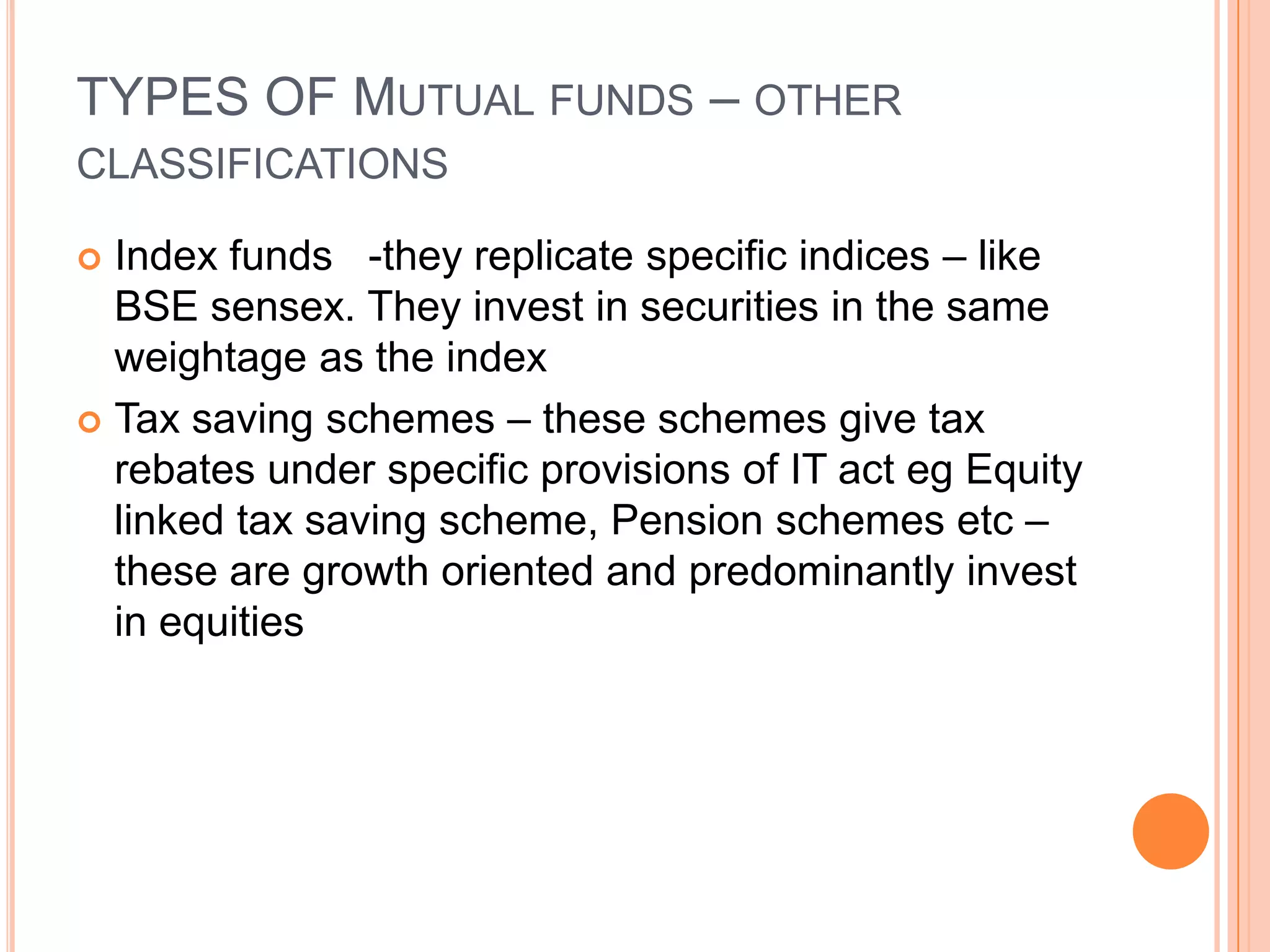

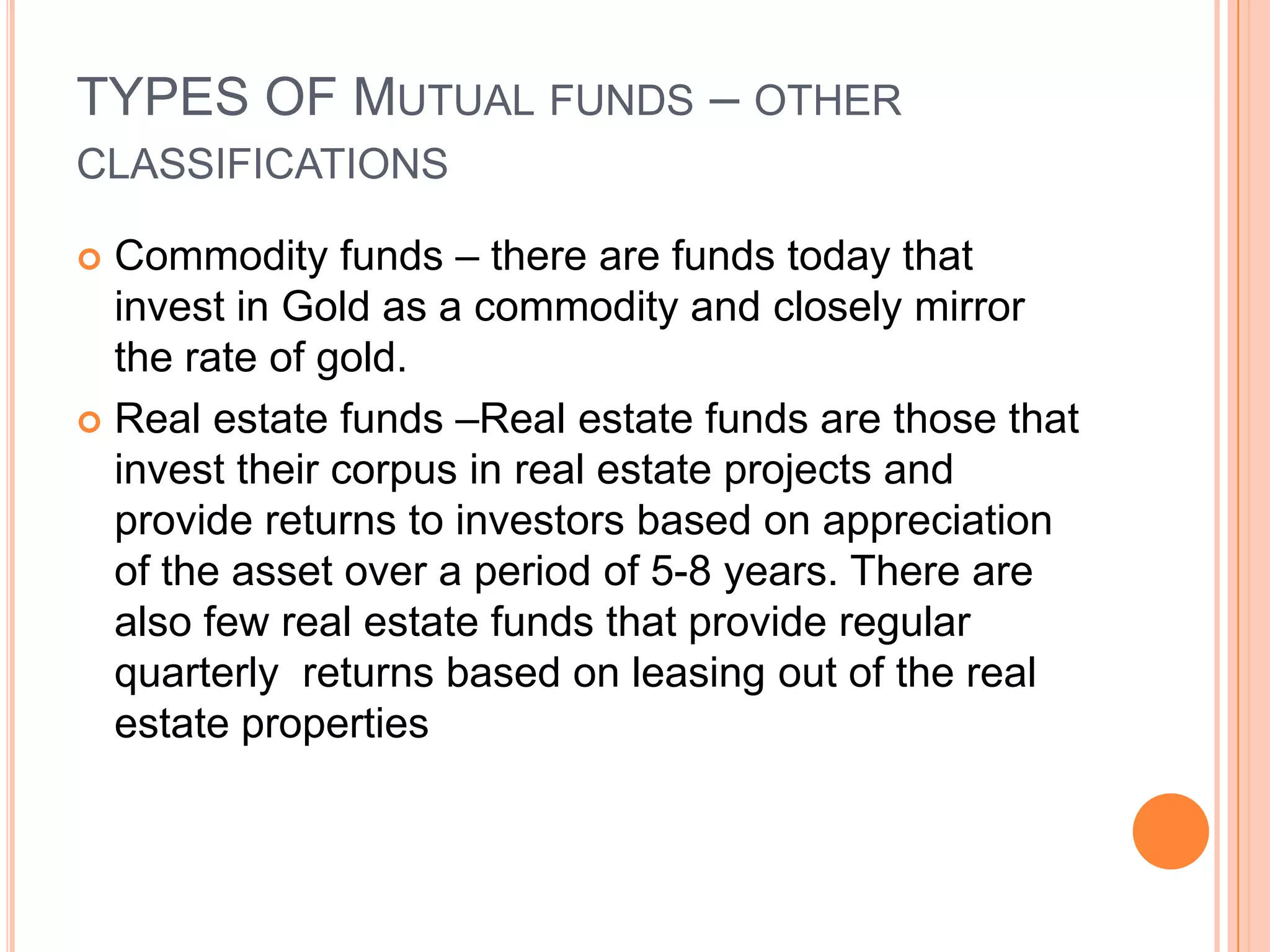

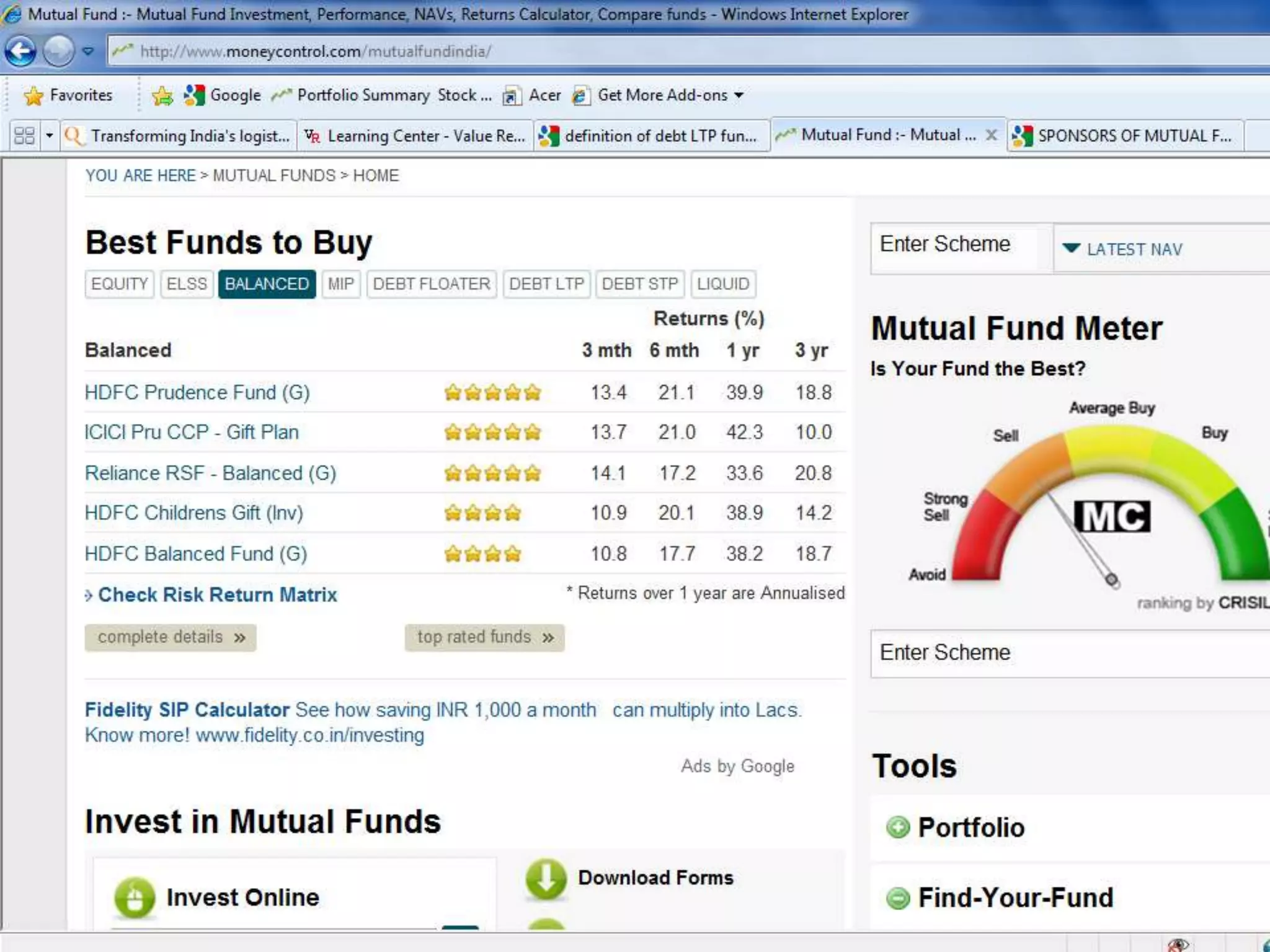

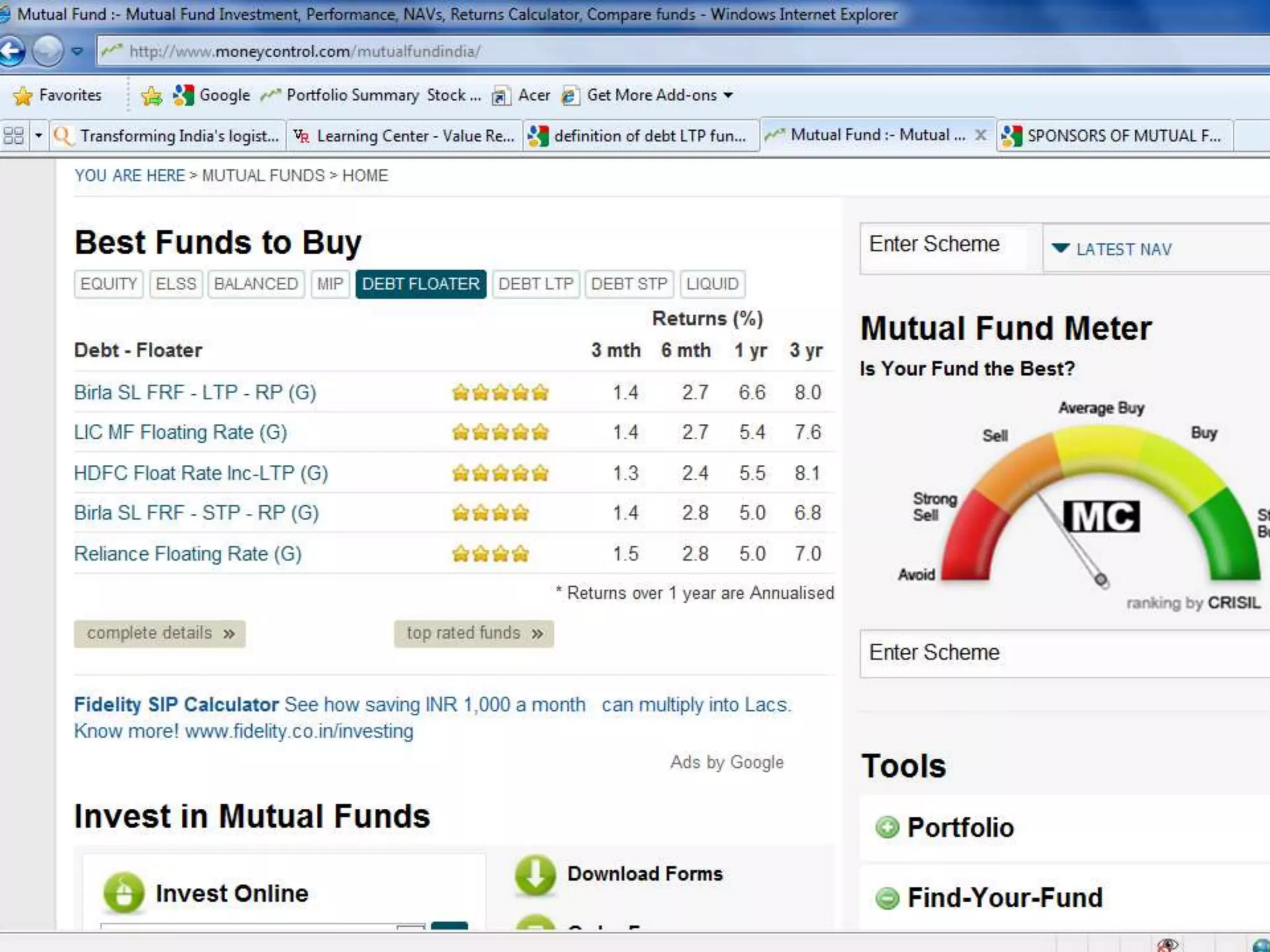

