The document discusses several mergers that have occurred in the Indian banking sector between 2004-2014. It provides details of four notable mergers:

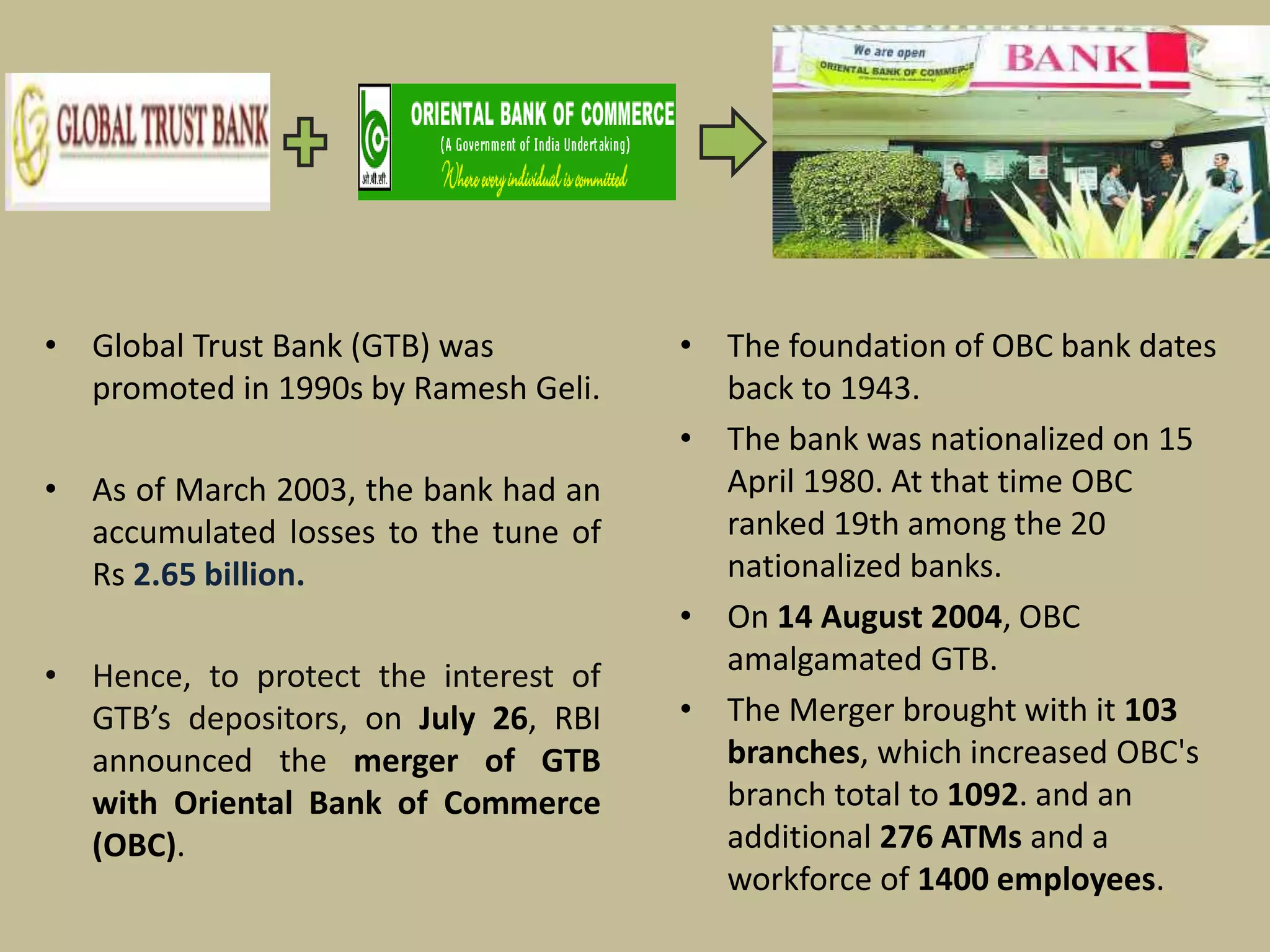

