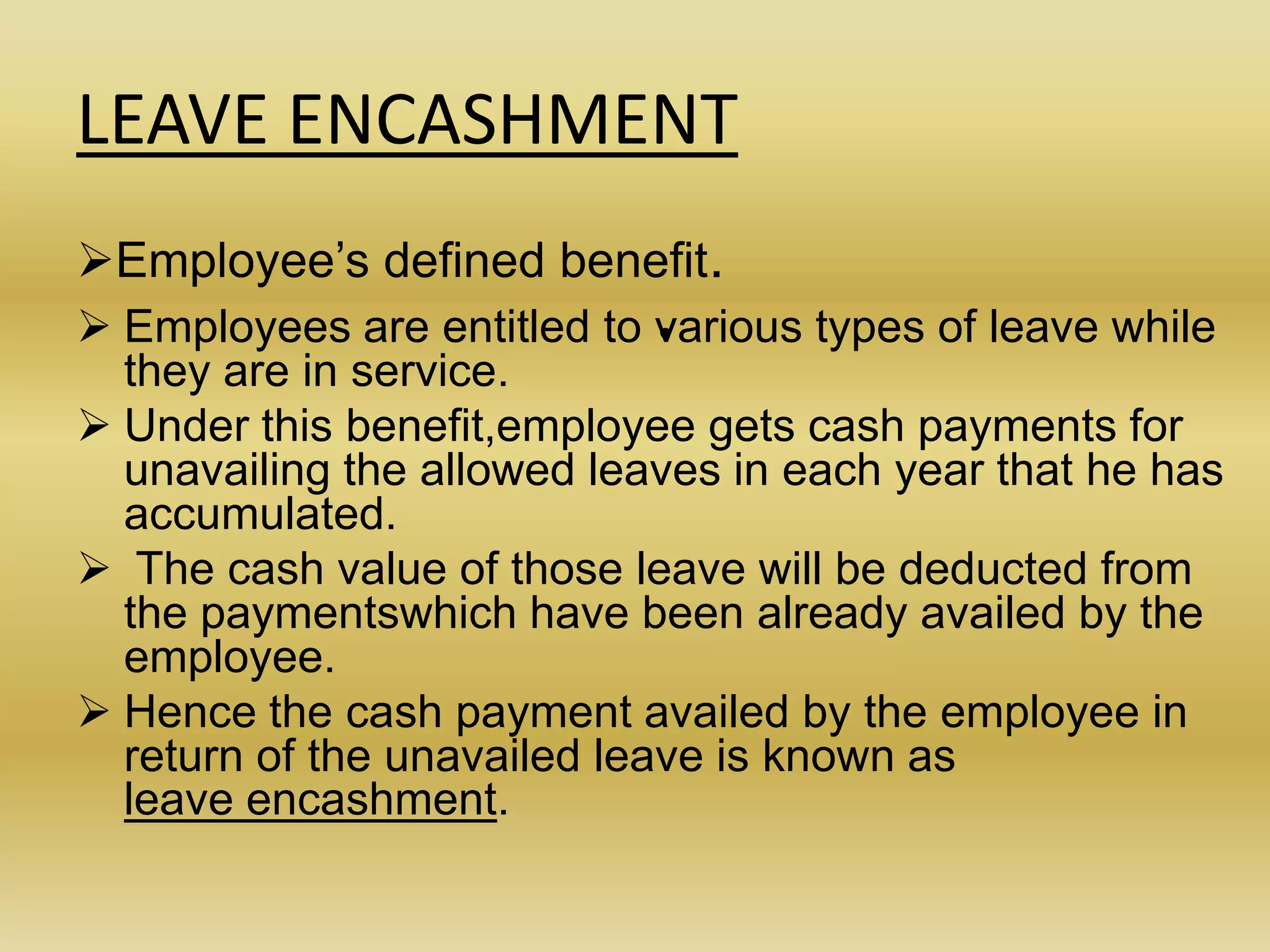

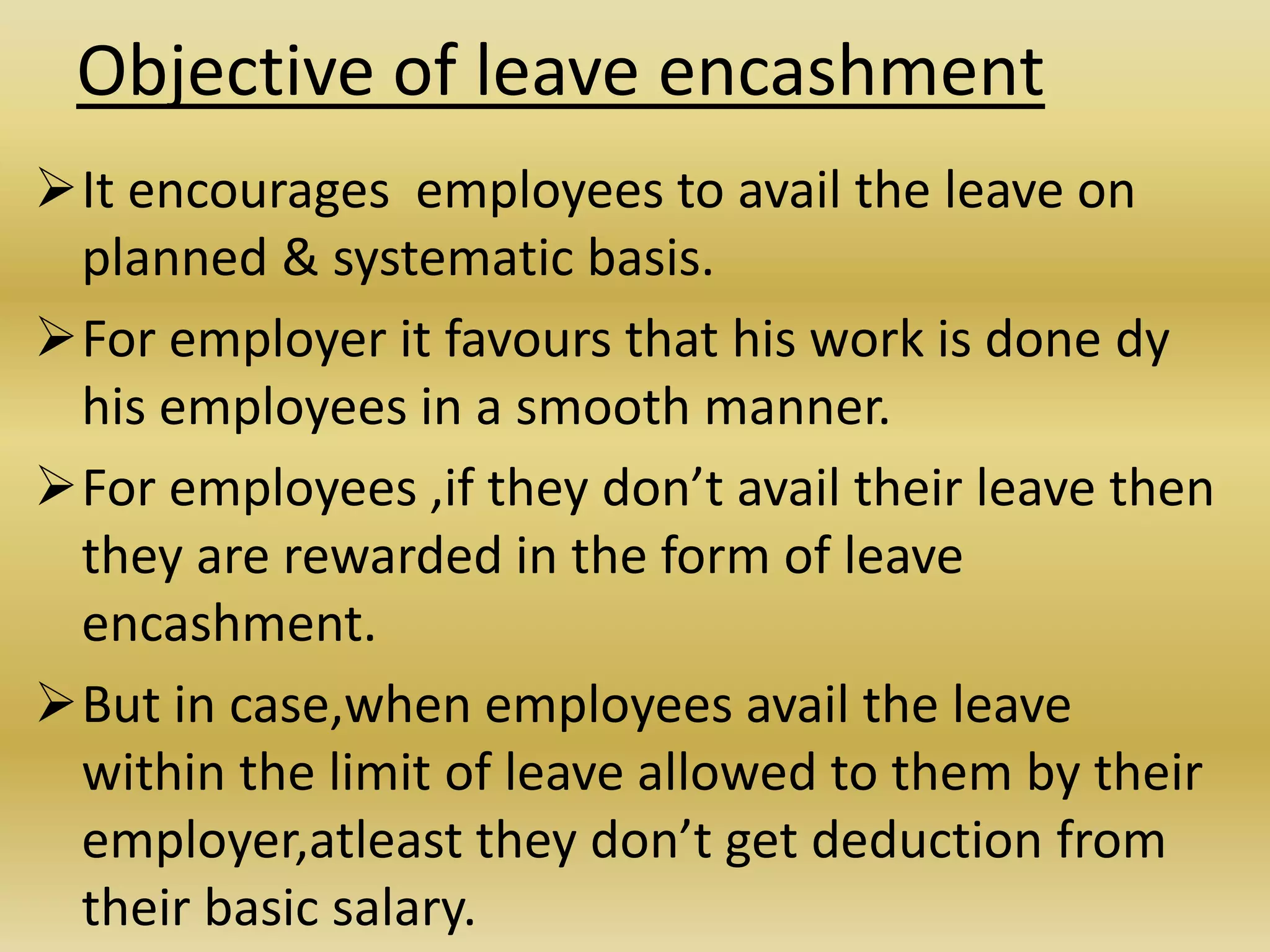

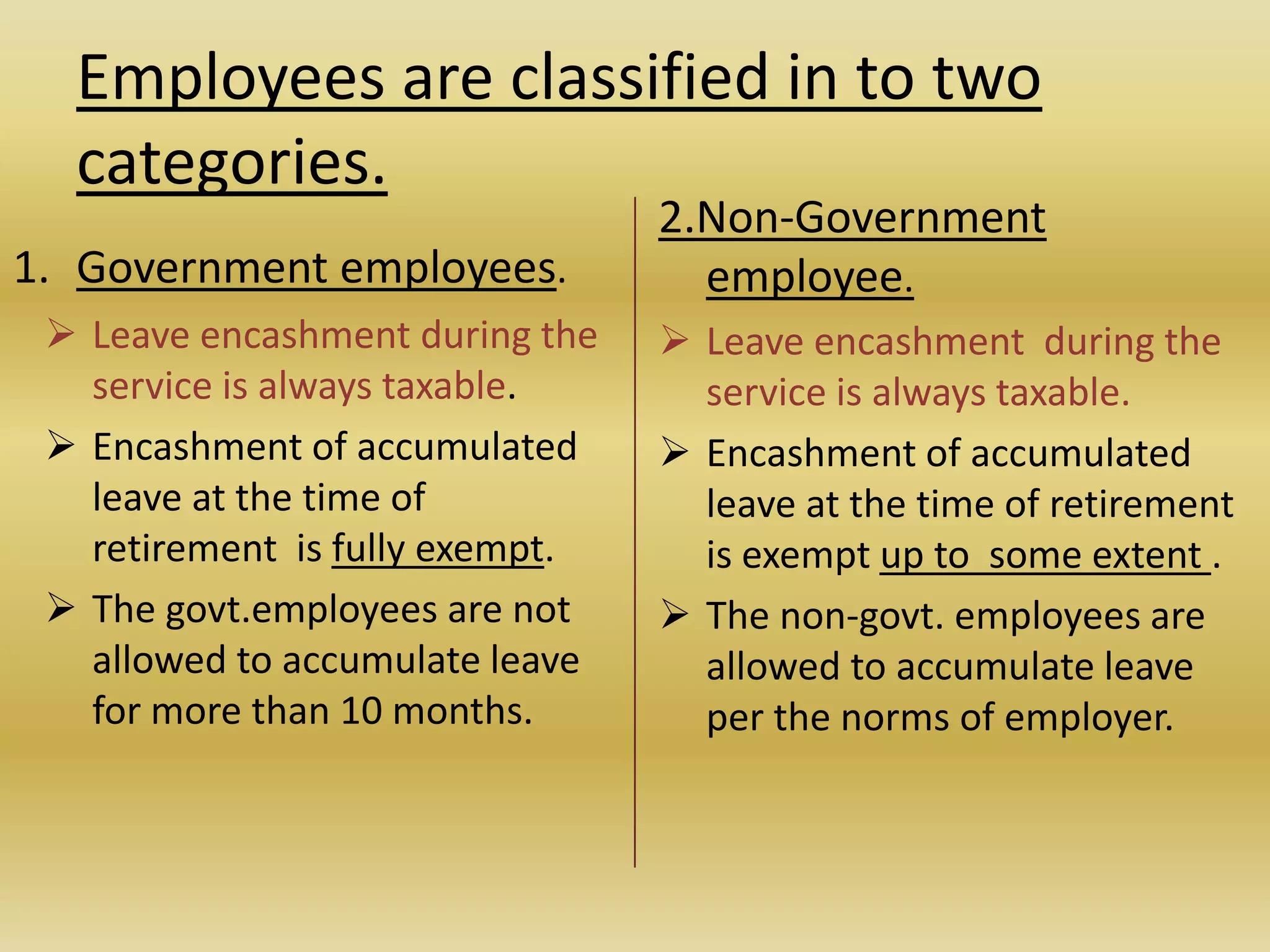

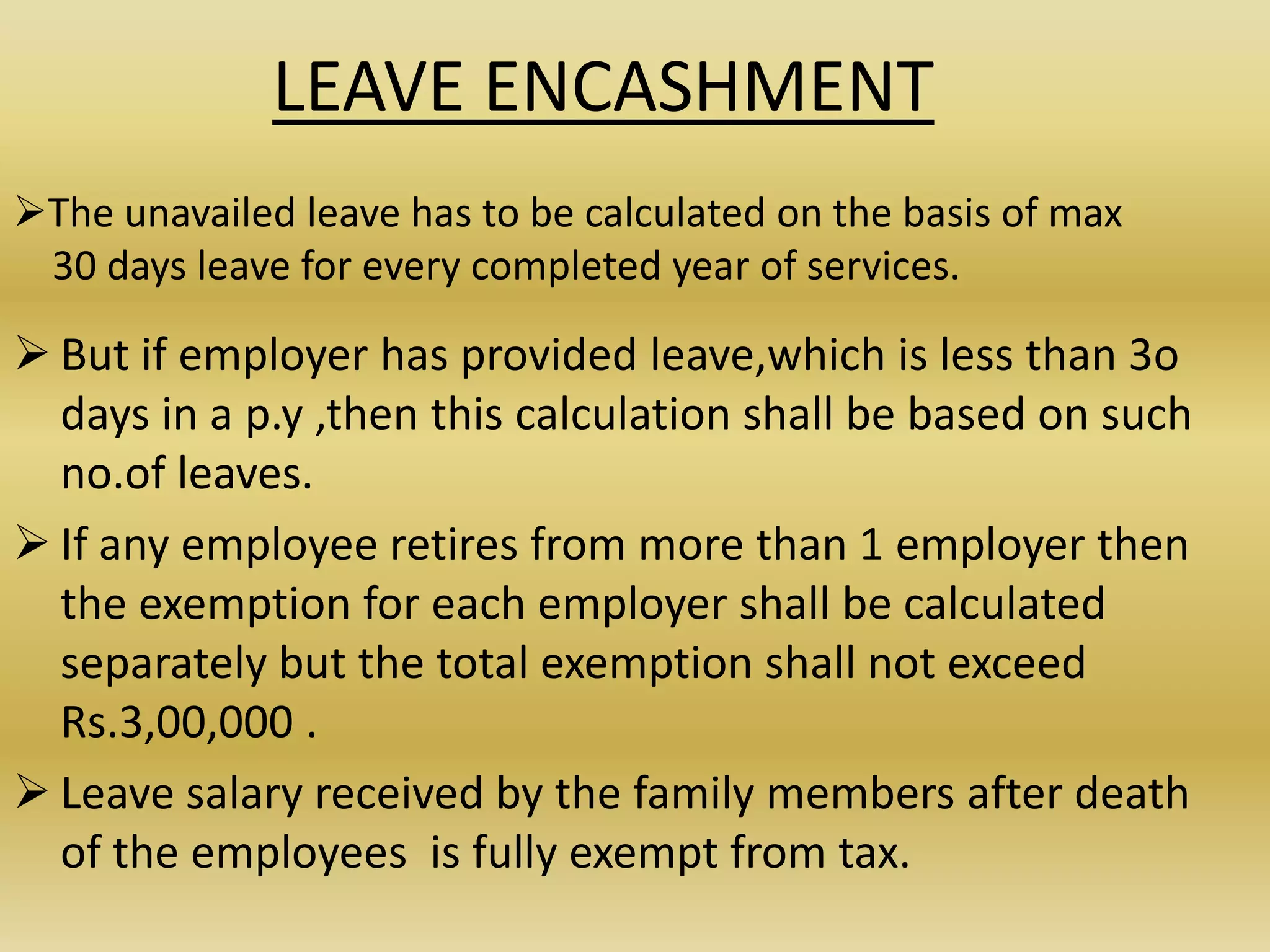