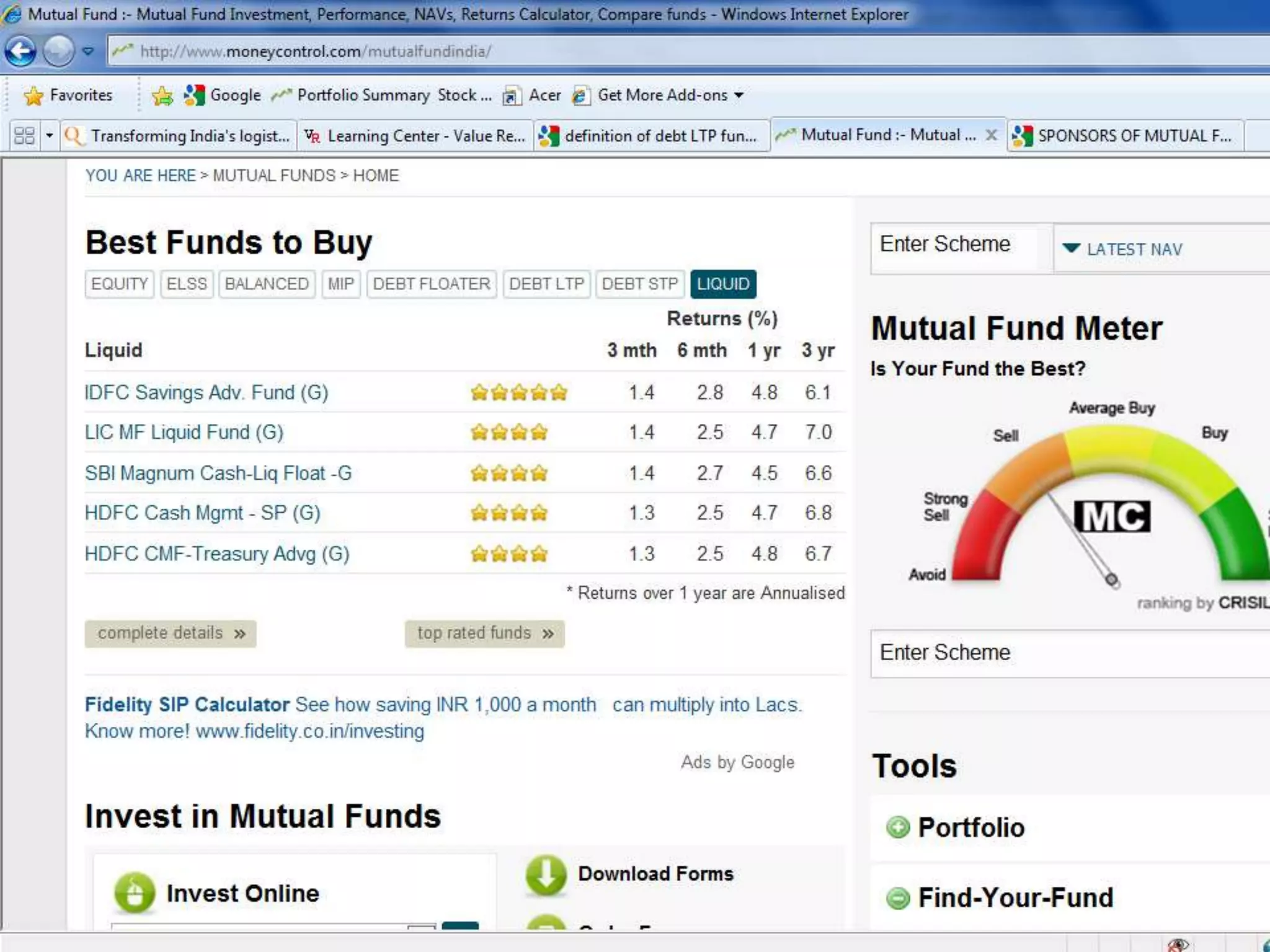

Classification based on goals: Growth, income, balanced, money market, gilt, tax saving, and commodity funds.