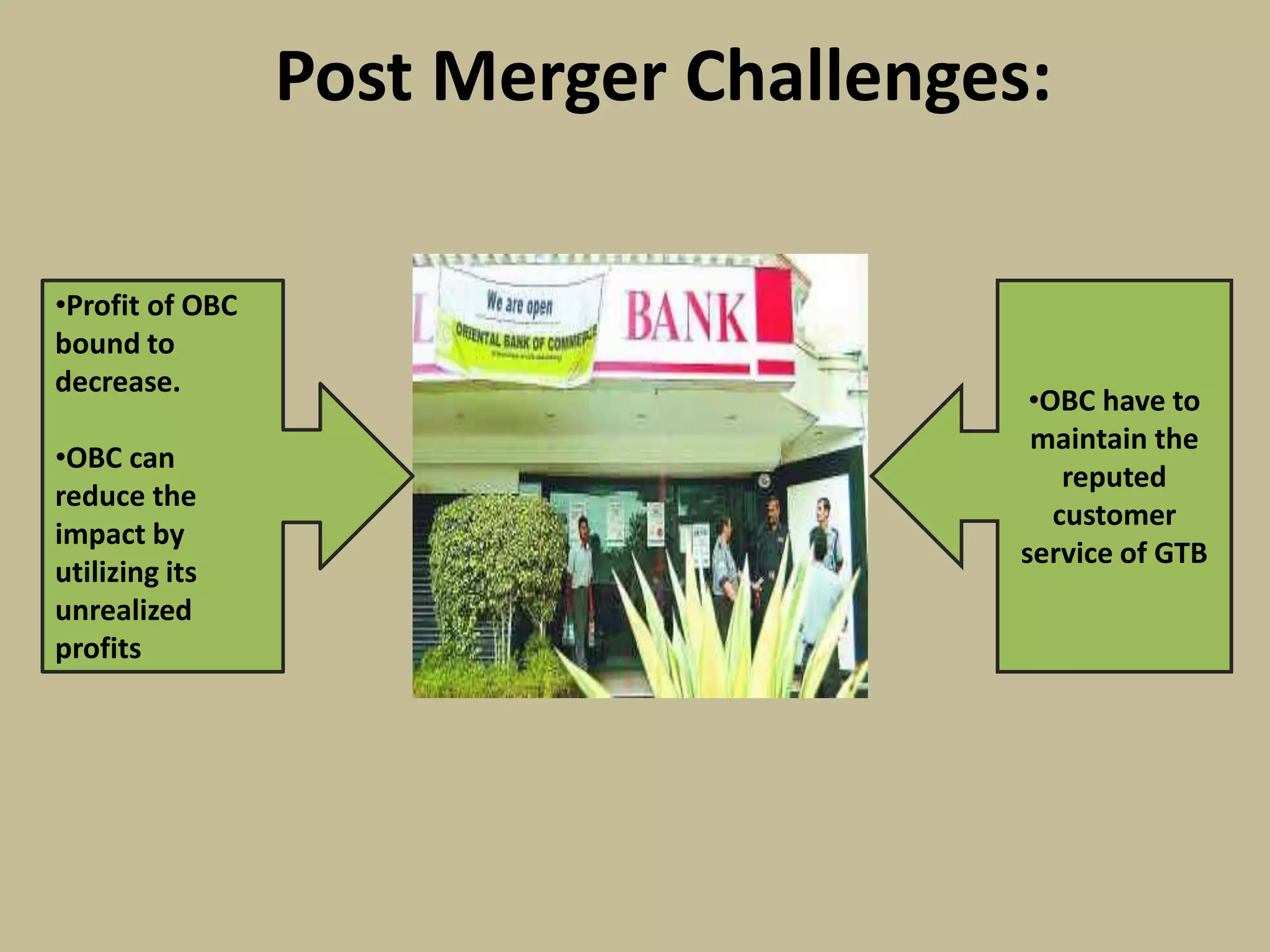

1) In 2004, Global Trust Bank merged with Oriental Bank of Commerce. This increased OBC's branch network and allowed it to gain customers, but also lowered profits initially.

