Monthly Market Commentary December 2009

•

1 like•318 views

The document provides a monthly market commentary and analysis for December 2009 from MacDougall, MacDougall & Mactier Inc. It summarizes the performance of major stock market indices in November 2009 and year-to-date. It also discusses the impact of the strong Canadian dollar on returns and the economy. Finally, it provides recommendations on several stocks and an outlook on currency movements based on economic fundamentals and commodity prices.

Recommended

More Related Content

What's hot

What's hot (18)

Viewers also liked

Similar to Monthly Market Commentary December 2009

Similar to Monthly Market Commentary December 2009 (20)

More from Christopher R Anderson

More from Christopher R Anderson (20)

Recently uploaded

Recently uploaded (20)

Monthly Market Commentary December 2009

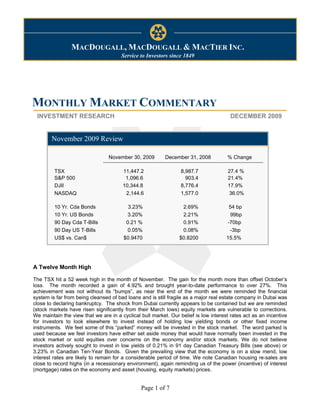

- 1. Monthly Market Commentary December 7, 2009 MACDOUGALL, MACDOUGALL & MACTIER INC. Service to Investors since 1849 MONTHLY MARKET COMMENTARY INVESTMENT RESEARCH DECEMBER 2009 November 2009 Review November 30, 2009 December 31, 2008 % Change TSX 11,447.2 8,987.7 27.4 % S&P 500 1,096.6 903.4 21.4% DJII 10,344.8 8,776.4 17.9% NASDAQ 2,144.6 1,577.0 36.0% 10 Yr. Cda Bonds 3.23% 2.69% 54 bp 10 Yr. US Bonds 3.20% 2.21% 99bp 90 Day Cda T-Bills 0.21 % 0.91% -70bp 90 Day US T-Bills 0.05% 0.08% -3bp US$ vs. Can$ $0.9470 $0.8200 15.5% A Twelve Month High The TSX hit a 52 week high in the month of November. The gain for the month more than offset October’s loss. The month recorded a gain of 4.92% and brought year-to-date performance to over 27%. This achievement was not without its “bumps”, as near the end of the month we were reminded the financial system is far from being cleansed of bad loans and is still fragile as a major real estate company in Dubai was close to declaring bankruptcy. The shock from Dubai currently appears to be contained but we are reminded (stock markets have risen significantly from their March lows) equity markets are vulnerable to corrections. We maintain the view that we are in a cyclical bull market. Our belief is low interest rates act as an incentive for investors to look elsewhere to invest instead of holding low yielding bonds or other fixed income instruments. We feel some of this “parked” money will be invested in the stock market. The word parked is used because we feel investors have either set aside money that would have normally been invested in the stock market or sold equities over concerns on the economy and/or stock markets. We do not believe investors actively sought to invest in low yields of 0.21% in 91 day Canadian Treasury Bills (see above) or 3.23% in Canadian Ten-Year Bonds. Given the prevailing view that the economy is on a slow mend, low interest rates are likely to remain for a considerable period of time. We note Canadian housing re-sales are close to record highs (in a recessionary environment), again reminding us of the power (incentive) of interest (mortgage) rates on the economy and asset (housing, equity markets) prices. Page 1 of 7

- 2. Monthly Market Commentary December 7, 2009 Currency Confusion: Exchange rate movements are having dramatic effects on investor returns and economic prospects. For example, the Dow Jones Industrial Index (U.S. equity index) has enjoyed a return of 18% for the 11 months ended in November but the Canadian dollar has risen by over 15%, leaving a Canadian investor with a much lower return for the year. The high Canadian dollar has also dampened the economic recovery in Canada. We note in the latest economic release in Canada the third quarter gross domestic economy rose 0.4% for the quarter, but a major drag on growth was from the trade sector. This is illustrated below in the graph on the left side. All components contributed to the growth in Canada with the exception of imports. The high Canadian dollar has encouraged the importation of various goods and services and lessened the appeal of Canadian made goods, though exports did grow. The importation of goods has the effect of raising the Gross Domestic Product of the country from which we import from while exports raise our Gross Domestic Product. For the third quarter, Canadians imported goods worth $94.2 billion, while only exporting $90.3 billion. Source: Statistics Canada The effect of the high Canadian dollar can also be seen on the current account balance Canada runs with the rest of the world. The current account is the difference in net exports (exports less imports) and net cash receipts (cash payments to the rest of the world less cash payments from the rest of the world). From a cash flow point of view the current account shows more money is leaving the country than coming in. The third quarter continued the trend from the previous three quarters. As the above right graph illustrates, Canada has, in recent years, run a surplus with the rest of the world. Starting in the fourth quarter of 2008 this surplus became a deficit and for the nine months of 2009 the deficit was at a record level of $13.1 billion predominately due to net exports turning negative. Predicting Currency Movements: We reviewed the literature on currency movements to see if there are critical variables one can use to predict where currencies trade versus each other. Economic differences (such as inflation, trade balance, budget surplus/deficits) between countries have long been considered critical determinants of a currency’s value. This complex issue has been extensively studied in economic literature. Still, there are no definitive answers. No single approach provides a satisfactory explanation of exchange rate movements, particularly short and medium term. Nevertheless, we feature two approaches to predicting currency movements which are used for forecasting purposes. The first approach has been broadly used and normally taught in economics 101 classes, while the latter one is a relatively new concept. Page 2 of 7