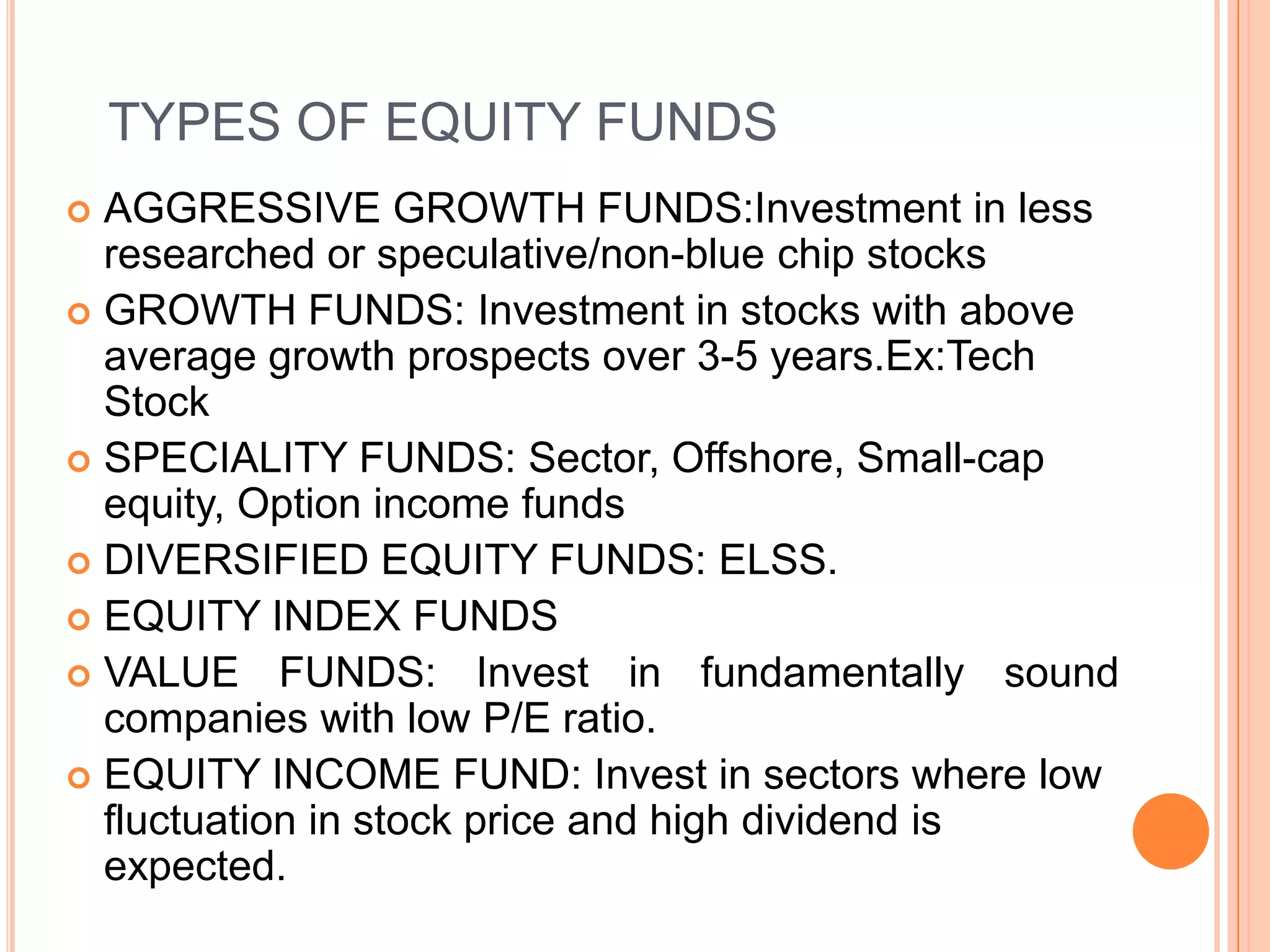

Different equity fund types include aggressive growth, diversified, specialty, value and income funds.