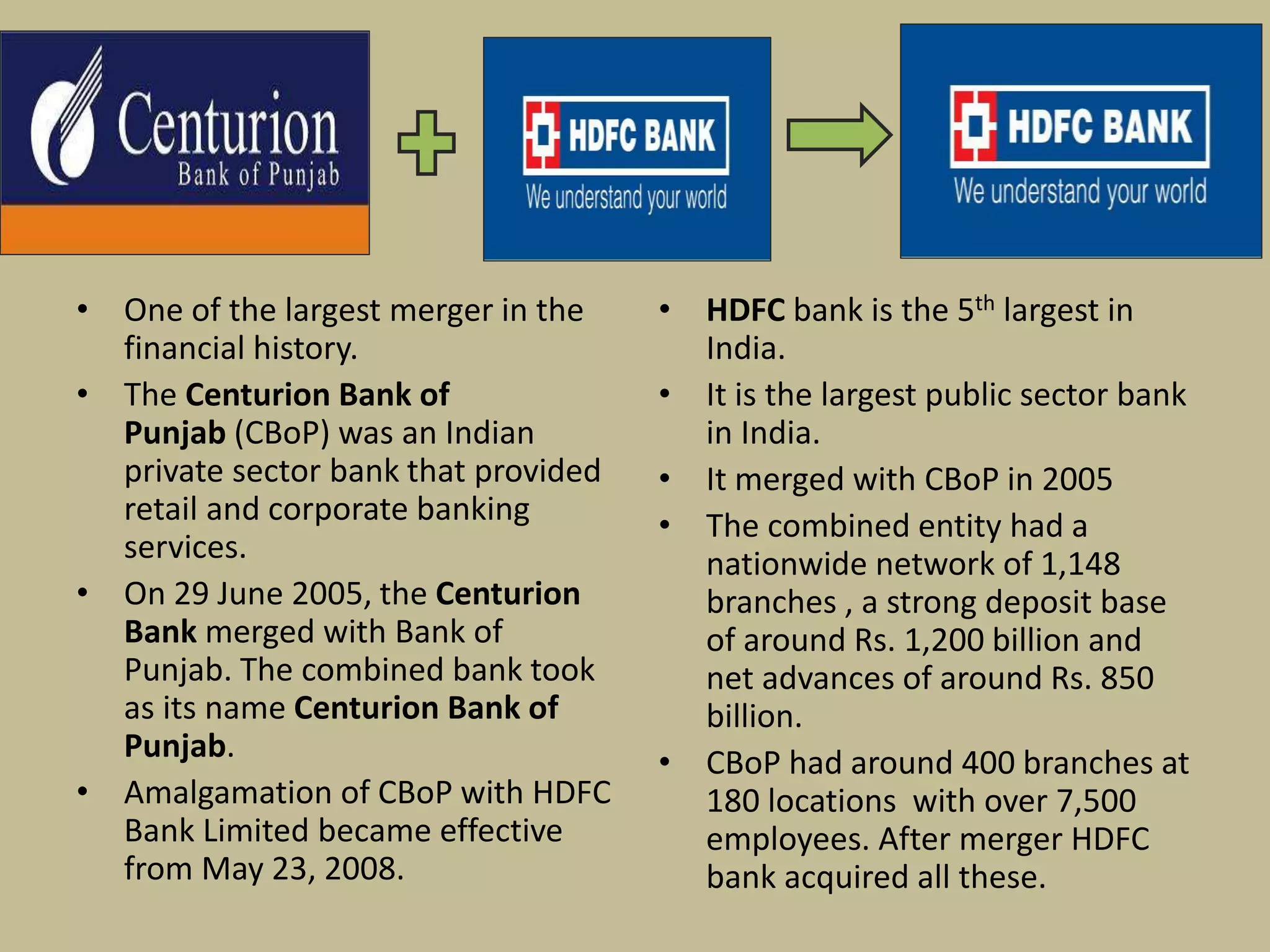

2) In 2008, Centurion Bank of Punjab merged with HDFC Bank. This expanded HDFC's network significantly but also came with challenges of integrating a bank with poorer asset quality.

