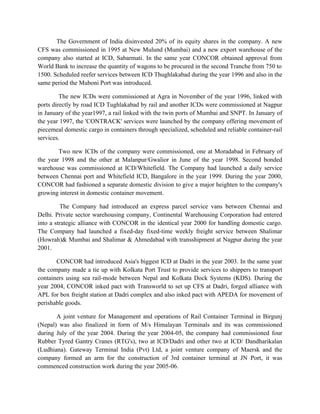

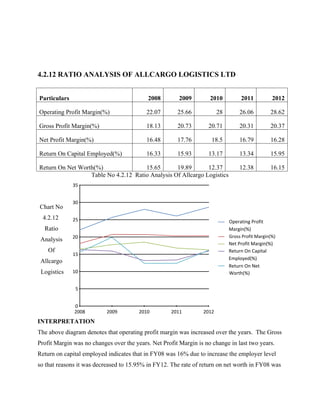

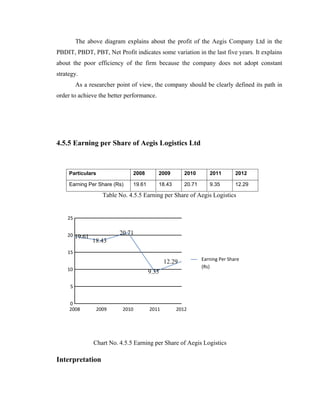

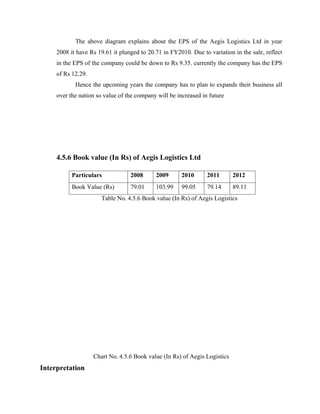

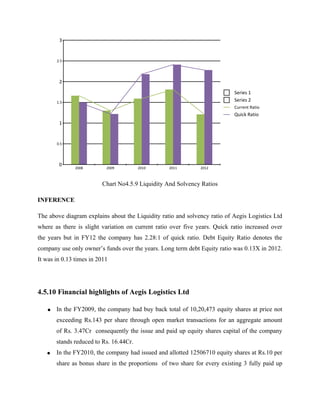

The document provides an overview of the logistics services market in India. It discusses key trends in the industry such as growth of third party logistics, private sector participation, development of logistics parks and warehouses. It also outlines government initiatives to support infrastructure development and liberalize regulations. Looking ahead, the future of the Indian logistics industry is seen as bright with expectations of exponential growth, supported by ongoing investments and developments in the manufacturing, retail and trade sectors.