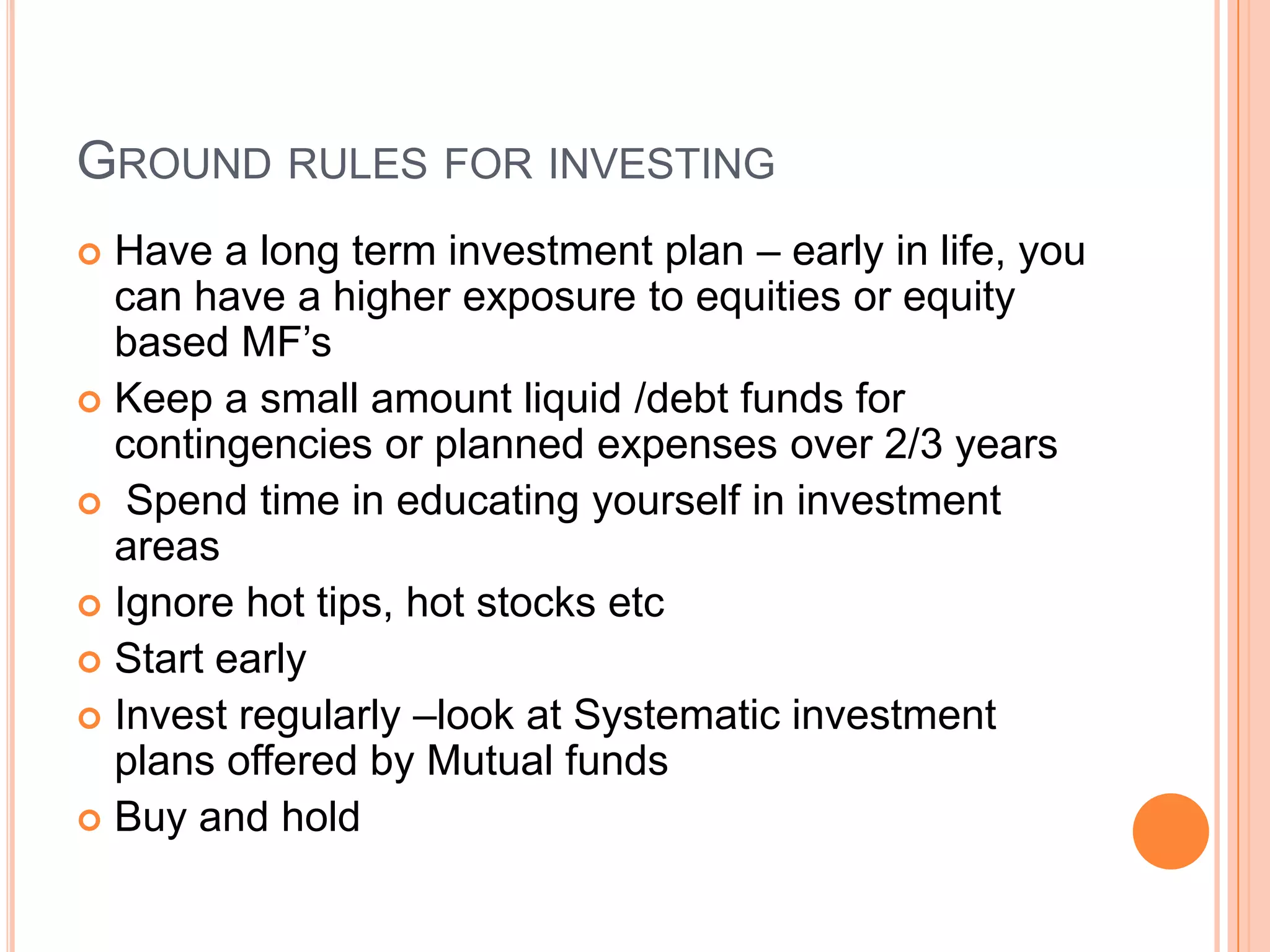

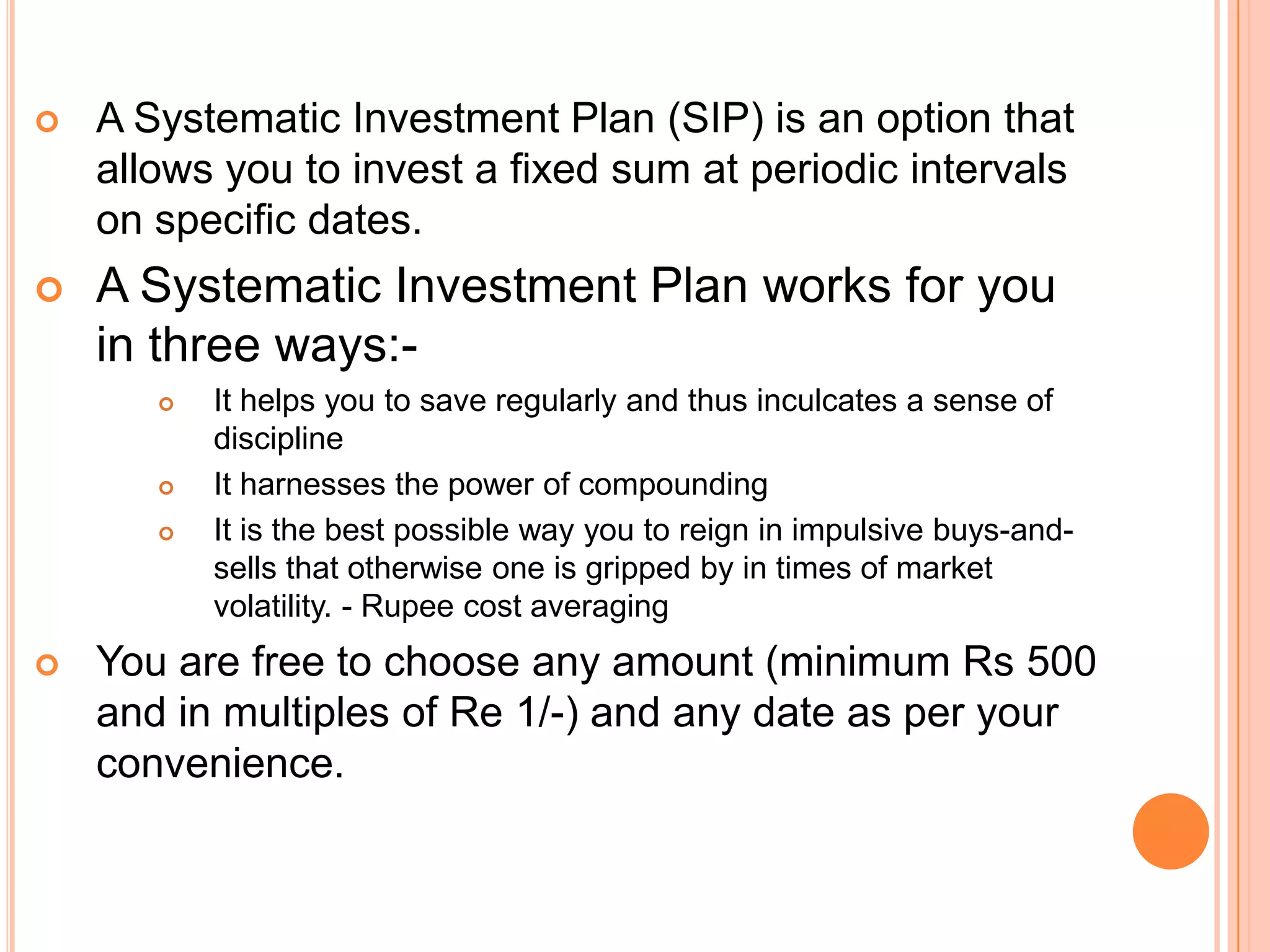

Advice on long-term planning, regular investments, and the benefits of Systematic Investment Plans (SIPs).

