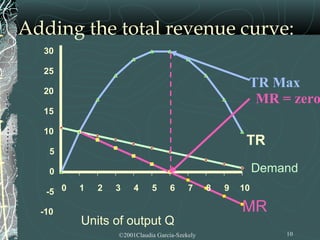

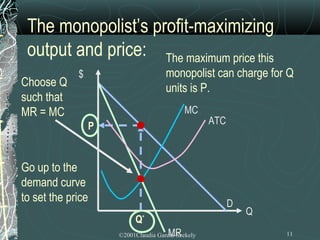

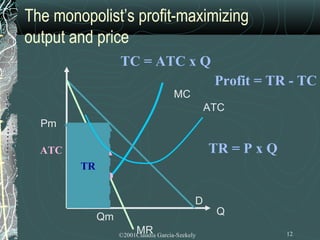

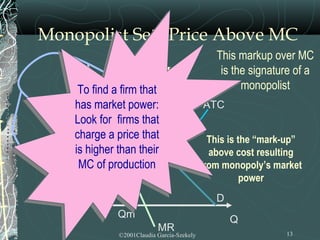

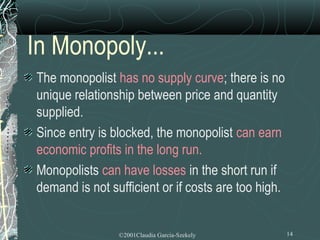

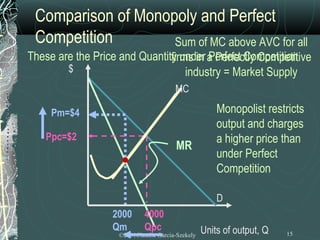

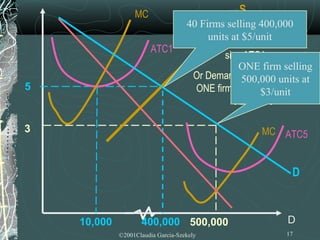

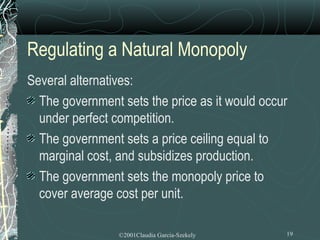

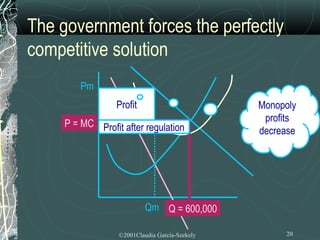

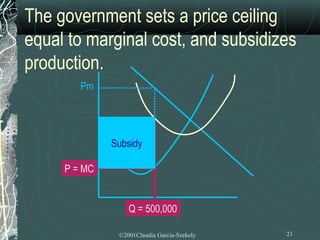

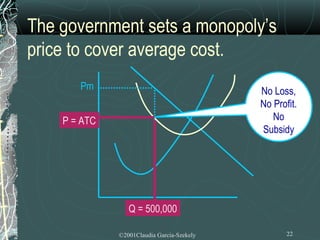

This document discusses different market structures including imperfect competition, monopoly, and perfect competition. It provides details on pure monopoly, including how a monopolist determines price and output by setting marginal revenue equal to marginal cost. The document also discusses barriers to entry for monopolies and natural monopolies where large-scale production allows for lower costs. Government regulation of natural monopolies is also mentioned.