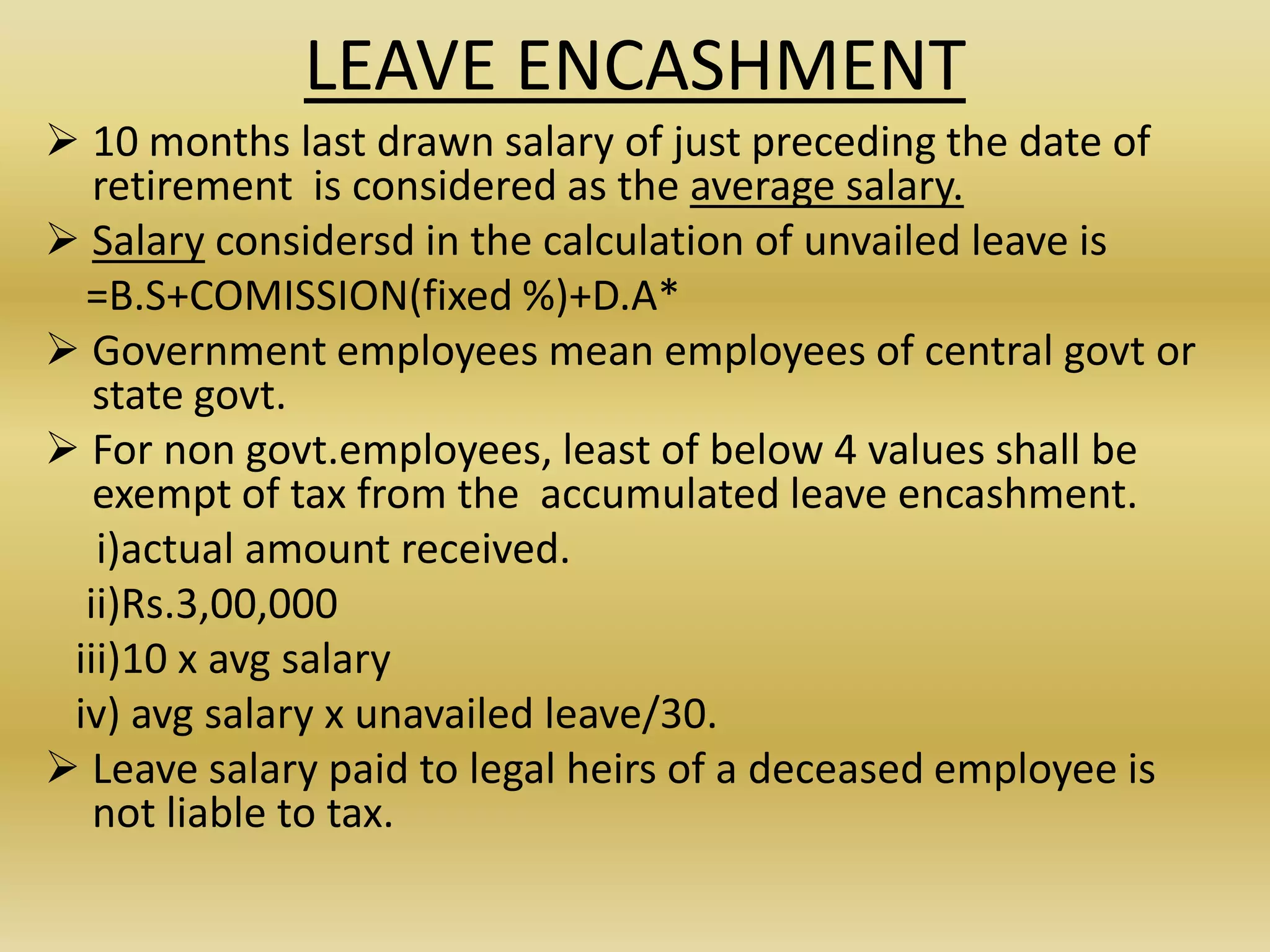

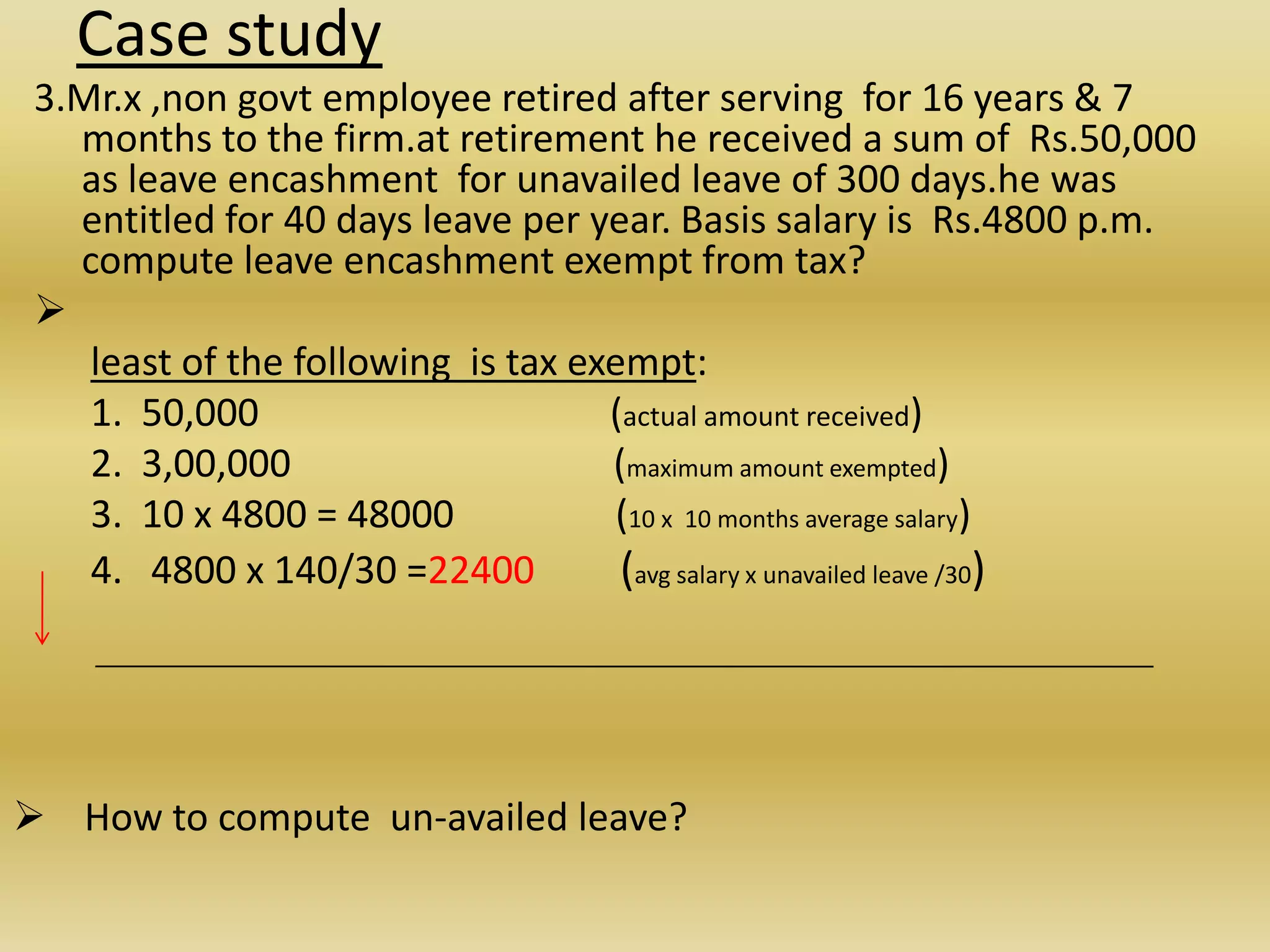

The document discusses leave encashment, which is a cash payment employees receive for unused leave days accumulated during employment. It provides details on: 1) Types of leaves such as casual, medical, and privileged leave and rules around their accumulation and use. 2) Objectives of leave encashment such as encouraging employees to take planned leave and rewarding those who don't use all allotted days. 3) Guidelines for calculating encashable leave, including a maximum of 30 days per year of service and capping payouts for government and non-government employees. 4) Tax treatment of leave encashment, which is taxable during employment but exempt up to Rs. 300,000 for non