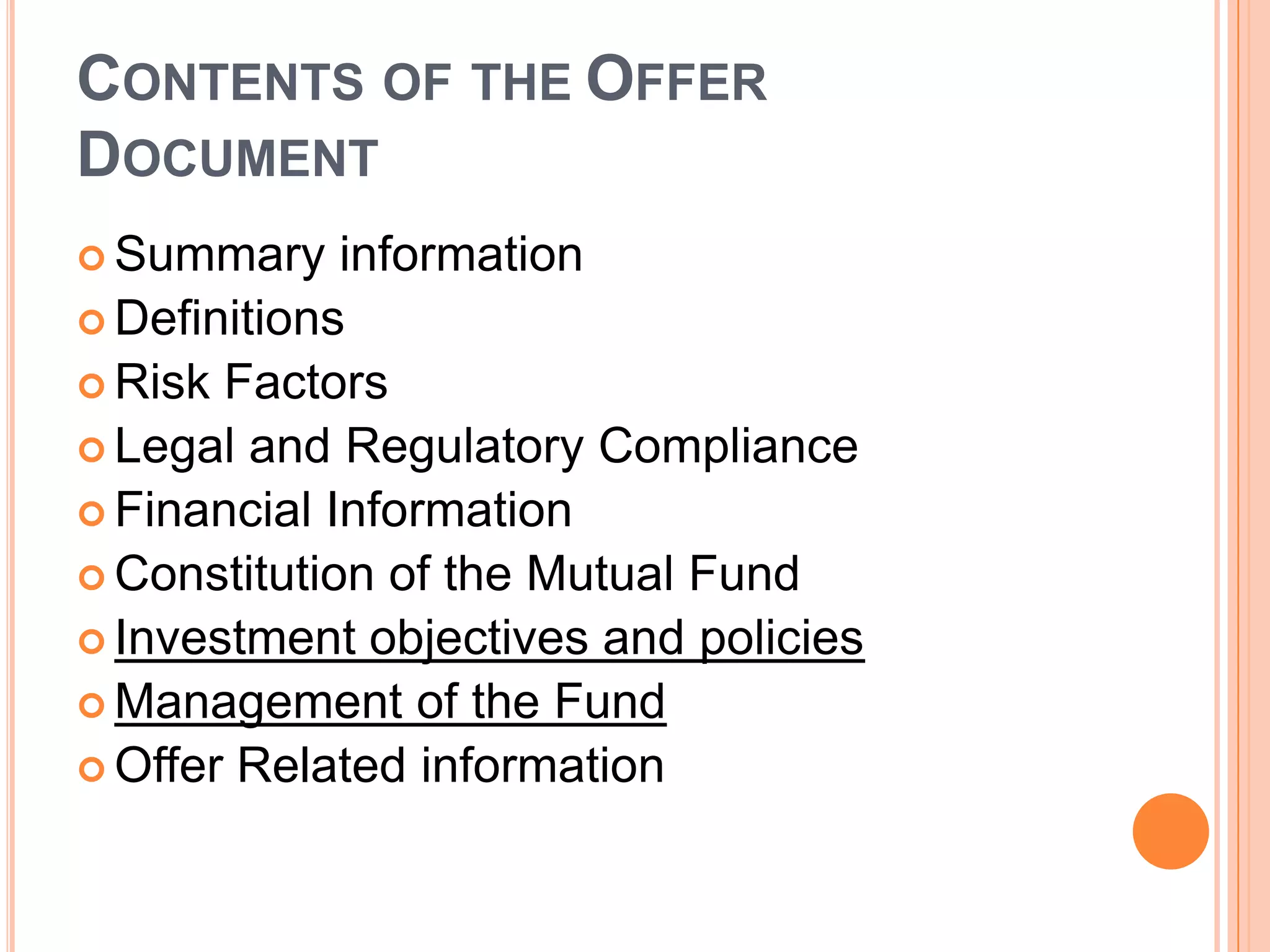

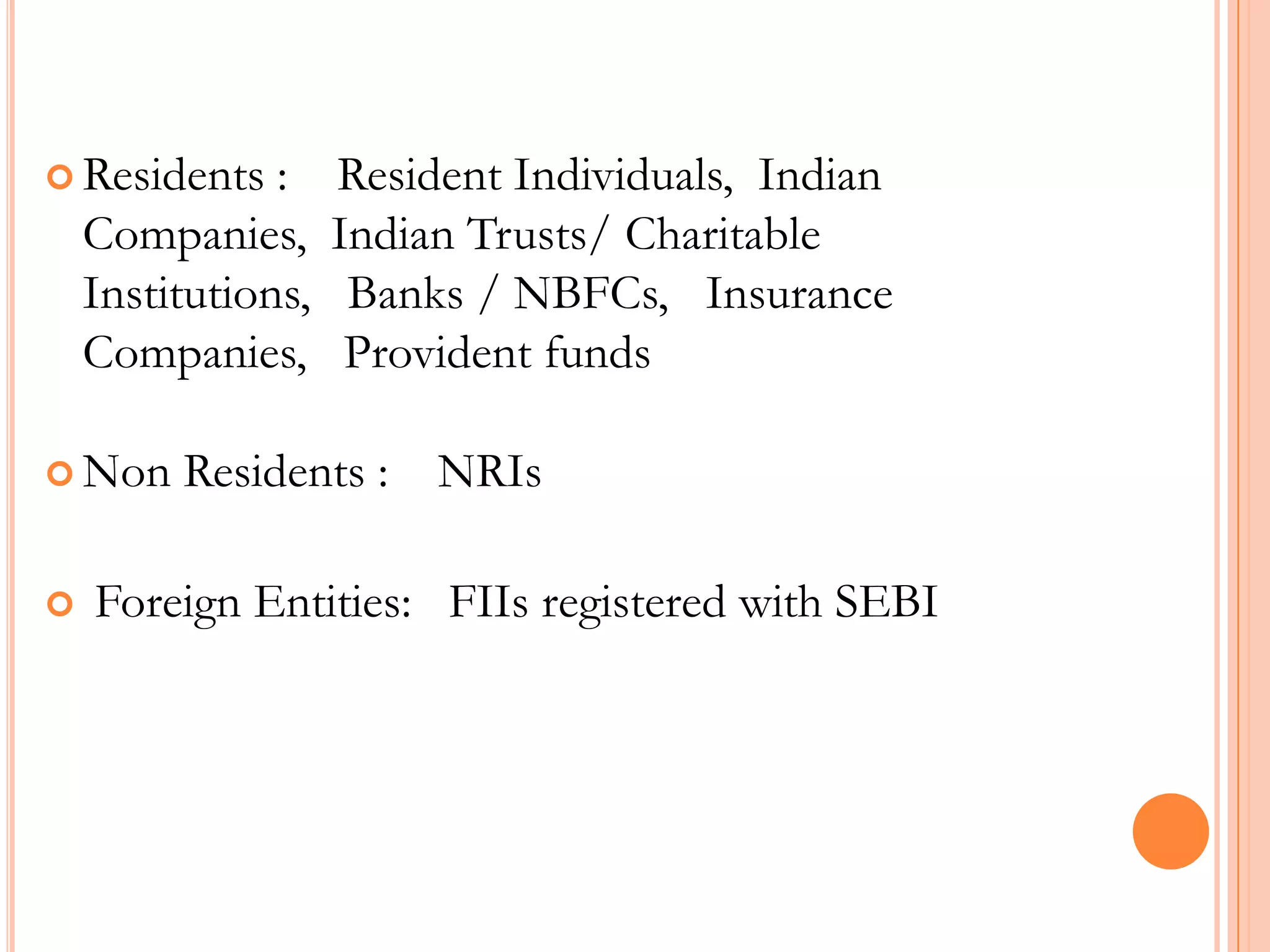

Overview of Offer Document contents and who can invest in mutual funds in India.