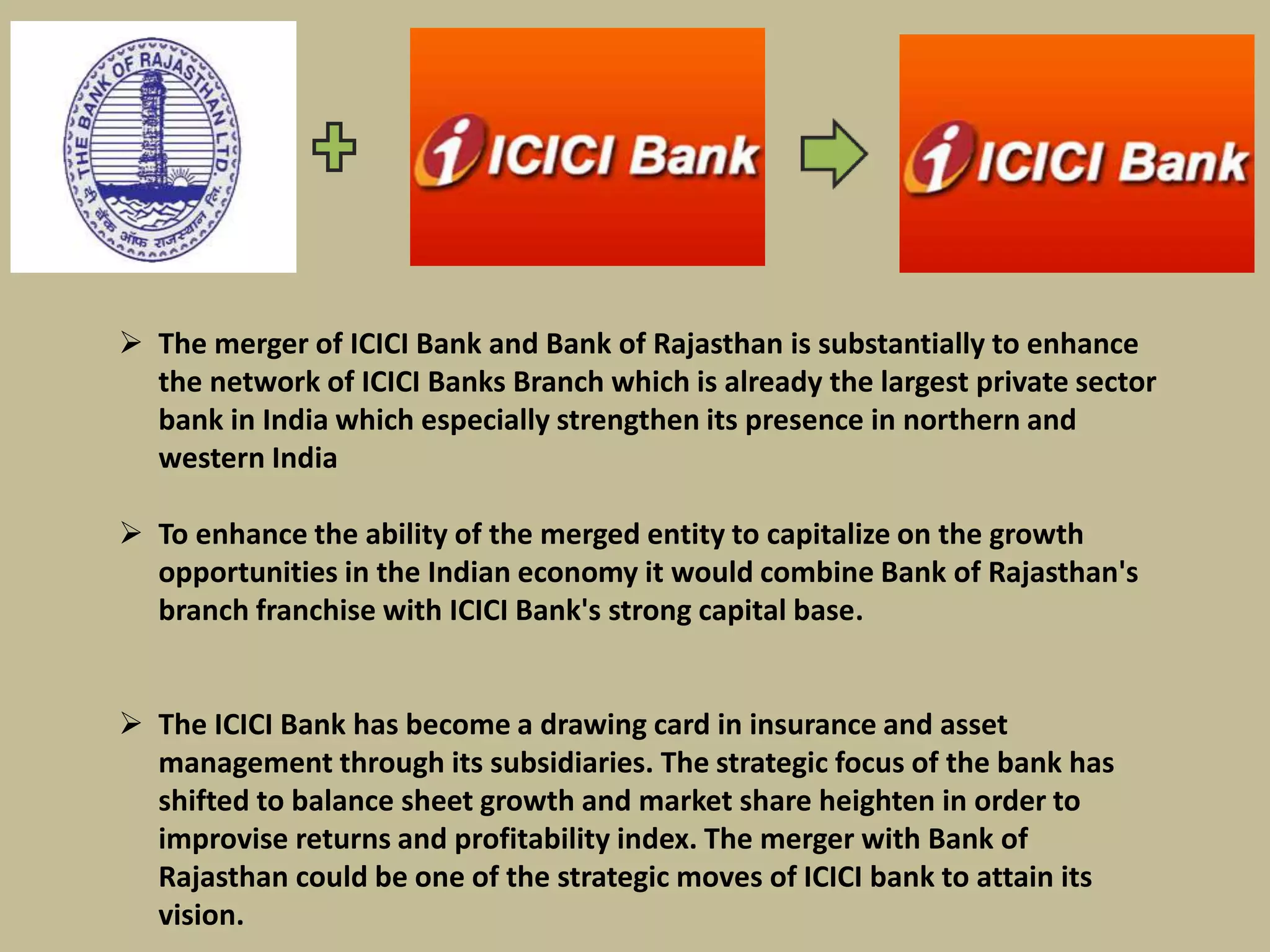

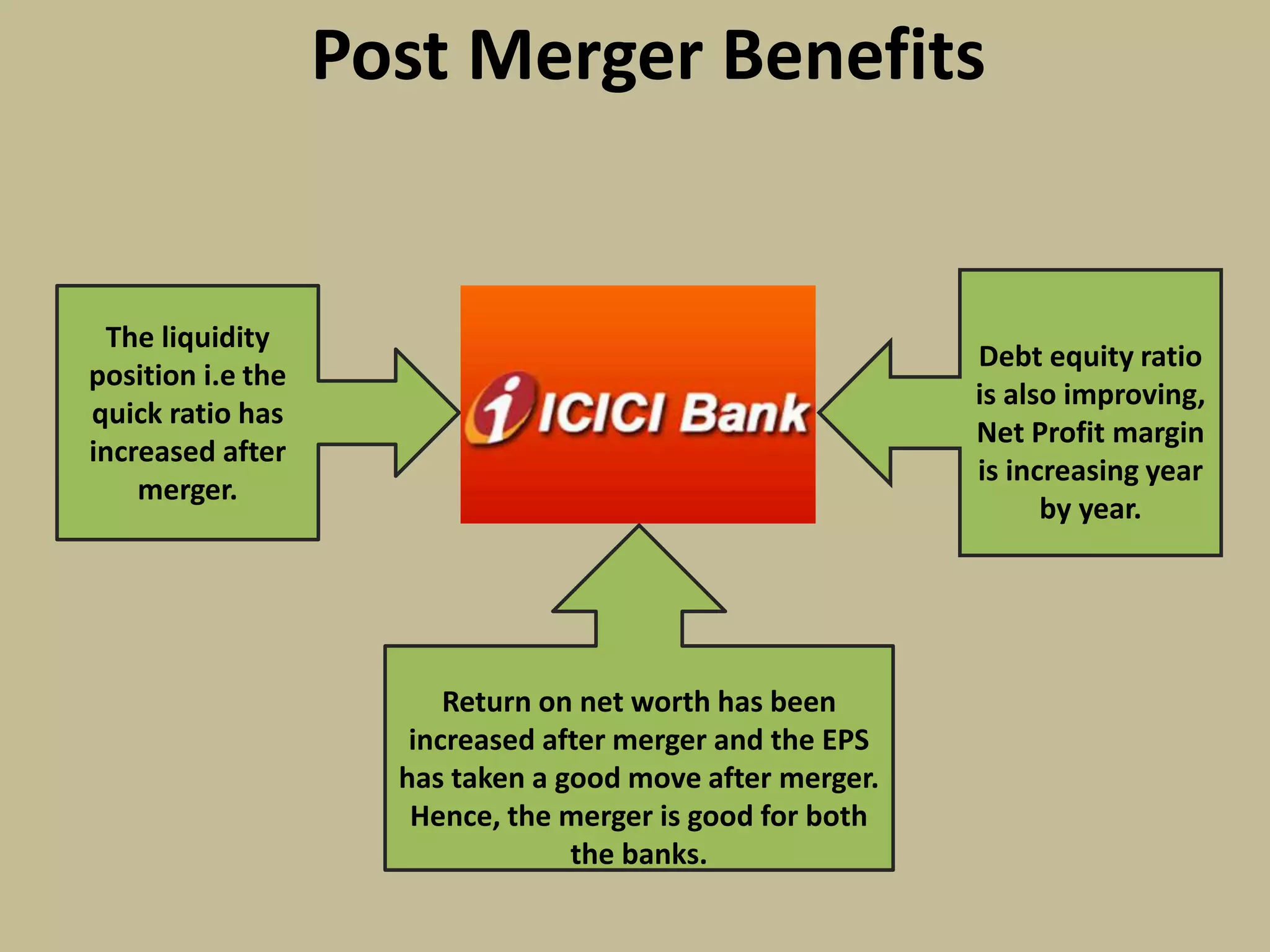

