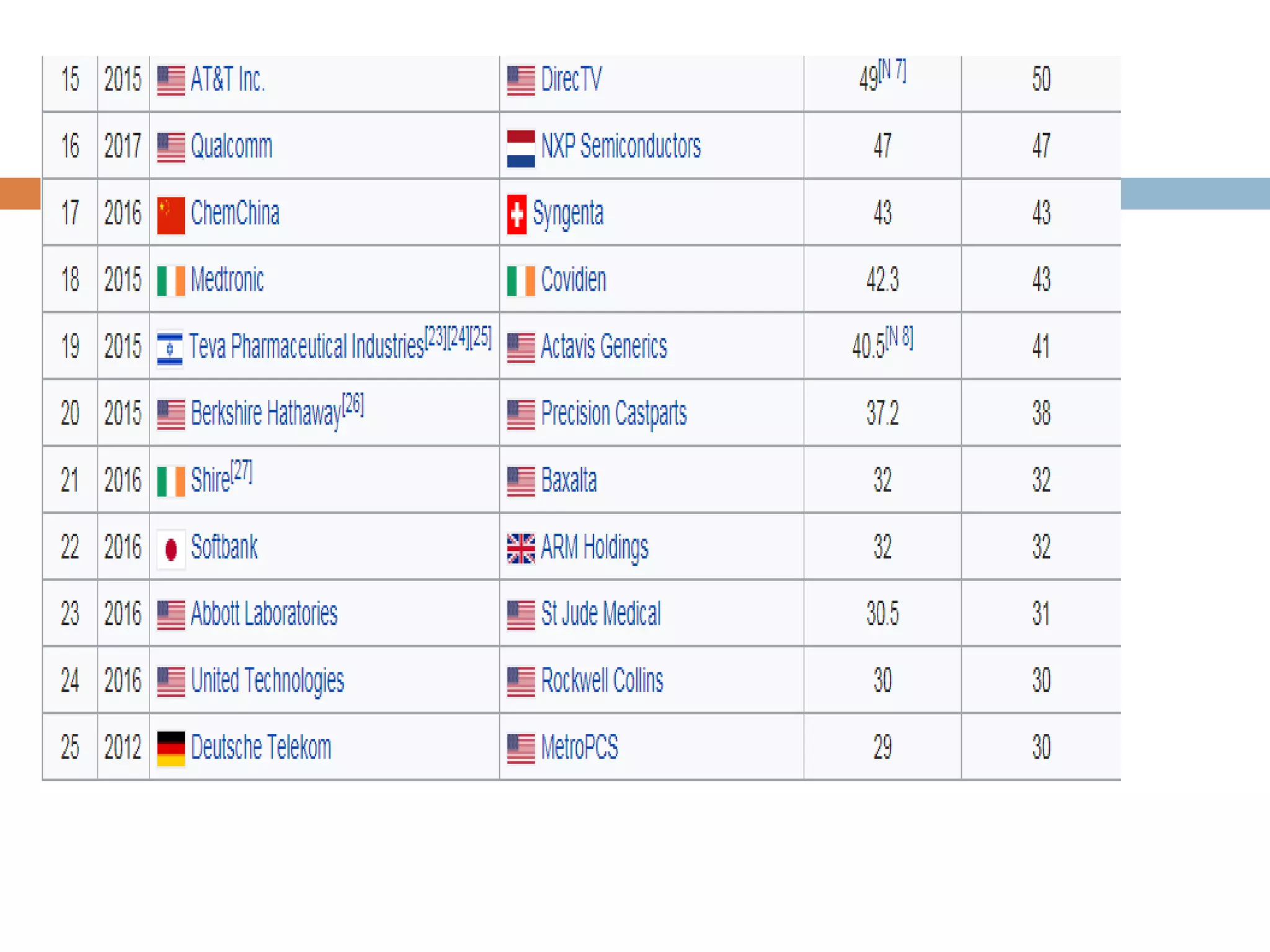

Kotak Mahindra Bank announced a merger with ING Vysya Bank in 2014 worth $2.4 billion. The merger provided synergies like increasing Kotak's branch network by 47% and ATMs by 35%, improving its geographic presence across India. However, integrating ING Vysya's unionized employees and different pay structures into Kotak posed human resource challenges. Completing the deal successfully in the face of potential employee union opposition would be a big test for Kotak.