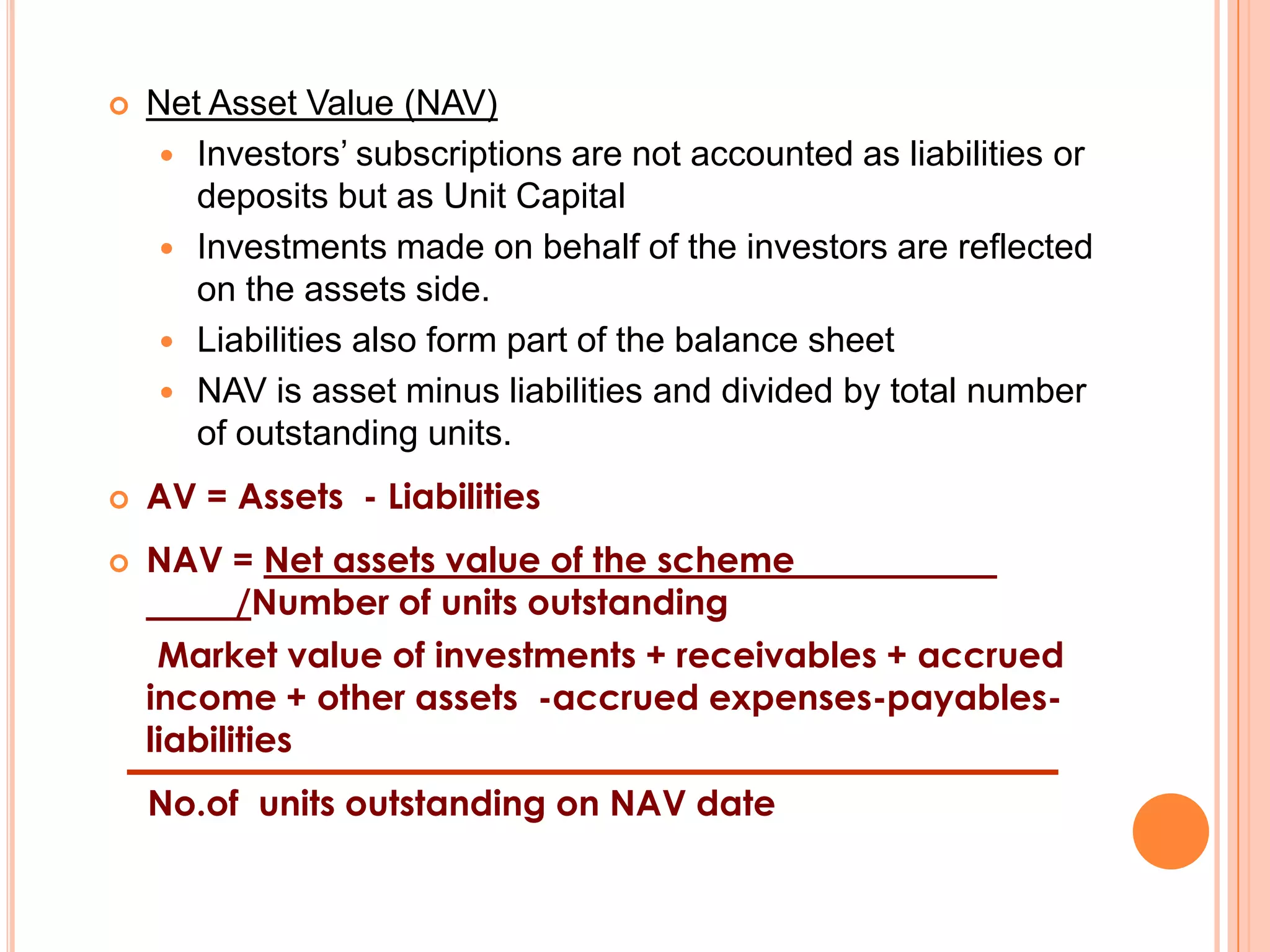

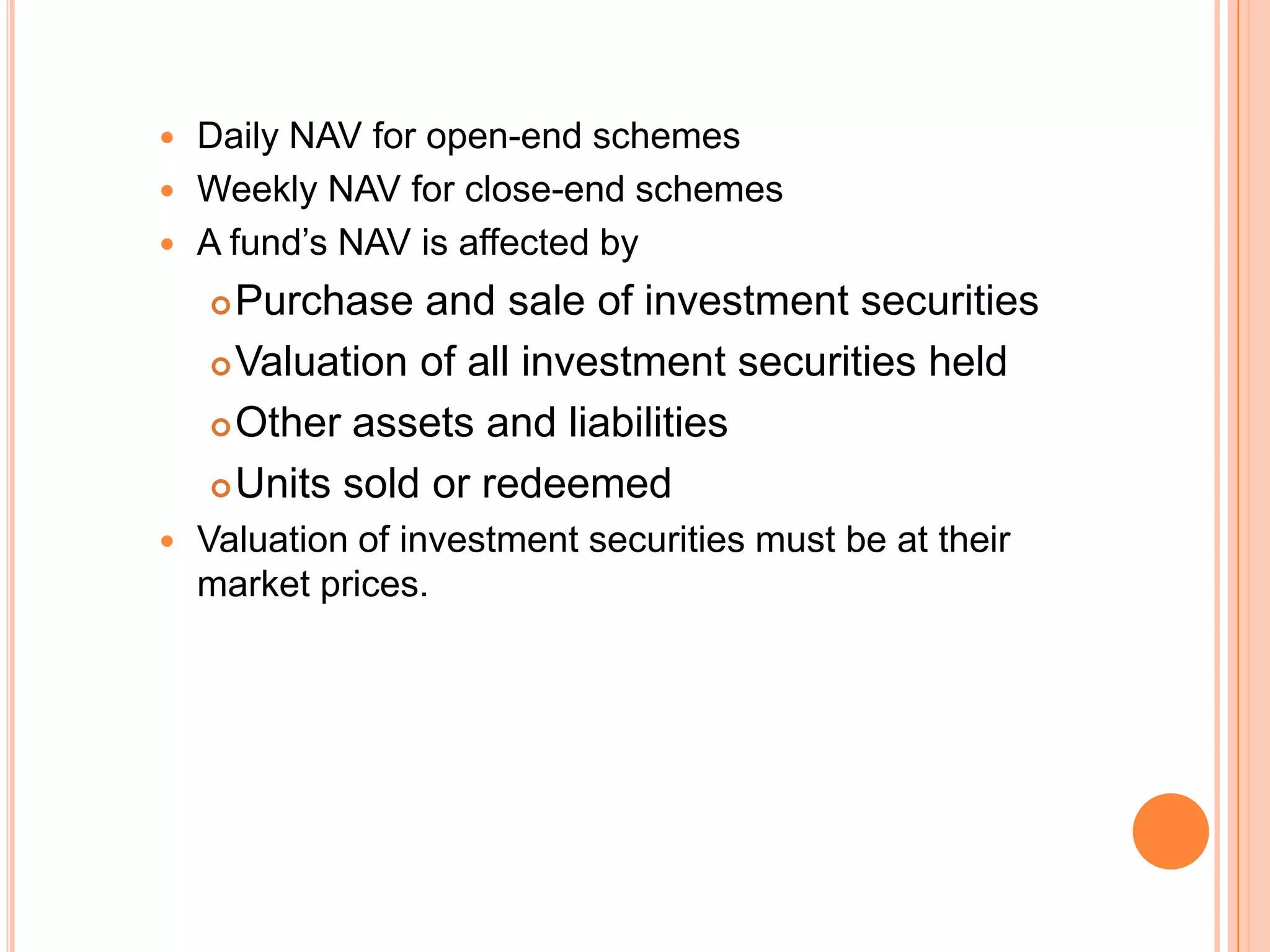

Explanation of Net Asset Value (NAV) calculation and its importance in mutual fund investments.