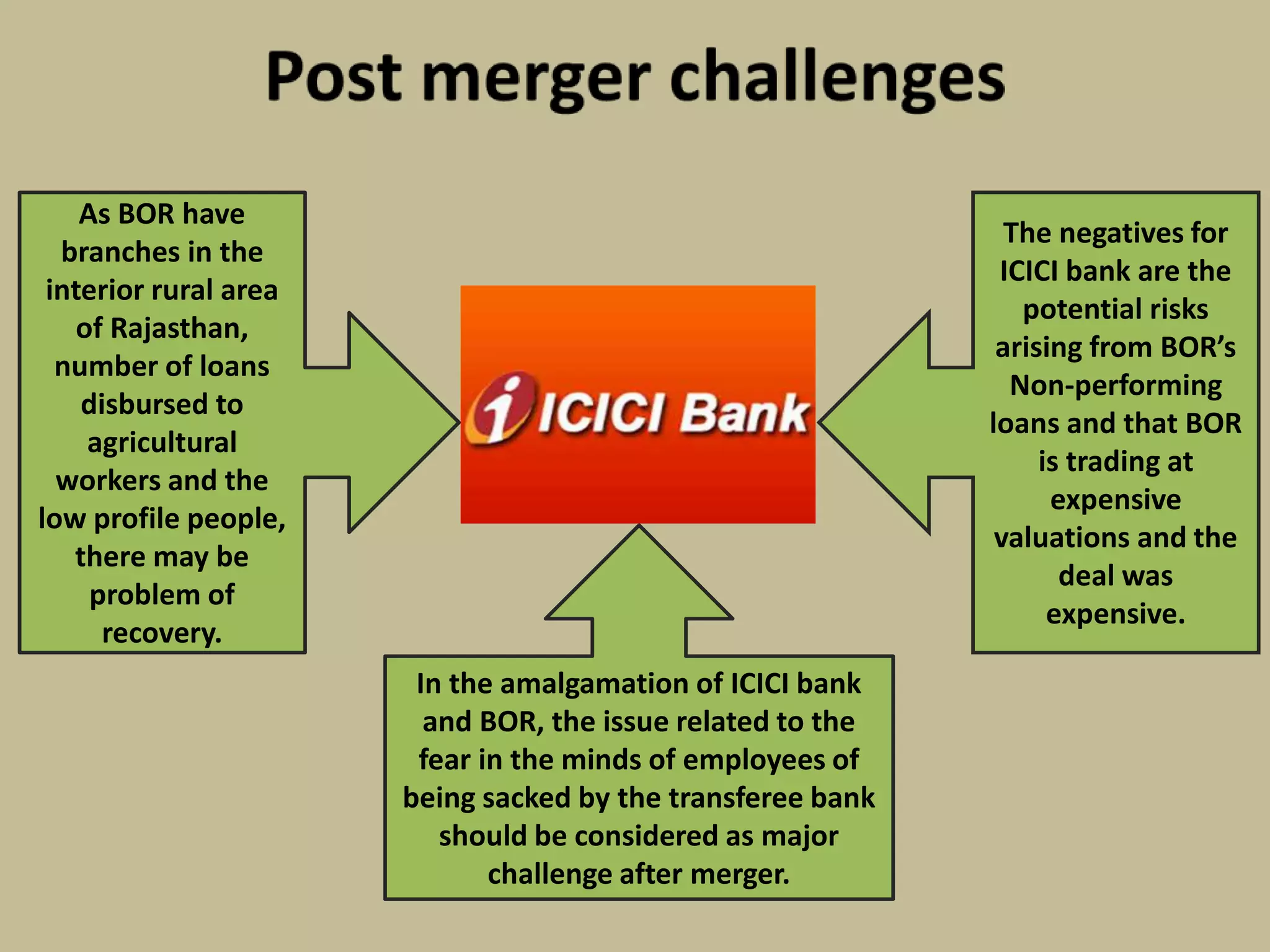

3) In 2010, ICICI Bank merged with Bank of Rajasthan to strengthen its presence in northern and western India but had to address BOR's non-performing loans.