- 3. Monthly Market Commentary December 7, 2009 1) The Purchasing Power Parity (PPP) approach. This concept follows from the law of one price. This thesis holds that in a competitive market, exchange rates will adjust to equalize the relative purchasing power of currencies. Identical goods should sell for the same price once adjusted for currency. For example, an identical car should sell for the same price regardless of the country in which it is sold adjusted for a country’s currency. In theory if a car is sold for $25,000 in one country the identical car should sell for the same amount in another country. In the case of the U.S., if a car was priced at US$25,000 then in Canada it should be priced at $26,250 (the month end exchange rate between Canada and the U.S. is $1.05 Canadian per U.S.). In theory, should these prices not equilibrate, entrepreneurs would have the incentive to buy autos in the cheaper location and sell them into the higher price location until the prices match adjusted for currency. In a more light-hearted approach, the magazine The Economist publishes the local prices of McDonald’s (MCD-NYSE) restaurant item the Big Mac around the world and computes the Big Mac PPP. The magazine then publishes the “fair value” of the currency to equalize the price paid by a U.S. consumer. Below we illustrate the Big Mac PPP using the price of Big Macs around the world as at July 2009 and using November 2009 month-end exchange rates. The Hamburger Standard The Hamburger Standard $6.00 45.0% $4.00 0.0% 40.0% $3.50 -10.0% $5.00 $3.00 35.0% Big Mac at Current $2.50 -20.0% $4.00 30.0% Big Mac at Current Exchange Rate Exchange Rate $2.00 -30.0% 25.0% Under-Valuation $3.00 $1.50 -40.0% 20.0% Over-Valuation $1.00 $2.00 15.0% $0.50 -50.0% 10.0% $0.00 -60.0% $1.00 5.0% ina A Ru d ia ala a T h ia $0.00 0.0% an US si ss ys Ch ne ail do USA Canada U.K. Euro Japan M In The Hamburger Standard $8.00 120.0% $7.00 100.0% $6.00 Big Mac at Current $5.00 80.0% Exchange Rate $4.00 60.0% $3.00 Over-Valuation 40.0% $2.00 $1.00 20.0% $0.00 0.0% nd ay k en A ar la S w ed m U or er en w itz N S D w S We use the price of a Big Mac in the U.S. and Europe. In Europe, the Big Mac sells for 3.31 Euros. Using the November month-end closing price of the U.S. dollar and Euro of US$1.51 per Euro the Big Mac should sell for $5.00 ($3.31 multiplied by 1.51). The price in the U.S. is $3.57. This implies an overvaluation of the Euro of some 40%. Page 3 of 7

- 4. Monthly Market Commentary December 7, 2009 We find it difficult to believe some of the currencies are so over/undervalued using this approach. Is the Euro, Norway and Switzerland that much over-valued? One can see the limitation of this approach as it assumes goods are freely tradable; there are no transportation charges or cultural differences. 2) Fundamental Equilibrium Exchange Rates (FEER): This concept has been recently advocated by an organization called The Peterson Institute of International Economics (www.petersoninstitute.org). The basic premise to arrive at the fair value of a currency is the exchange rate at which a country would not increase its foreign indebtedness as a percentage of its Gross Domestic Product. We illustrate their estimate of the fair value (FEER) of various currencies relative to the U.S. dollar in the table below. We show the exchange rate at the end of March 2009, this month’s closing exchange rate and the necessary currency adjustment from November’s close to reach their calculated fair value. Using the two measures (PPP and FEER) shows that many of the Asian countries (China, Malaysia and Thailand) have undervalued currencies. We also note the large currency adjustment made since March. The Canadian dollar is but one currency whose adjustment has been rapid and appears slightly over- valued in both approaches. 3) There is an argument each country has its particular nuances and that a generalized model is not applicable. The graph on the following page highlights the relationship between the Canadian/U.S. dollar and commodity prices. The three commodities used in this forecast are gold, natural gas and oil. As these three commodities have moved up in price, the Canadian dollar has also moved up. We note the forecast ($0.956) is above the current spot price ($0.9406) of the Canadian dollar. Page 4 of 7

- 5. Monthly Market Commentary December 7, 2009 Source: Dundee Wealth Economics. Ian Nakamoto Director of Research Recommended Stocks: Agrium Inc.(AGU-TSX) Telus Corporation (T-TSX) iShares MSCI All Country Asia ex-Japan (AAXJ-NASDAQ) Absolute Software Corporation (ABT-TSX) The Royal Bank of Canada (RY-TSX) Bombardier Inc. (BBD.B-TSX) Metro Inc. Page 5 of 7

