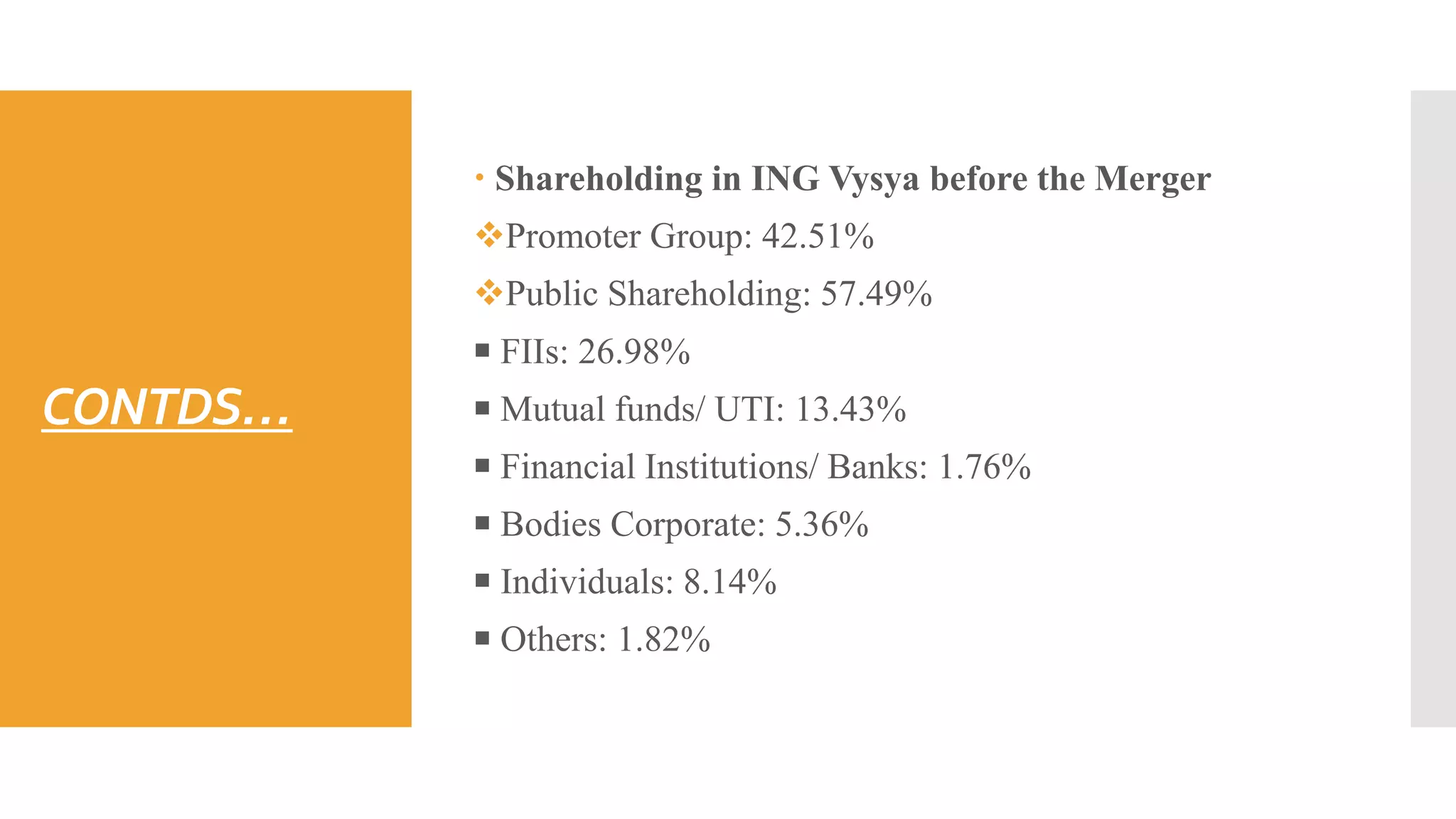

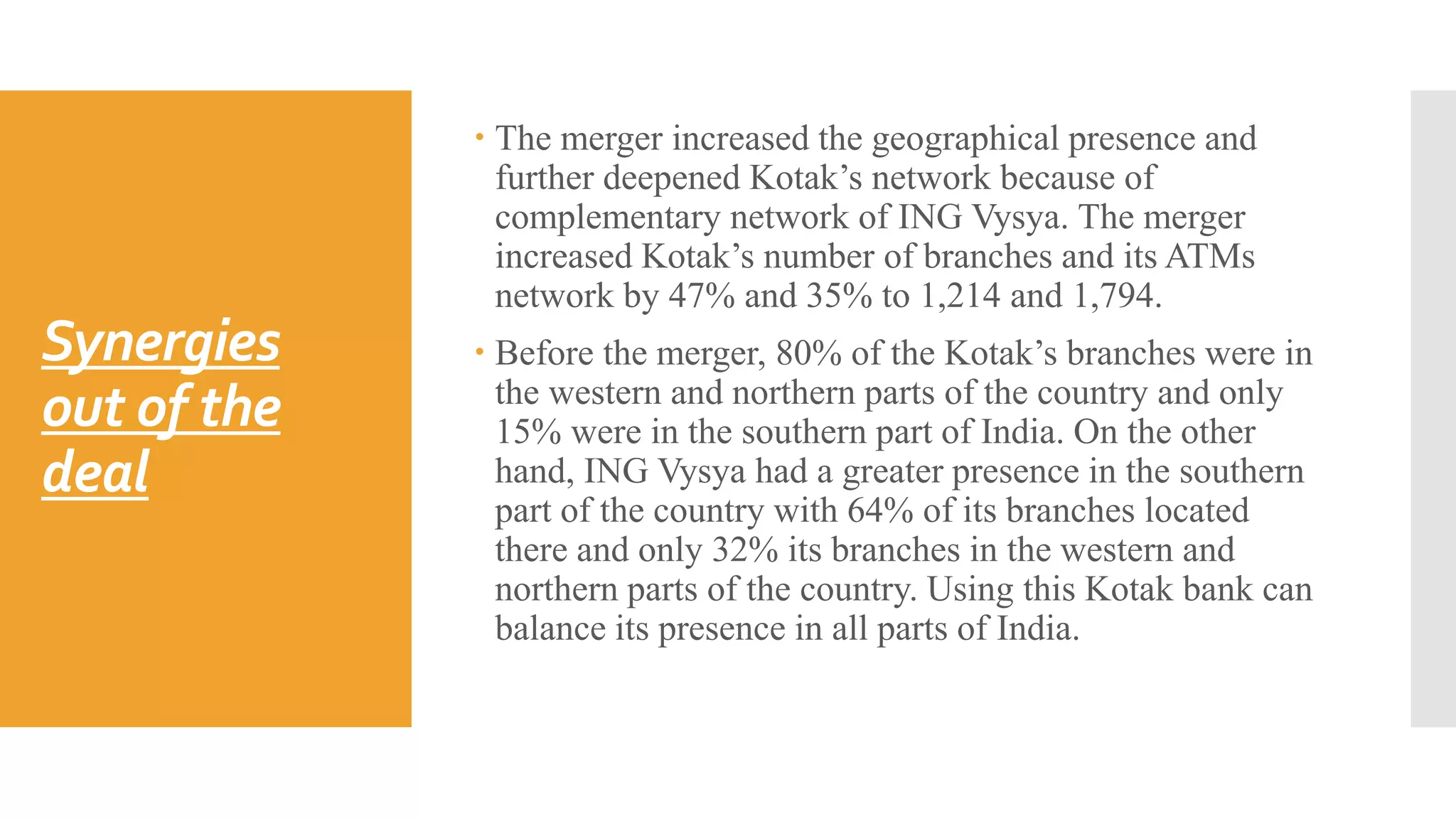

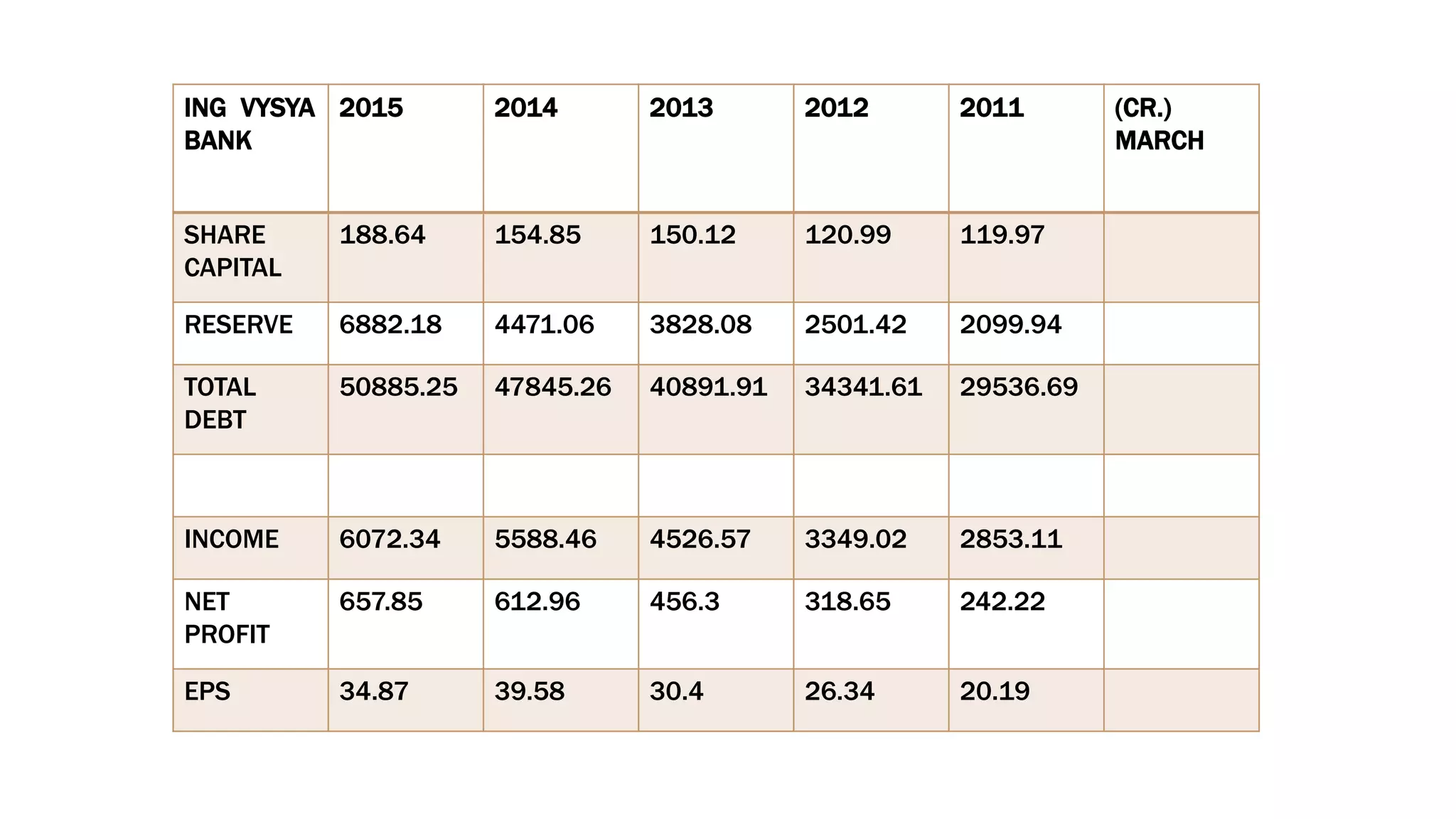

The document details the merger between Kotak Mahindra Bank and ING Vysya Bank, announced on November 20, 2014, valued at Rs. 148.51 billion, with a share exchange ratio that allows ING Vysya shareholders to receive Kotak shares. This strategic merger aimed to enhance geographic presence, customer base, and access to international business, while addressing regulatory approvals and the challenges posed by employee concerns. The transaction signifies a shift towards consolidation in the banking sector, with expected benefits for stakeholders and overall efficiencies for the combined entity.