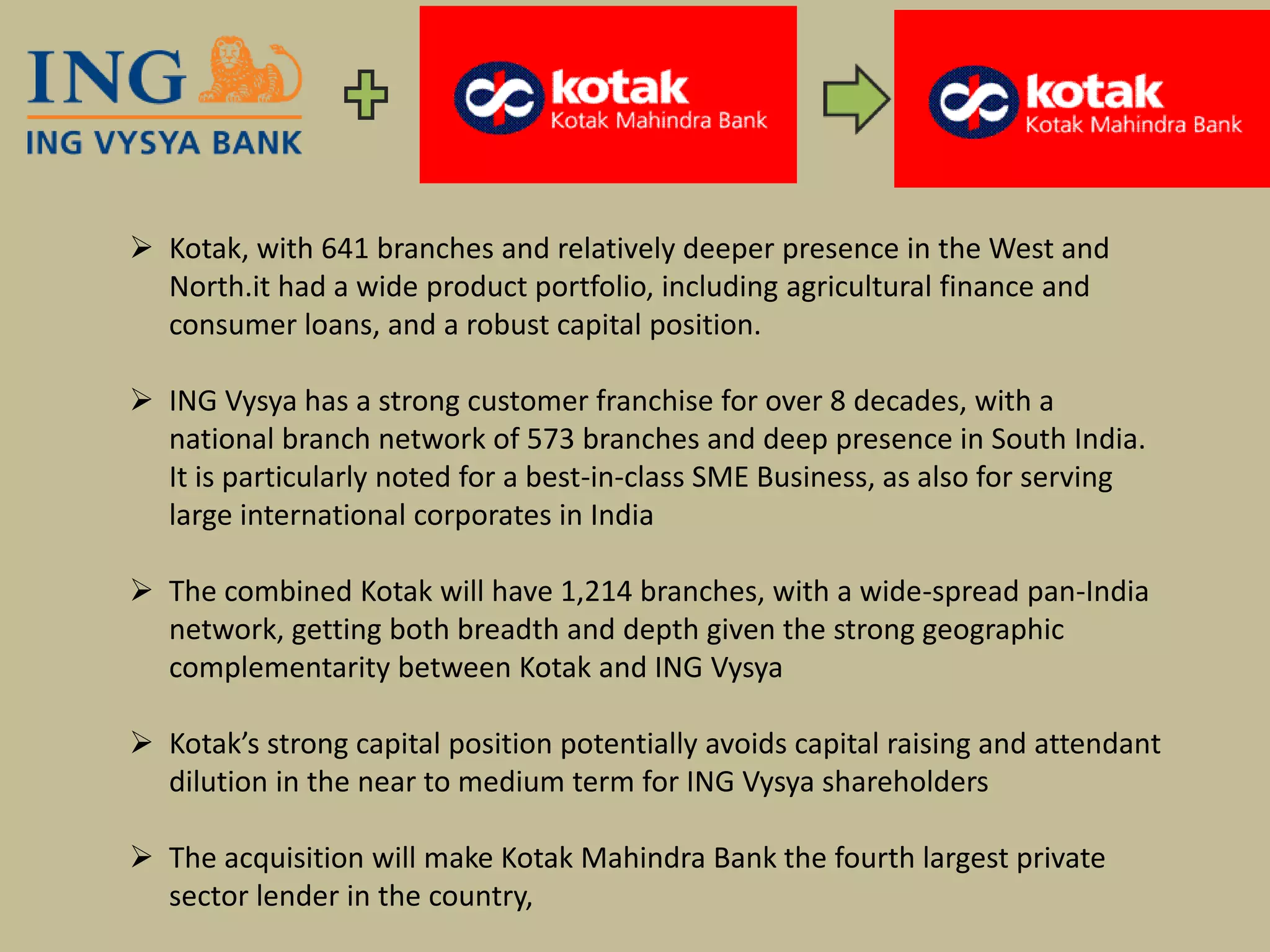

4) In