- 6. Monthly Market Commentary December 7, 2009 Important Disclosures Company Ticker Disclosures McDonalds Corporation MCD-NYSE - Agrium Inc. AGU-TSX 1 Telus Corporation T-TSX - iShares MSCI All Country Asia ex-Japan AAXJ-NASDAQ - Absolute Software Corporation ABT-TSX - The Royal Bank of Canada RY-TSX - Bombardier Inc. BBD.B-TSX - The research analyst (s) who authored this report certify that the views expressed therein accurately reflect their personal views and that no part of the analyst’s compensation will be related to those views. Conflict of Interest Policy for Analysts 1. Refers to share ownership of the company in question by the Analyst. In the disclaimer section of a report, the number 1 will indicate that the analyst or a member of the analyst’s family has any position (equity, derivative or other) in the shares in question. 2. Refers to share ownership of the company in question by the Director of Research or Supervisory Analyst. In the disclaimer section of a report, the number 2 will appear if the Director of Research or Supervisory Analyst has a position (equity, derivative or other) in the shares in question. 3. Refers to any relationship the Analyst, a member of the family thereof, or firm has with the company in question. A relationship includes anything except the simple trading of stock for the company. In the disclaimer section of a report, the number 3 will appear if the analyst, a family member thereof or the firm has a relationship with the company in question. 4. Refers to whether Analysts have visited facilities and/or key operations of the company. 5. Refers to whether the company in question defrayed any of the costs of traveling to see the company in question’s facilities. In the disclaimer section of the report, the number 5 will appear if the company has paid any portion of the analyst’s travel expenses related to viewing facilities. 6. Refers to MacDougall, MacDougall & MacTier Inc. having undertaken any underwriting business from the company in question. If, in the previous 18 months, MacDougall, MacDougall & MacTier Inc. has acted as an underwriter to the company in question, it will be included in the disclaimer section of a report with footnote number 6. 7. Collective ownership by 3Macs and its affiliates of 1% or more of any class of the issuer’s equity shares for a period of 60 days preceding the issuance of the report. Definition of Equity Research Ratings & Risk Ratings Equity Research Ratings The rating system for recommendations on research reports published by MacDougall, MacDougall & MacTier Inc. will be as follows: BUY - will represent opportunities that potentially offer in excess of a 20% return on investment within a 12-18 month period. HOLD - will represent opportunities that offer between 5% and 20% potential return on investment within a 12-18 month period. SELL- will represent opportunities that offer less than 5% return on investment within a 12-18 month period. Risk Ratings MacDougall, MacDougall & MacTier Inc. employs two risk ratings with its research reports; Above Market Risk and Market Risk. Above Market Risk denotes a company, which operates in an inherently speculative industry, or one that is more volatile than the market as measured by its beta. Above Market Risk may also indicate weakness in the company’s balance sheet, low debt ratings, and the lack of a dividend, low liquidity or other deficiencies. Market Risk denotes a company, which is expected to present, on average, the volatility present with the overall market, measured by its beta. Market Risk companies will generally have sound balance sheets, will be established, large cap companies in industries generally regarded as stable and for the most part will pay a dividend. MacDougall, MacDougall & MacTier Inc. Equity Research Ratings Distribution 100 90 80 70 60 50 40 30 20 10 0 BUY HOLD SELL ■ Percentage of companies covered by MacDougall, MacDougall & MacTier Inc. Equity Research within each rating category. Page 6 of 7

- 7. Monthly Market Commentary December 7, 2009 Glossary of Terms: EPS Earnings per Share P/E Price to Earnings Ratio EBITDA Earnings before Interest, Taxes, Depreciation and Amortization Market Cap Total Shares Outstanding multiplied by Shares Price Enterprise Value Fully Diluted Shares Outstanding PEG P/E Multiple Divided by Growth Rate ADR American Depository Receipt WACC Weighted Average Cost of Capital Risk Free Rate 10 Year Treasury bond Yield Dividend divided by Share Price ASP Average Price DSOs Days Sales Outstanding Capex Capital Expenditures CPU Cost per Unit EVA Economic value Added EV / EBITDA Enterprise Value / Earnings before Interest, Taxes, Depreciation and Amortization DCF Discounted Cash Flow Holts DCF Holts Discounted Cash Flow DYT Dividend Yield Target Yield Yield BSOPM Black Scholes Options Pricing Model BETA Quantitative measure of the volatility of a stock, mutual fund, or portfolio, relative to the overall market MF Mutual Fund This research report has been prepared and circulated for general information only. It does not account for the specific investment objectives and financial situation of any person receiving this report. Investors should seek professional advice regarding the appropriateness of investing in any securities discussed or recommended in this report and should recognize that statements regarding future prospects may not be realized. This report is not to be construed as an offer to sell or as a solicitation for an offer to buy any securities. The information presented in this report has been compiled from sources believed to be reliable but no guarantee is made as to its accuracy, completeness, or correctness. All opinions and estimates contained in this report are provided in good faith and are subject to change without notice. Montreal 514-394-3000 Quebec 418-656-1212 Toronto 416-597-7900 London 519-645-1110 Page 7 of 7