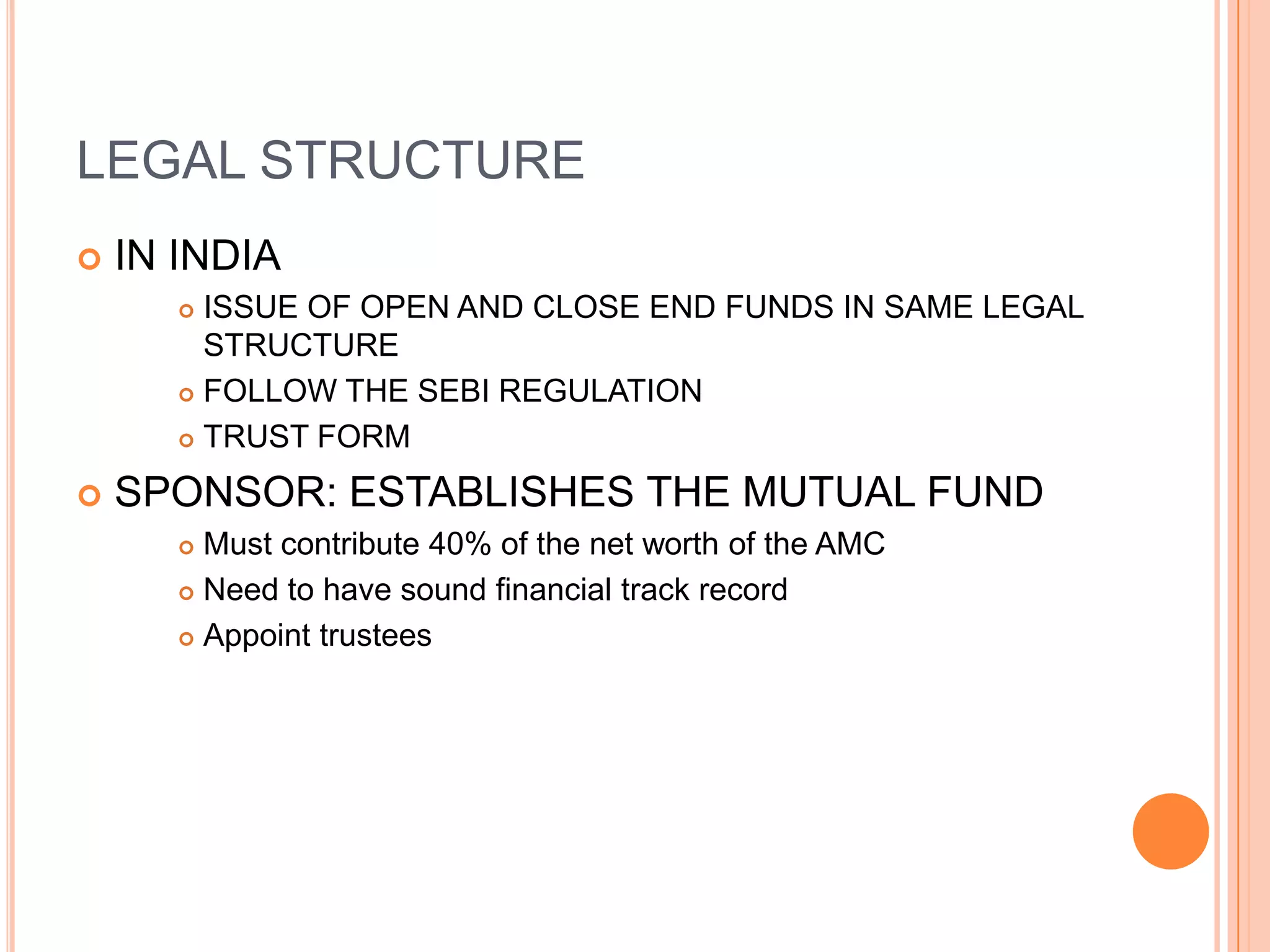

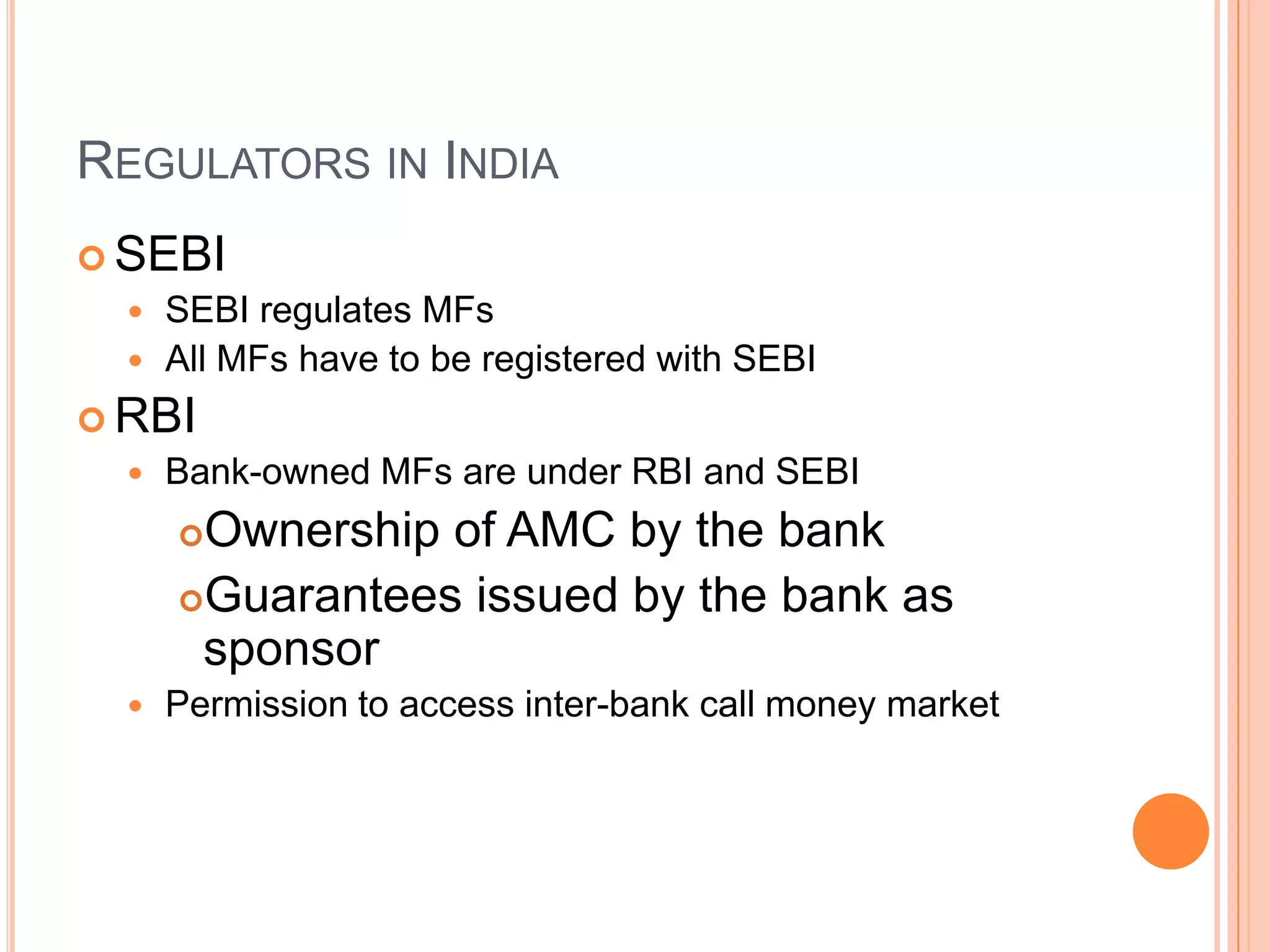

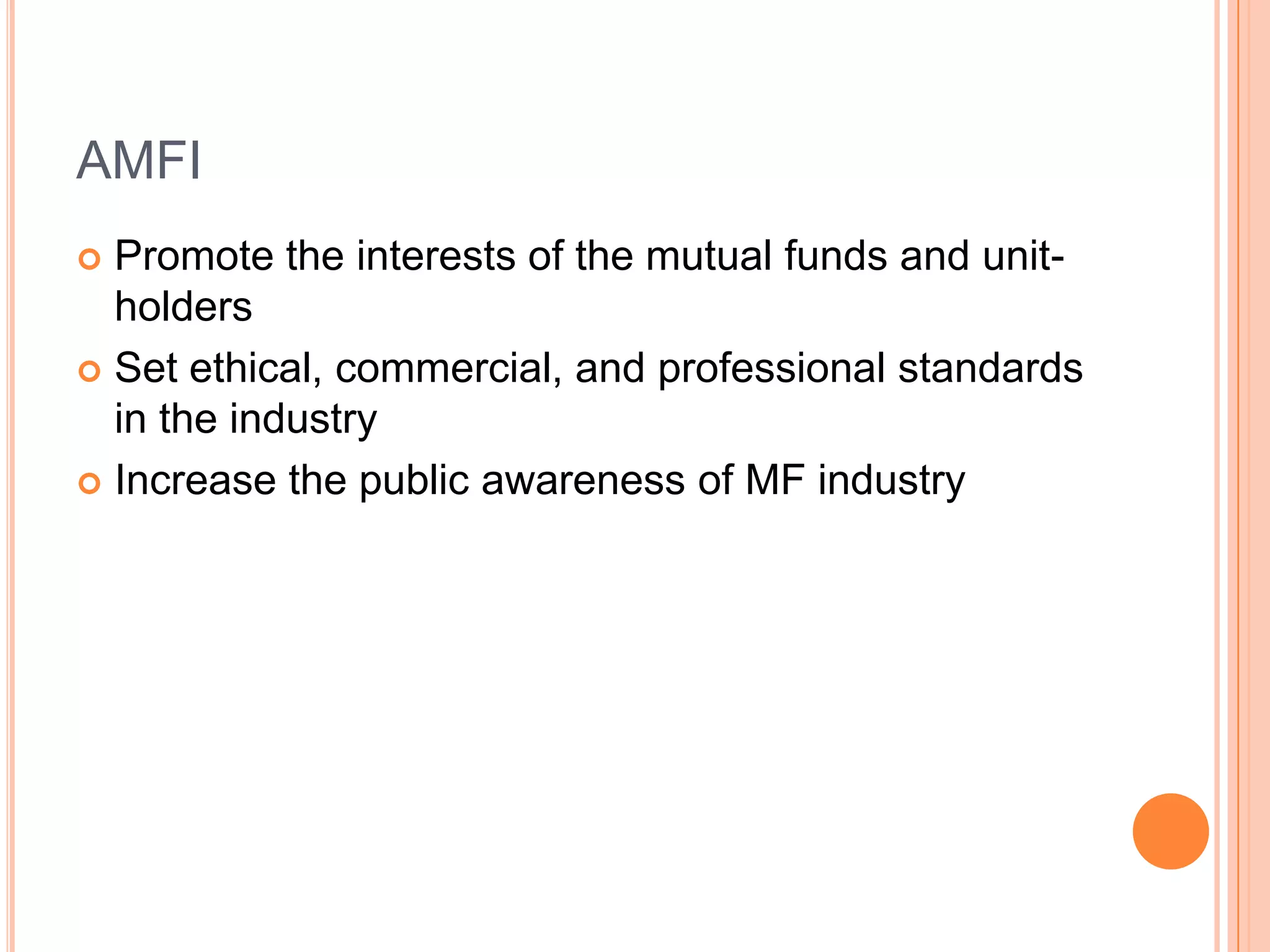

Overview of mutual fund structure, regulatory environment, and the role of SEBI and AMFI in India.

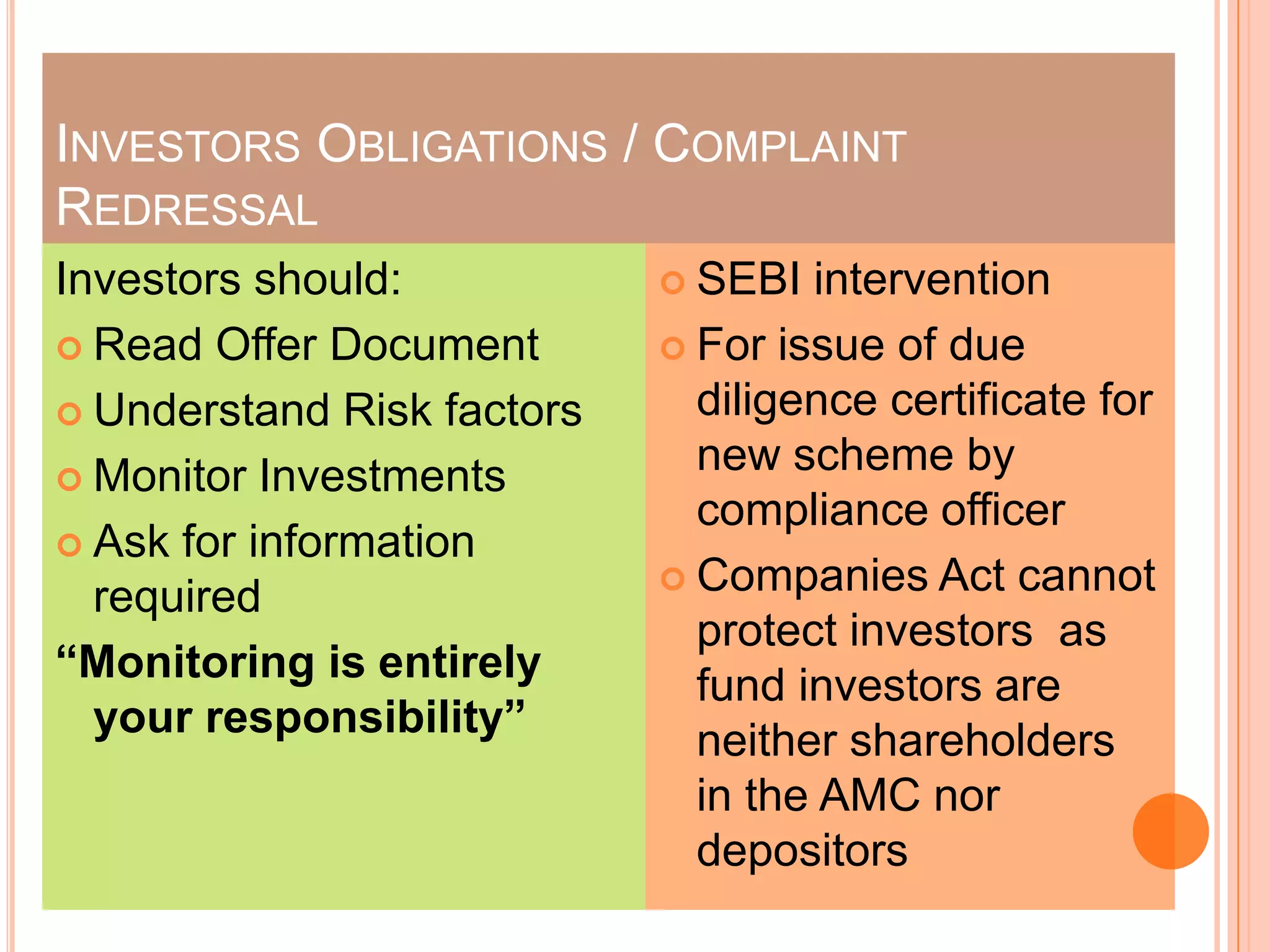

Obligations of investors in monitoring and understanding their mutual fund investments.

Thank you note and conclusion of the presentation.

![Mutual funds[1]](https://cdn.slidesharecdn.com/ss_thumbnails/mutualfunds1-140128115104-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)